What this calculator does

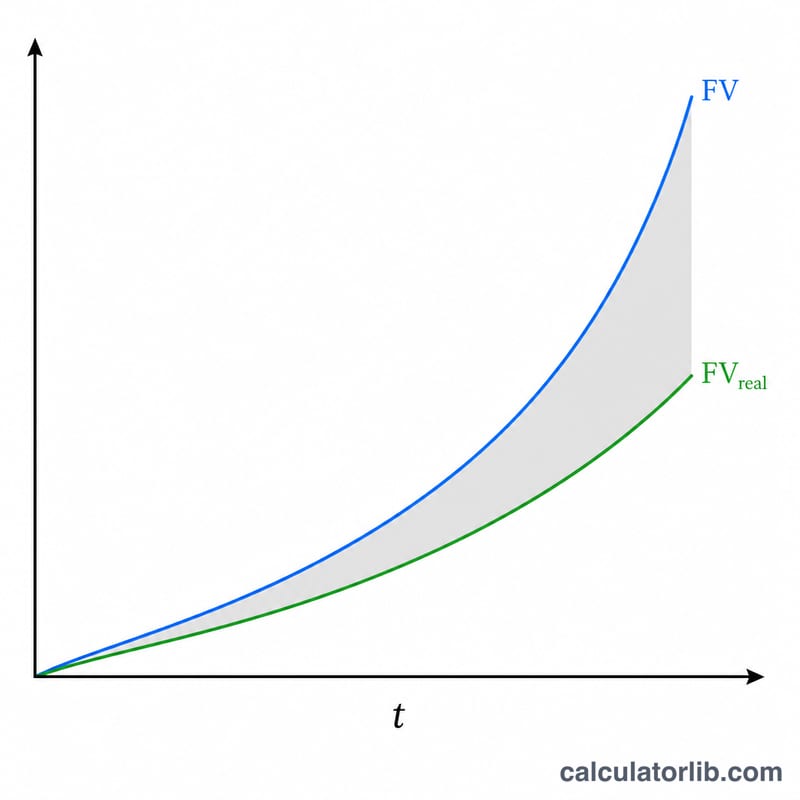

The Investment Inflation Calculator shows how inflation erodes the buying power of an investment that earns compound interest and may also receive regular deposits or withdrawals. It runs in two modes. In "The Return on an Investment" you enter an initial investment (present value) and it returns both the nominal future value and that value expressed in today's dollars. In "Investment Required for a Target Return" you enter a goal stated in today's purchasing power and it computes the initial investment you need now. The math is universal time-value-of-money; the currency symbol is illustrative.

How to use it

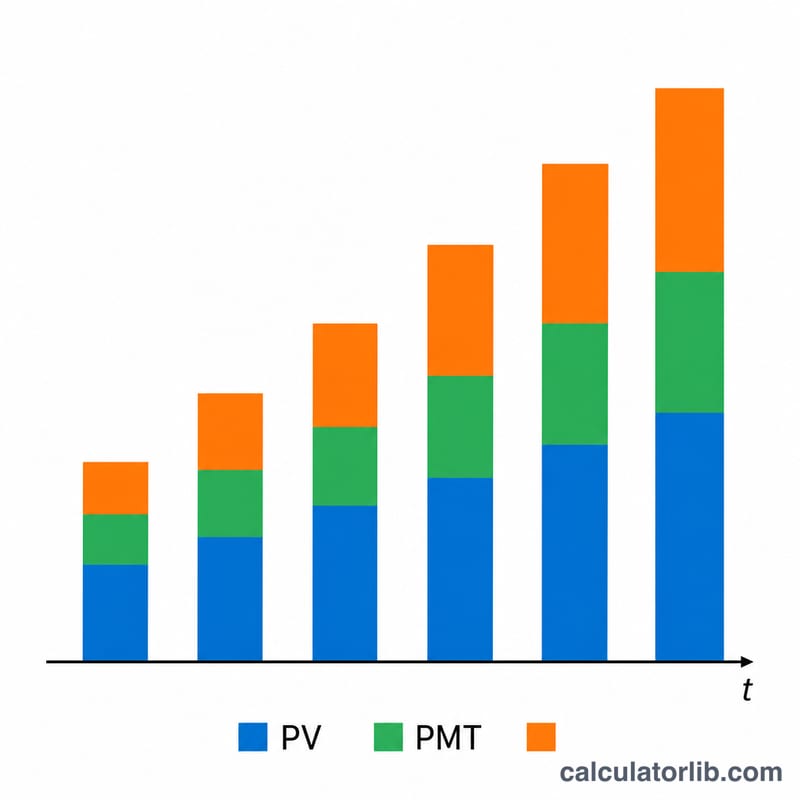

Pick a mode, then enter the dollar amount, the number of years, the annual interest rate, how often interest compounds, and the expected inflation rate. Optionally add a recurring deposit or withdrawal and choose its frequency. The tool aligns payment frequency with compounding by deriving an equivalent rate per payment period, so weekly deposits with monthly compounding are handled correctly.

The formula explained

The lump sum grows by \(FV = PV(1 + r/m)^{mt}\), where r is the annual rate, m is compoundings per year and t is years. Periodic payments form an ordinary annuity valued with an equivalent payment-period rate \(r_{pay} = (1 + r/m)^{m/q} - 1\) over \(N = q \cdot t\) payments. Deposits add and withdrawals subtract. Finally the nominal total is deflated by \((1 + i)^{t}\) to express it in today's dollars.

Worked example

Goal mode, target $100,000 in today's dollars, 10 years, 6.25% rate compounded monthly, 2.25% inflation, no payments. Nominal target $$= 100{,}000 \times (1.0225)^{10} = \$124{,}920.34.$$ Required PV $$= 124{,}920.34 \div (1 + 0.0625/12)^{120} = 124{,}920.34 \div 1.865435 = \mathbf{\$66{,}973.58}.$$ So investing about $66,974 today reaches $100,000 of purchasing power in ten years.

FAQ

Why is the inflation-adjusted value lower? Inflation means future dollars buy less, so the real value is the nominal balance divided by cumulative inflation.

What if my deposit frequency differs from compounding? The calculator converts the rate to an equivalent per-payment rate, so any combination works.

Can withdrawals make the result negative? Yes — if withdrawals outpace growth the future value can go negative, and the result is shown as computed.