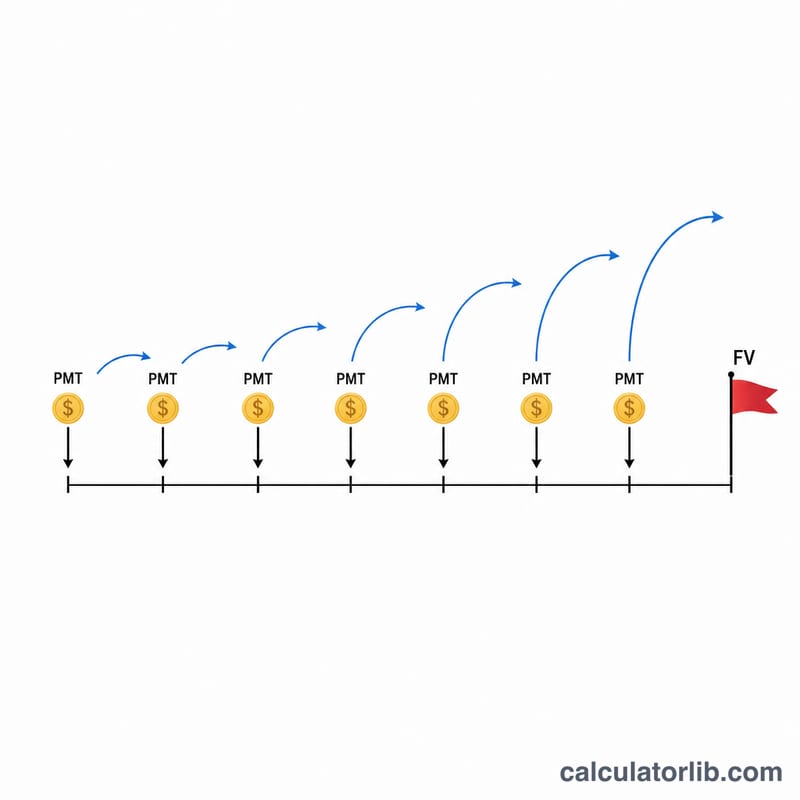

What this calculator does

The Savings Goal Calculator tells you exactly how much you must set aside each period — weekly, bi-weekly, monthly, quarterly, or annually — to reach a target balance (future value) by a chosen date. Instead of guessing, you enter the goal, the time horizon, how often you deposit, and the interest rate, and it returns the required recurring deposit. Interest is compounded daily (365 times per year) and deposits are assumed to be made at the beginning of each period (an annuity-due), which is how most automated savings plans work.

How to use it

1) Enter your Savings Goal — the amount you want to have. 2) Set the Saving Period in years. 3) Choose how often you make deposits under Making Deposits. 4) Enter the annual Interest Rate as a percent. The result shows the deposit you need each period, plus the total you will deposit and the interest you will earn.

The formula explained

Because interest compounds daily but you deposit less often, the calculator first finds the effective rate earned over one deposit period: $$i = \left(1 + \frac{r}{365}\right)^{365/q} - 1$$ where r is the annual rate as a decimal and q is deposits per year. The number of deposits is \(N = q \times Y\). Using the future value of an annuity-due, the required payment is $$\text{PMT} = \frac{\text{FV}}{\left(\dfrac{(1+i)^{N}-1}{i}\right)(1+i)}$$ If the rate is zero, this simplifies to \(\text{PMT} = \text{FV} / N\).

Worked example

Goal $15,000 in 10 years, monthly deposits (q = 12), 0.75% rate. The monthly effective rate is \(i \approx 0.00062522\), with \(N = 120\) periods. The annuity-due factor is about 124.64, so $$\text{PMT} = 15{,}000 / 124.64 \approx \$120.34 \text{ per month}$$ You would deposit roughly $14,440 total and earn about $560 in interest.

FAQ

Are deposits at the start or end of each period? The start (annuity-due), so each deposit earns a little extra interest.

Why daily compounding? Many savings and money-market accounts credit interest daily; the model uses 365 days per year.

What if I enter 0% interest? The tool divides the goal evenly across all deposits, so \(\text{PMT} = \text{goal} / \text{number of deposits}\).