What this calculator does

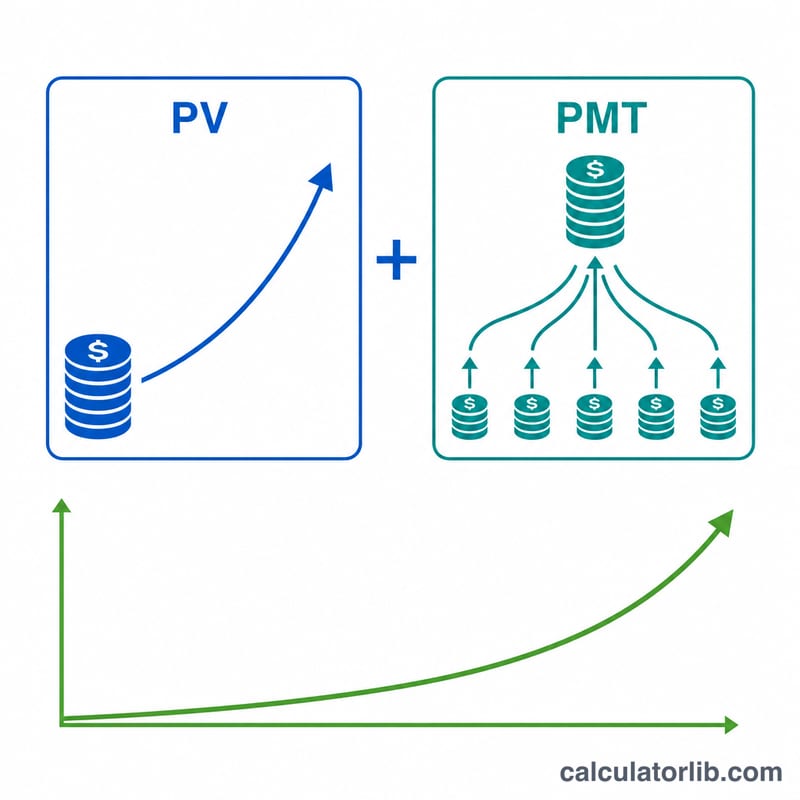

The Savings Account Future Value Calculator projects how much a savings account will be worth after a chosen number of years. It combines a one-time starting balance with regular periodic deposits and applies compound interest. It then shows your future savings, the total number of deposits made, how much you contributed without interest, and the total interest earned. The tool is currency-agnostic — the dollar signs are just labels, so the math works for any currency.

How to use it

Enter your starting balance, the deposit amount, and how often you deposit (deposit frequency). Choose whether deposits land at the beginning or end of each period, set the term in years, the annual interest rate as a percent, and the compounding frequency. Press calculate to see the projected balance.

The formula explained

Because interest may compound at a different rate than your deposit schedule, the nominal annual rate r is first converted to an effective rate per deposit period: $$i = \left(1 + \frac{r}{m}\right)^{m/q} - 1$$ where m is compounding periods per year and q is deposits per year. With n = q × t total deposits, the future value is the grown starting balance plus an annuity of deposits: $$\text{FV} = \text{PV}(1+i)^n + \text{PMT}\cdot\frac{(1+i)^n - 1}{i}\cdot(1 + i\cdot\text{type})$$ The "type" flag is 1 for beginning-of-period deposits (annuity-due) and 0 for end-of-period (ordinary annuity). If the rate is zero, FV simply equals \(\text{PV} + \text{PMT}\cdot n\).

Worked example

Starting balance $500, weekly deposits of $50 (q = 52) at the beginning of each week, 10 years, 0.75% annual rate compounded daily (m = 365). Then \(n = 520\), \(i \approx 0.000144243\) per week, \(\text{FV} \approx \$27{,}540.72\). You contributed \(500 + 50\times520 = \$26{,}500\), so total interest is about $1,040.72.

FAQ

What does compounding frequency change? More frequent compounding (e.g. daily vs. annually) slightly increases the effective rate and therefore the final balance.

Beginning vs. end of period? Depositing at the beginning of each period earns one extra period of interest per deposit, producing a marginally higher balance.

Is this a guarantee? No. It assumes a constant rate and steady deposits; actual savings rates and contributions vary over time.