What Is the Optimal Hedge Ratio?

The optimal hedge ratio — also called the minimum-variance hedge ratio — tells you how much of a futures position you should hold per unit of the underlying spot position to minimise the variance (risk) of the combined position. It is a cornerstone of risk management for commodity producers, importers, and portfolio managers who use futures to offset price exposure.

The Formula Explained

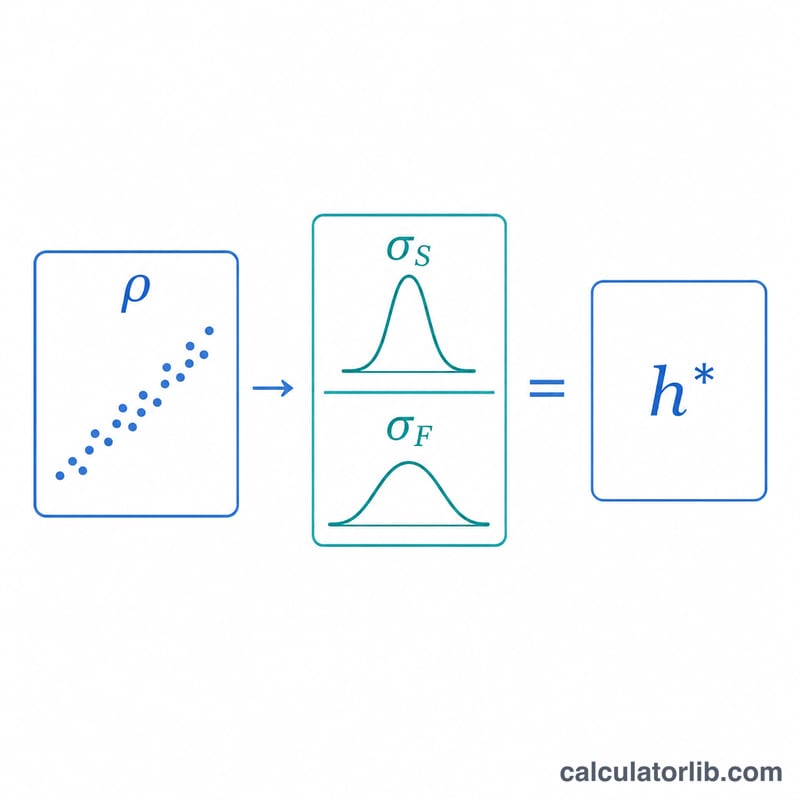

The hedge ratio is given by

$$h^{*} = \rho \times \frac{\sigma_S}{\sigma_F}$$where \(\rho\) is the correlation between changes in the spot price and changes in the futures price, \(\sigma_S\) is the standard deviation of spot price changes, and \(\sigma_F\) is the standard deviation of futures price changes. Intuitively, you scale by how volatile the spot is relative to the futures, then dampen the result by how tightly the two move together. A perfect 1.0 correlation with equal volatilities gives a hedge ratio of exactly 1.

How to Use the Calculator

Enter the estimated correlation (between -1 and 1), the standard deviation of spot price changes, and the standard deviation of futures price changes. Optionally enter the size of the position you are hedging and the futures contract size to get the recommended number of contracts. The tool also reports the proportion of variance eliminated by the hedge, which equals \(\rho^{2}\).

Worked Example

Suppose an airline expects jet fuel volatility of \(\sigma_S = 0.04\) and hedges with heating-oil futures of volatility \(\sigma_F = 0.05\), with a correlation of \(\rho = 0.8\). Then

$$h^{*} = 0.8 \times \frac{0.04}{0.05} = 0.8 \times 0.8 = 0.64$$The airline should hold futures equal to 64% of its spot exposure. The hedge removes \(\rho^{2} = 0.64 = 64\%\) of the price variance.

FAQ

Can the hedge ratio exceed 1? Yes — if spot price changes are more volatile than futures (\(\sigma_S > \sigma_F\)) and correlation is high, \(h^{*}\) can be greater than 1.

What does a negative result mean? A negative correlation produces a negative hedge ratio, meaning you would take the same direction in futures rather than the opposite to offset risk.

How much risk does an optimal hedge remove? The optimal hedge removes a fraction \(\rho^{2}\) of the variance; the rest is unavoidable basis risk.