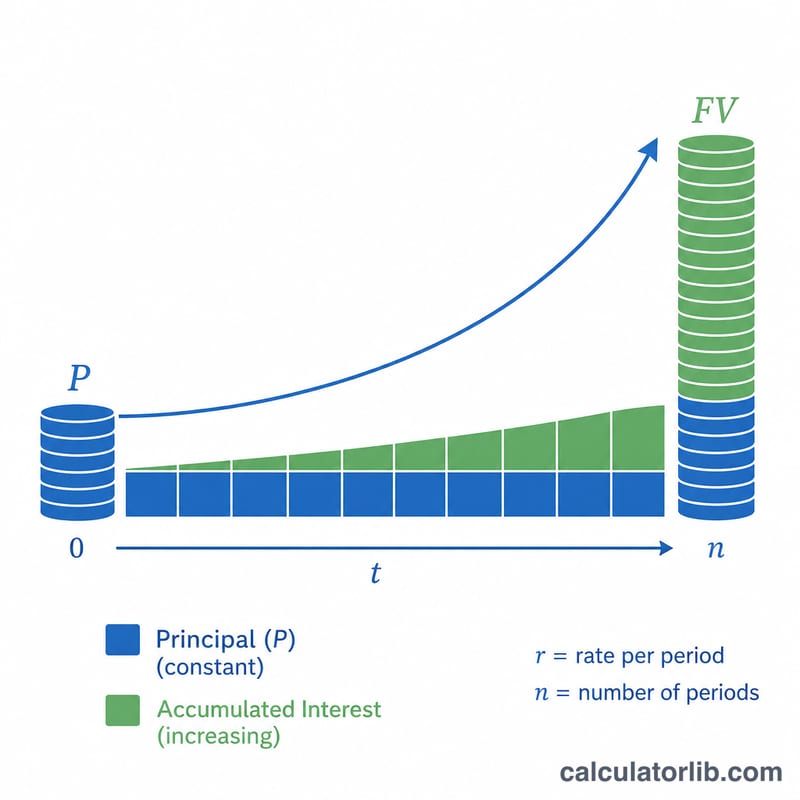

What is a Lumpsum Investment Calculator?

A lumpsum investment calculator estimates how much a single, one-time investment will grow to over a chosen period, given an expected annual return and a compounding frequency. Unlike a SIP (where you invest periodically), a lumpsum is invested all at once and left to compound.

How to use it

Enter the amount you invest today, your expected annual return rate, the number of years you plan to stay invested, and how often returns compound (annually, quarterly, monthly, etc.). The calculator returns the projected future value plus the total gains earned over and above your invested amount.

The formula explained

The tool uses the standard compound interest equation: $$\text{FV} = \text{P} \times \left(1 + \frac{r}{n}\right)^{n \times t}$$ where P is the principal, r is the annual rate as a decimal, n is the number of compounding periods per year, and t is the number of years. More frequent compounding (larger \(n\)) produces a slightly higher future value for the same nominal rate.

Worked example

Invest ₹50,000 at 10% per year, compounded monthly, for 5 years. Here P = 50000, r = 0.10, n = 12, t = 5. So $$\text{FV} = 50000 \times \left(1 + \frac{0.10}{12}\right)^{60} = 50000 \times (1.008333\ldots)^{60} \approx ₹82{,}265.45$$ Total returns ≈ ₹32,265.45.

FAQ

Does compounding frequency matter? Yes — for the same nominal rate, monthly compounding yields a bit more than annual compounding because interest is added more often.

Is the result guaranteed? No. It is a projection based on a constant assumed return; actual market returns vary year to year.

What rate should I use? Use a realistic long-term expected return for your asset class rather than a single good year's performance.