What this calculator does

This tool tells you how long it will take for a lump-sum investment or savings balance to grow from a starting amount to a chosen target, assuming a fixed annual interest rate that compounds a set number of times per year. It rearranges the standard compound-interest formula to solve for time, so instead of guessing a year and checking, you get the exact duration directly.

How to use it

Enter your starting amount (P), the target amount you want to reach (A), the annual interest rate as a percentage, and how often interest compounds (annually, monthly, daily, etc.). The calculator returns the time in years, plus a rounded years-and-months breakdown and the total number of months.

The formula explained

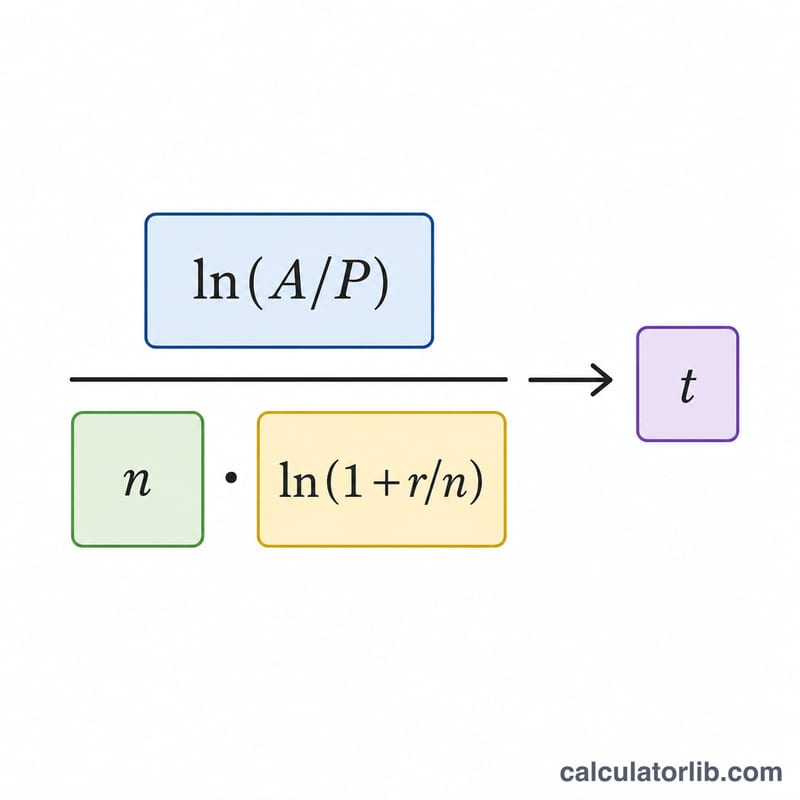

The growth formula is $$A = P\left(1 + \frac{r}{n}\right)^{nt}.$$ Solving for t gives $$t = \frac{\ln\!\left(\frac{A}{P}\right)}{n \cdot \ln\!\left(1 + \frac{r}{n}\right)},$$ where r is the rate as a decimal (\(5\% = 0.05\)) and n is compounds per year. The natural logarithm (ln) appears because we are undoing an exponential growth process.

Worked example

Suppose you invest $1,000 and want to reach $2,000 at 5% interest compounded monthly (\(n = 12\)). Here \(r/n = 0.05/12 \approx 0.0041667\), and \(\ln(1.0041667) \approx 0.0041580\). So $$t = \frac{\ln(2)}{12 \times 0.0041580} = \frac{0.693147}{0.049896} \approx 13.89 \text{ years}$$ — roughly 13 years and 11 months.

FAQ

Does this include regular contributions? No — it assumes a single lump sum with no deposits or withdrawals. For ongoing contributions you'd need a future-value-of-an-annuity model.

Why does compounding frequency matter? More frequent compounding earns slightly more interest per year, so a higher n reaches the target marginally faster at the same nominal rate.

What if the rate is 0%? With no growth the balance never increases, so no finite time can reach a higher target; the calculator requires a positive rate.