What this calculator does

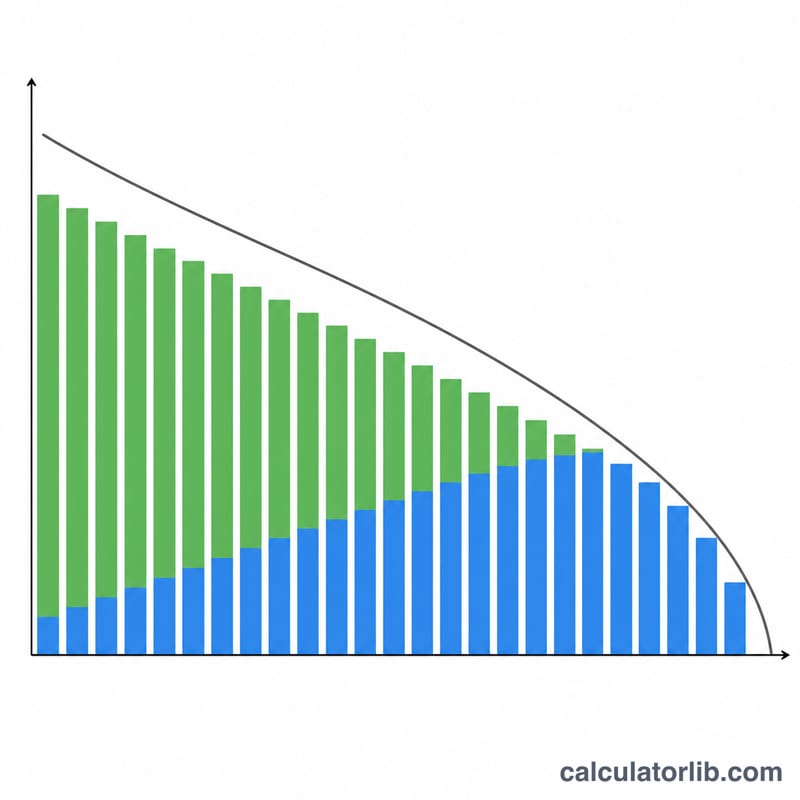

This tool computes the fixed payment for a fully-amortizing loan such as a mortgage, car loan or personal loan. It also returns the total amount you will pay over the life of the loan, the total interest, and a complete period-by-period amortization schedule showing how each payment splits between interest and principal.

How to use it

Enter the amount borrowed (the principal), the nominal annual interest rate as a percentage, the loan term in years, and how many payments you make each year (monthly is the most common). The calculator converts the annual rate to a per-period rate and computes the level payment that pays the loan off exactly at the end of the term.

The formula explained

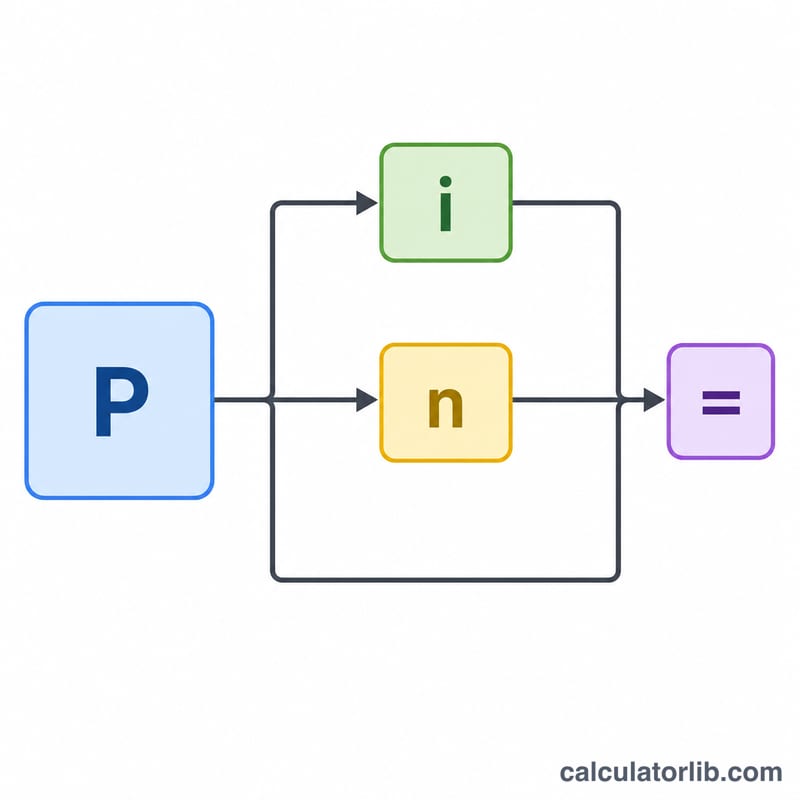

For a level-payment loan the periodic payment is $$\text{Payment} = \dfrac{P \cdot i}{1 - (1 + i)^{-n}}$$ where P is the loan amount, i is the per-period interest rate, and n is the total number of payments. The per-period rate is \(i = \dfrac{r/100}{m}\), and \(n = t \cdot m\). If the interest rate is zero, the payment is simply \(P / n\). Each period's interest equals the outstanding balance times \(i\); the rest of the payment reduces principal. The last payment is reconciled so the ending balance is exactly zero.

Worked example

Borrow 200,000 at 6.5% annual interest for 30 years, paid monthly. Then \(i = 0.065/12 = 0.0054167\) and \(n = 360\). The payment is $$200{,}000 \times \frac{0.0054167}{1 - 1.0054167^{-360}} \approx 1{,}264.14$$ per month. Total paid is about 455,090, of which roughly 255,090 is interest. In the first month, interest is \(200{,}000 \times 0.0054167 = 1{,}083.33\) and principal is \(1{,}264.14 - 1{,}083.33 = 180.81\).

FAQ

Is the quoted rate APR? No. The rate is treated as a nominal annual rate compounded at the payment frequency, the standard US loan convention. APR additionally folds in fees and points and would be a separate calculation.

Does it model extra payments or balloon payments? No. This assumes a fixed rate and equal payments with no extra payments, fees or balloon. Those change the schedule.

Why is the last payment slightly different? Rounding during the term leaves a tiny remainder, so the final payment is adjusted so the balance lands exactly on zero.