What Is a Reverse Compound Interest Calculator?

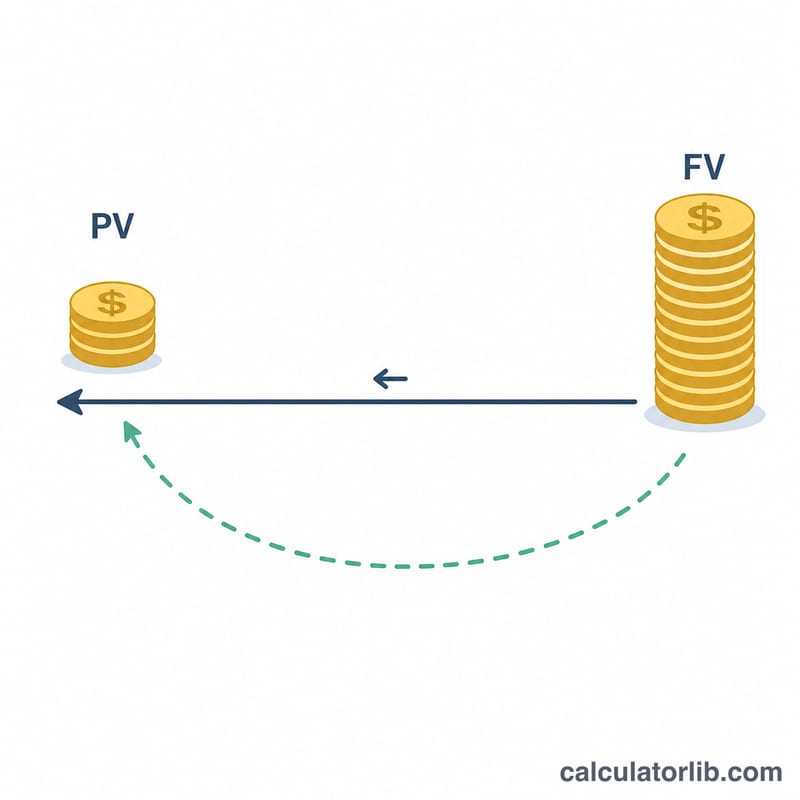

A Reverse Compound Interest Calculator works backwards from a target amount. Instead of asking "how much will my money grow to?", it asks "how much do I need to invest today to reach a specific future value?" That starting amount is called the present value (PV), and finding it is known as discounting.

This tool is useful anywhere in the world and is not tied to any single country's tax rules. It applies to savings goals, lump-sum investments, sinking funds, education planning, and any situation where you know your target and want to know the deposit required today.

How to Use It

Enter the following four inputs:

- Future value – the amount you want to have at the end.

- Annual interest rate – the expected yearly return, as a percentage.

- Years – how long the money will grow.

- Compounding frequency – how often interest is added (annually, quarterly, monthly, or daily).

The calculator returns the required present value, the total interest earned over the period, and the effective annual rate (EAR).

The Formula Explained

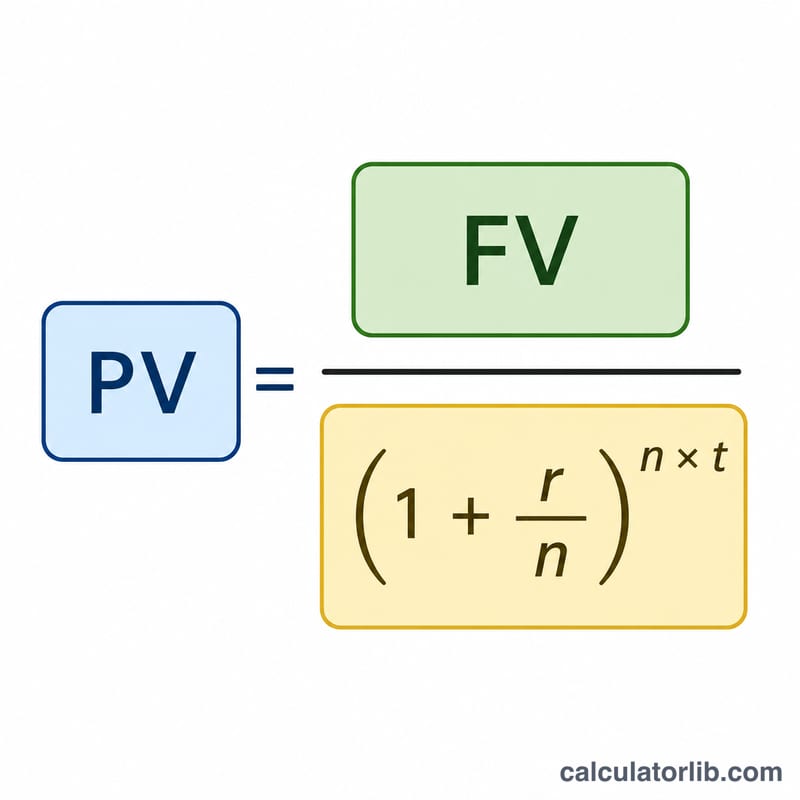

The present value is found by reversing the standard compound interest formula:

$$PV = \dfrac{FV}{\left(1 + \dfrac{r}{n}\right)^{n \cdot t}}$$Where FV is the future value, r is the annual rate (as a decimal), n is the number of compounding periods per year, and t is the number of years. Total interest is simply \(FV - PV\). The effective annual rate is $$EAR = \left(1 + \dfrac{r}{n}\right)^{n} - 1$$ which shows the true yearly return once compounding is included.

Worked Example

Suppose you want $20,000 in 5 years, earning 6% compounded monthly. Here \(r = 0.06\), \(n = 12\), \(t = 5\), so \(n \times t = 60\) periods and \(r/n = 0.005\).

$$PV = \dfrac{20{,}000}{(1.005)^{60}} = \dfrac{20{,}000}{1.34885} \approx \$14{,}827$$You would need to invest about $14,827 today, earning roughly $5,173 in interest. The EAR is \((1.005)^{12} - 1 \approx 6.17\%\).

Frequently Asked Questions

What is reverse compound interest?

Reverse compound interest works backward from a future goal to find the present value you need today. Instead of growing a deposit forward, it discounts the future amount using the interest rate, time period, and compounding frequency to reveal the single lump sum required now.

What formula does the reverse compound interest calculator use?

It uses the present value formula PV = FV / (1 + r/n)^(n*t), where FV is the future value, r is the annual rate as a decimal, n is the number of compounding periods per year, and t is the number of years. This discounts your target back to today.

Why does compounding frequency matter?

More frequent compounding means interest earns interest sooner, so you need a slightly smaller deposit to reach the same target. Daily compounding requires less upfront than annual compounding for an identical future value, because more periods of growth do more of the work for you.

Can I use this calculator to find a required savings deposit?

Yes. Enter your savings goal as the future value, your expected annual interest rate, the number of years, and how often interest compounds. The calculator returns the lump sum you must deposit today to reach that goal, plus total interest earned and the effective annual rate.

What is the effective annual rate shown in the results?

The effective annual rate (EAR) converts a nominal rate with intra-year compounding into the true yearly return. It is calculated as (1 + r/n)^n - 1. EAR lets you compare accounts with different compounding frequencies on an equal, annual basis.

Does this account for inflation or regular contributions?

No. The result is a nominal present value for a single lump sum. It does not adjust for inflation, so run a separate inflation calculation to find purchasing power. Recurring deposits need an annuity present value formula rather than this single-sum method.