What Is the Hedge Ratio?

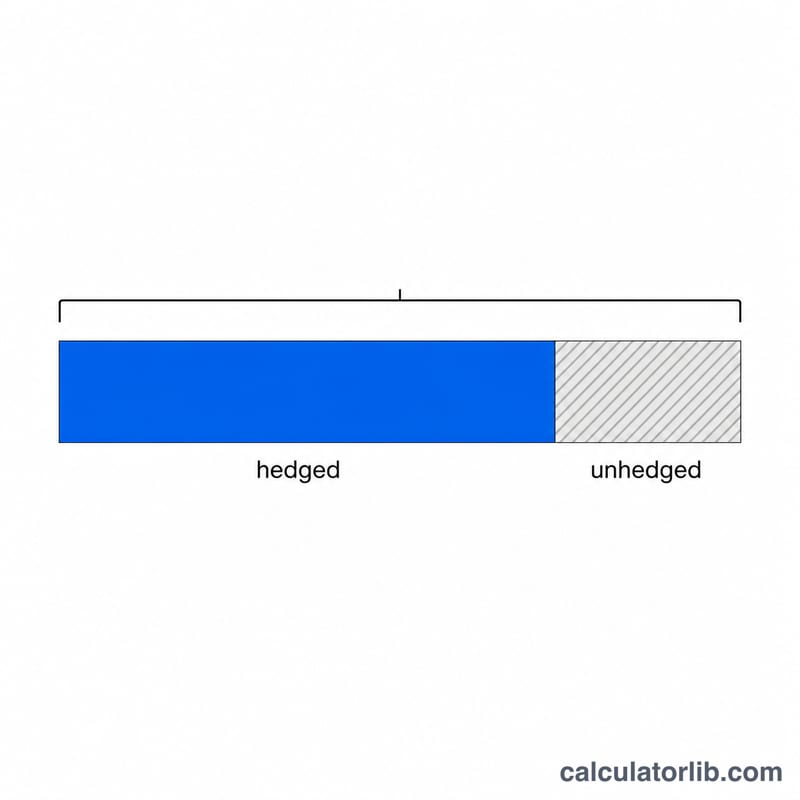

The hedge ratio measures how much of a position's total exposure is offset by a hedge. It is the value being hedged divided by the total value at risk. A hedge ratio of 1.0 (100%) means the position is fully hedged, while 0.0 means it is completely unhedged. Investors, treasurers, and risk managers use it to quantify how protected a portfolio, commodity position, or foreign-currency cash flow is against adverse price moves.

How to Use This Calculator

Enter the dollar value you have hedged (for example, the notional of futures or options contracts you hold) and the total exposure you want to protect. The calculator returns the hedge ratio as a decimal, the equivalent percentage, and the remaining unhedged exposure so you can see exactly how much risk is still open.

The Formula Explained

The core equation is simply:

$$\text{Hedge Ratio} = \frac{\text{Value Hedged (\$)}}{\text{Total Exposure (\$)}}$$

Multiply the result by 100 to express it as a percentage. The unhedged exposure is the total exposure minus the value hedged. The calculator guards against division by zero, so a total exposure of 0 returns a ratio of 0.

Worked Example

Suppose you hold $250,000 of a stock portfolio and you hedge $200,000 of it using index futures. The hedge ratio is $$200{,}000 \div 250{,}000 = 0.8,$$ or 80% hedged. The unhedged exposure is $$250{,}000 - 200{,}000 = \$50{,}000,$$ meaning a fifth of the position still moves freely with the market.

FAQ

What is a good hedge ratio? It depends on your risk appetite. A ratio near 1.0 minimizes price risk but can cap upside and add cost; many managers choose a partial hedge between 0.5 and 0.9.

Can the hedge ratio exceed 1? Yes. A ratio above 1.0 means you are over-hedged — the hedge is larger than the underlying exposure, which can create a net opposite position.

Does this account for correlation or beta? No. This is the simple value-based hedge ratio. A beta- or minimum-variance hedge ratio additionally scales by the correlation and volatility between the asset and the hedging instrument.