What Is the Combined Ratio?

The combined ratio is the key profitability metric for property and casualty insurers. It measures total underwriting costs — incurred losses (claims) plus operating expenses — as a percentage of earned premium. A combined ratio below 100% means the insurer earned an underwriting profit; above 100% means it paid out more in claims and expenses than it collected in premium, relying on investment income to stay profitable.

How to Use This Calculator

Enter three figures for a period: incurred losses (claims paid plus reserve changes), expenses (commissions, administration, acquisition costs), and earned premium (premium attributable to coverage actually provided). The calculator returns the combined ratio along with its two components — the loss ratio and the expense ratio.

The Formula Explained

$$\text{Combined Ratio} = \frac{\text{Incurred Losses} + \text{Expenses}}{\text{Earned Premium}} \times 100\%$$ Equivalently, it is the sum of the loss ratio (losses ÷ premium) and the expense ratio (expenses ÷ premium). This is the "trade basis" combined ratio commonly cited in financial statements.

Worked Example

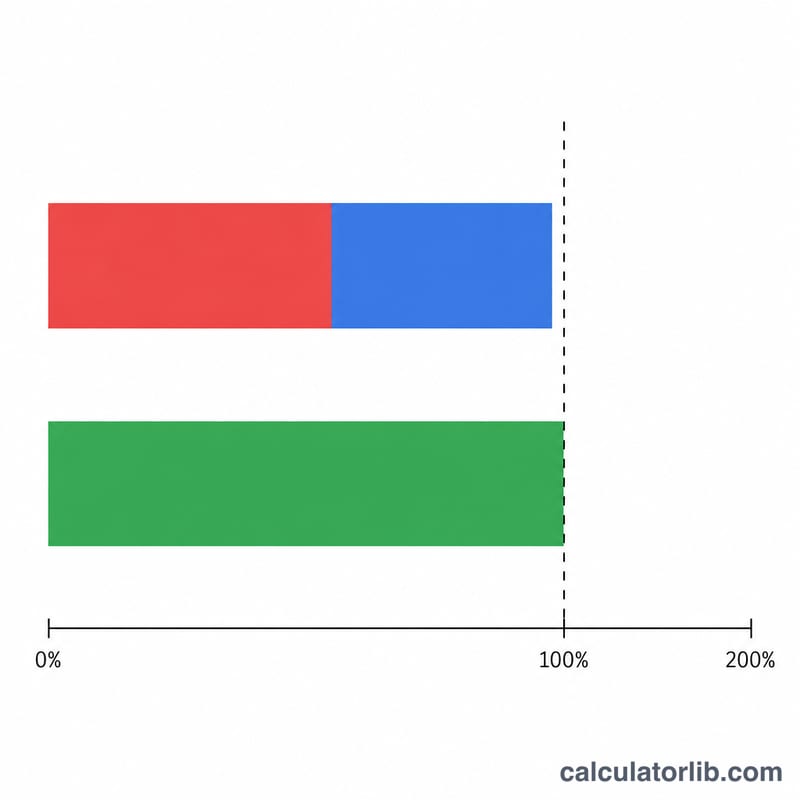

An insurer has $650,000 in incurred losses, $300,000 in expenses, and $1,000,000 in earned premium. Loss ratio \( = 650{,}000 \div 1{,}000{,}000 = 65\% \). Expense ratio \( = 300{,}000 \div 1{,}000{,}000 = 30\% \). $$\text{Combined Ratio} = 65\% + 30\% = \mathbf{95\%}$$ indicating a 5-cent underwriting profit on every premium dollar.

FAQ

Is a lower combined ratio better? Yes. A lower ratio means more of each premium dollar is retained as underwriting profit.

Can the combined ratio exceed 100% and still be acceptable? Yes — insurers with strong investment returns can run above 100% and remain profitable overall.

What's a good combined ratio? Consistently below 100% is excellent; the long-run industry average tends to hover near 95–105%.