What this calculator does

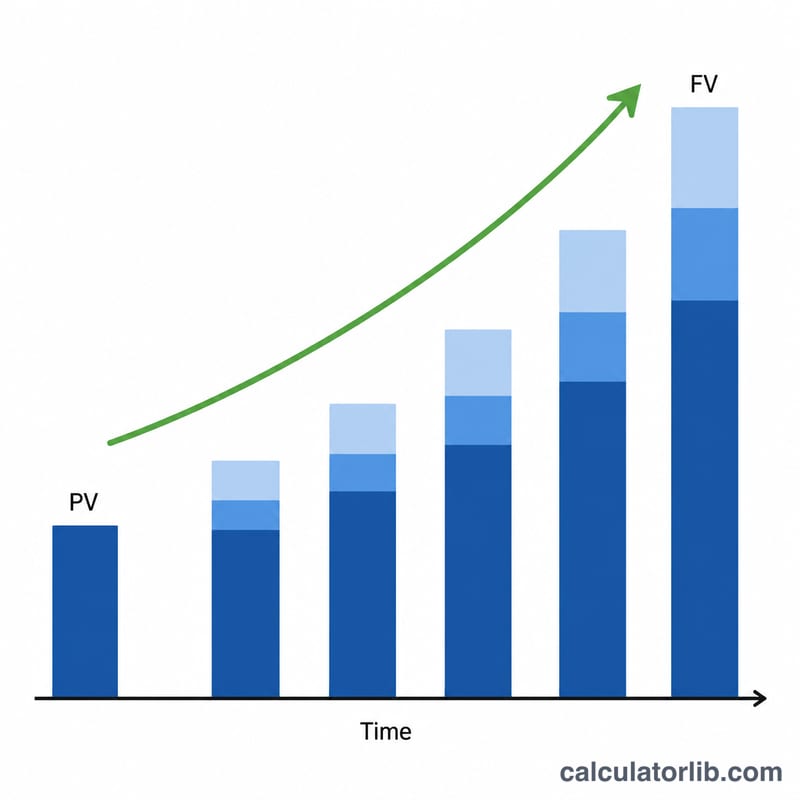

This Future Value (FV) calculator combines two classic time-value-of-money problems in one tool. It grows a present-value lump sum forward to the end of your time horizon, and it can also add the accumulated value of a stream of periodic cash flows (an annuity). The cash flows can be level, can grow each period (a growing annuity), can occur at the start of each interval (annuity-due) or the end (ordinary annuity), and can be deposits that build value or withdrawals that reduce it. The math is universal: it applies in any country and any currency, so the currency symbol is purely cosmetic.

How to use it

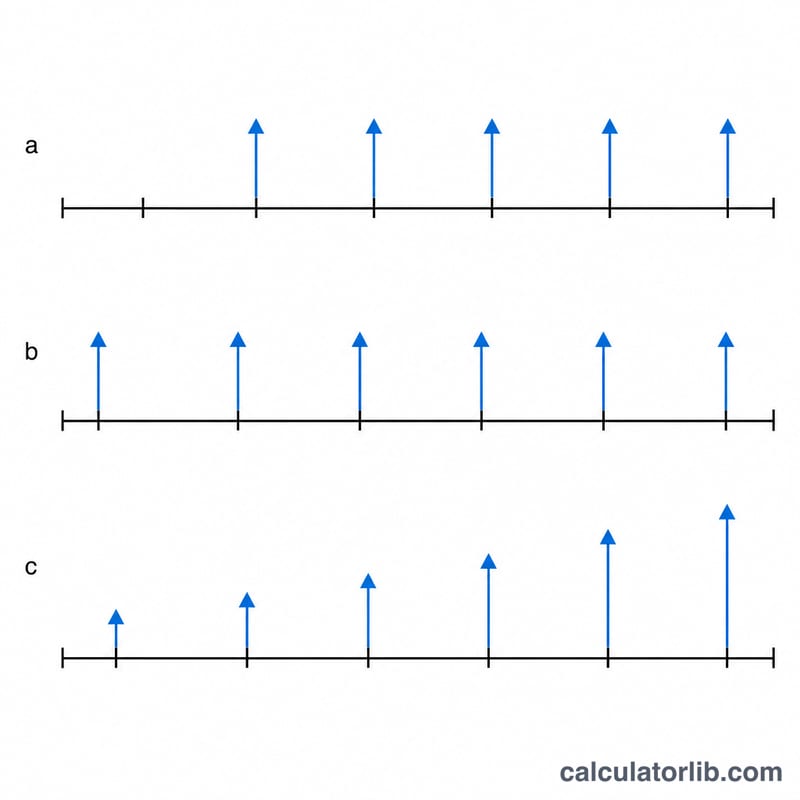

Enter the Present Value (PV) you are starting with, the Number of Periods (t), the nominal Rate (R) as a percent, and how many times interest compounds per period (m) — or tick "Continuous compounding". To model contributions, fill in the payment Amount (PMT), choose Deposits or Withdrawals, set the number of payments per period (q), an optional PMT Growth (G), and whether payments fall at the start or end of each interval. Leave PMT blank or 0 for a pure lump-sum calculation.

The formula explained

The lump sum uses $$FV = PV\left(1+\frac{r}{m}\right)^{mt}.$$ For the annuity, the compounding rate is first converted into an equivalent rate over one payment interval: $$i_{pay} = \left(1+\frac{r}{m}\right)^{m/q} - 1,$$ with \(N = q \cdot t\) total payments. The level ordinary annuity then accumulates as $$PMT \cdot \frac{(1+i_{pay})^{N} - 1}{i_{pay}}.$$ Annuity-due multiplies by \((1+i_{pay})\). A growing annuity uses $$PMT \cdot \frac{(1+i_{pay})^{N} - (1+g)^{N}}{i_{pay} - g},$$ with safe limit forms when \(i_{pay}\) equals \(g\) or the rate is zero.

Worked example

PV = 15,000, t = 10 periods, R = 5.25%, m = 12, no payments. Here \(r/m = 0.004375\) and \(mt = 120\), so $$(1.004375)^{120} = 1.6885239$$ and $$FV = 15{,}000 \times 1.6885239 = 25{,}327.86.$$ Total interest = \(25{,}327.86 - 15{,}000 = 10{,}327.86\).

FAQ

What is the difference between ordinary and due? An ordinary annuity pays at the end of each interval; an annuity-due pays at the start, so every payment earns one extra interval of interest.

What is a growing annuity? One where each payment is larger than the last by a fixed percentage G — useful for modeling contributions that rise with inflation or salary.

How is total interest computed? Total interest = FV - PV - total contributions (with withdrawals counted as negative contributions), isolating the earnings from your own deposits.