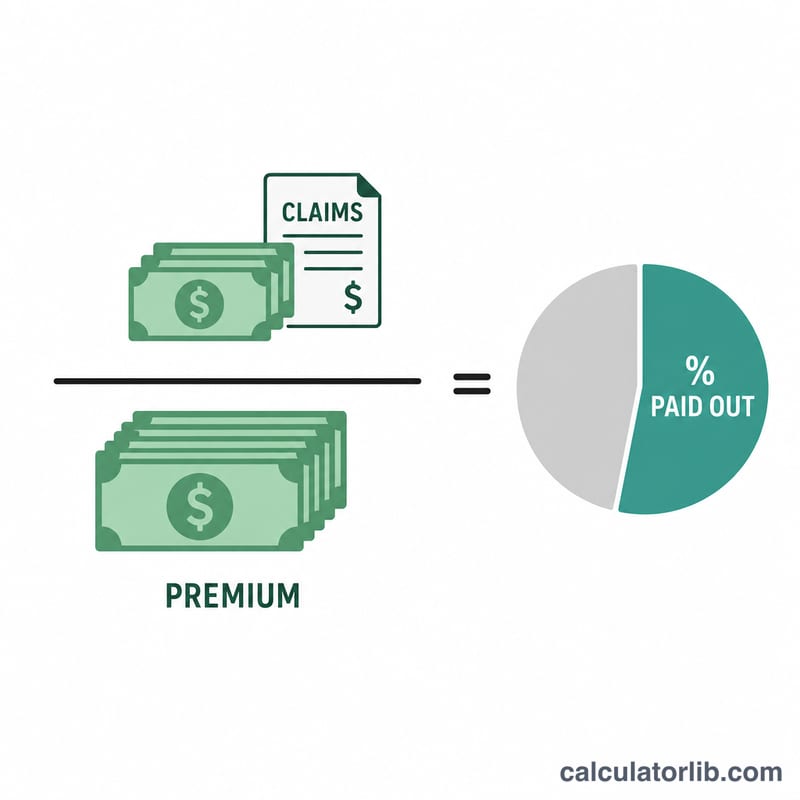

What Is the Loss Ratio?

The loss ratio is a key insurance metric that measures the proportion of earned premiums an insurer pays out in claims (incurred losses). It tells you, for every dollar of premium collected, how much went toward covering losses. A lower loss ratio generally indicates better underwriting profitability, while a ratio above 100% means claims exceeded premiums.

How to Use This Calculator

Enter the total incurred losses (claims paid plus reserves and adjustment expenses) and the earned premiums for the period. The calculator instantly returns the loss ratio as a percentage. Use consistent time periods and currency for both figures.

The Formula Explained

The formula is straightforward:

$$\text{Loss Ratio} = \frac{\text{Incurred Losses}}{\text{Earned Premiums}} \times 100\%$$

Incurred losses include paid claims plus changes in loss reserves. Earned premiums represent the portion of written premiums that corresponds to coverage already provided during the period.

Worked Example

Suppose an insurer paid $65,000 in incurred losses and earned $100,000 in premiums. The loss ratio is:

$$\left(65{,}000 \div 100{,}000\right) \times 100\% = \mathbf{65\%}$$

This means 65 cents of every premium dollar went to claims, leaving 35 cents toward expenses and profit.

FAQ

What is a good loss ratio? It varies by line of business, but many insurers target a loss ratio between 40% and 60%, leaving room for expenses and profit margin.

What does a loss ratio over 100% mean? The insurer paid out more in claims than it collected in premiums for that period — an unprofitable underwriting result.

How does loss ratio differ from the combined ratio? The combined ratio adds the expense ratio to the loss ratio, giving a fuller picture of underwriting profitability.