What this calculator does

This tool tells you how much you need to set aside each month to reach a specific savings target by a chosen date. Instead of just dividing your goal by the number of months, it accounts for the compound growth your money earns along the way, so the required deposit is lower when your expected return is higher.

How to use it

Enter your savings goal (the amount you want to have), the time to goal in years, and your expected annual return rate as a percentage. The calculator converts the rate to a monthly rate and the years to months, then solves for the level monthly deposit needed.

The formula explained

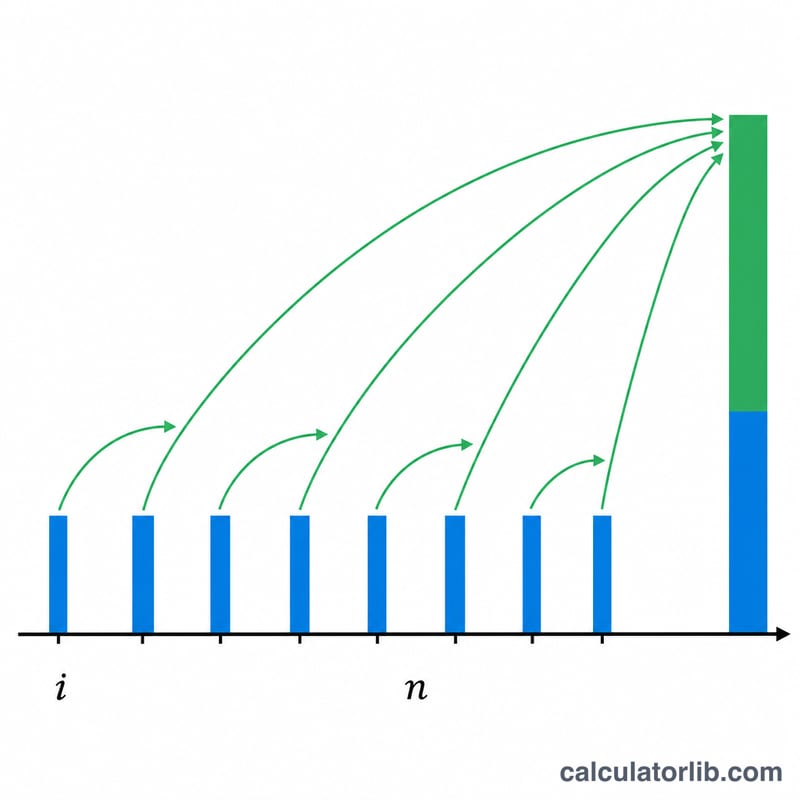

It uses the future value of an ordinary annuity, rearranged to solve for the payment:

$$\text{PMT} = \text{FV} \times \frac{i}{(1 + i)^{n} - 1}$$

Here \(i\) is the monthly rate (annual rate divided by 12) and \(n\) is the total number of months. When the return rate is 0%, the formula simply divides the goal evenly across all months.

Worked example

Suppose you want $20,000 in 5 years at a 6% annual return. Then \(i = 0.06/12 = 0.005\) and \(n = 60\). $$\text{PMT} = 20{,}000 \times \frac{0.005}{(1.005)^{60} - 1} = \frac{100}{0.34885} \approx \$286.66 \text{ per month}$$ Over 60 months you contribute about $17,199, and roughly $2,801 comes from investment growth.

FAQ

Does it assume deposits at the start or end of the month? It assumes end-of-month deposits (an ordinary annuity), the most common convention.

What return rate should I use? Use a realistic long-term average for your investment mix. A high-yield savings account may be 4–5%, while a diversified stock portfolio has historically averaged around 7% before inflation.

What if I set the rate to 0%? The calculator divides your goal evenly across all months, giving the deposit needed with no growth.