What this calculator does

This Savings Goal Calculator tells you how long it will take to reach a target amount when you start with a lump sum, add a fixed deposit every period, and earn compound interest. It is universal compound-interest math, so it works for any currency — only the symbols are cosmetic. The tool ignores taxes, fees and rate changes, giving a clean deterministic estimate.

How to use it

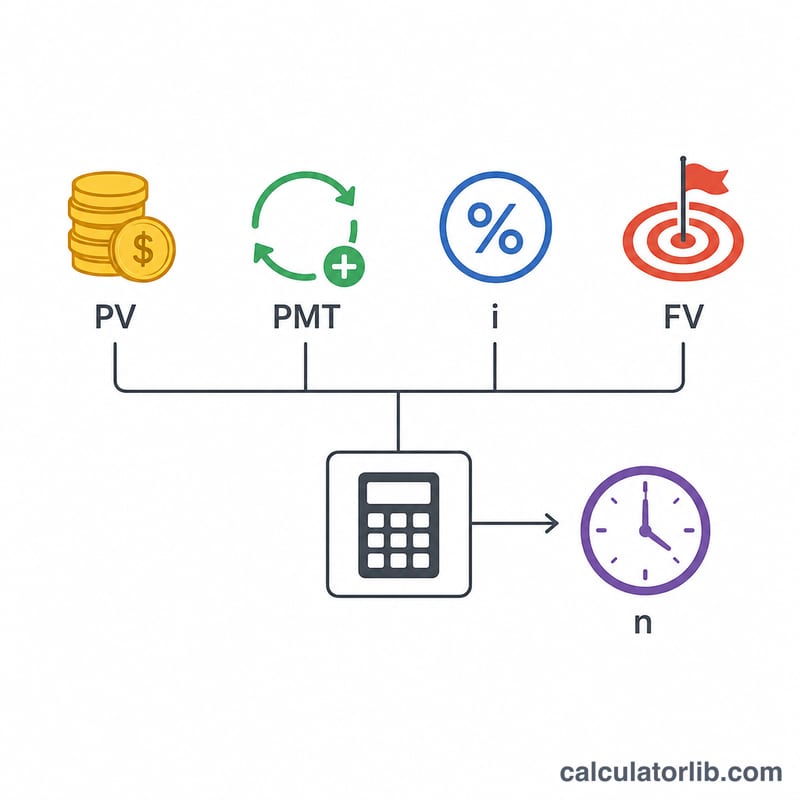

Enter your Starting Amount (present value, often 0), the Savings Goal you want to reach, your Regular Deposit per period, and the Annual Interest Rate. Choose how often interest compounds and deposits are made — deposits are assumed to occur at the same frequency. Pick whether deposits land at the end of each period (ordinary annuity) or the beginning (annuity due). The result shows the time in years, the whole number of periods required, total deposited and total interest earned.

The formula explained

Starting from the future-value-of-an-annuity equation \(FV = PV(1+i)^{n} + PMT\cdot\left[\dfrac{(1+i)^{n} - 1}{i}\right]\), we solve for n. Letting i be the periodic rate (annual rate ÷ periods per year), the closed form is $$n = \dfrac{\ln\!\left(\dfrac{FV + PMT/i}{PV + PMT/i}\right)}{\ln(1+i)}.$$ For annuity-due timing, \(PMT/i\) is replaced by \(PMT(1+i)/i\). When the rate is 0%, the balance grows only by deposits, so $$n = \dfrac{FV - PV}{PMT}.$$

Worked example

Start with $1,000, goal $10,000, deposit $100 monthly at 5% compounded monthly. The periodic rate \(i = 0.05/12 = 0.0041667\) and \(PMT/i = 24{,}000\). Then $$x = \frac{10{,}000 + 24{,}000}{1{,}000 + 24{,}000} = 1.36,$$ and $$n = \frac{\ln(1.36)}{\ln(1.0041667)} \approx 73.95 \text{ months}$$ — round up to 74 months, about 6 years 2 months. Total deposited \(= 1{,}000 + 100\times74 = \$8{,}400\), and interest earned is roughly $1,607.

FAQ

What if I set the rate to 0%? The calculator uses the linear formula \(n = (FV - PV)/PMT\), so the goal is reached purely through deposits.

Can I reach a goal with no deposits? Yes, if you have a starting balance and a positive rate — it computes pure compound growth, \(n = \ln(FV/PV)/\ln(1+i)\).

Why is the whole-period number rounded up? Interest credits and deposits happen at discrete period ends, so you need a full extra period to meet or exceed the target.