What this calculator does

The Compound Interest Calculator finds the future value (accrued amount) and total interest earned on a deposit or investment. It supports periodic compounding (annually, semiannually, quarterly, monthly, semimonthly, biweekly, weekly, or daily), continuous compounding, and a simple-interest mode. The math is universal — it applies the same way anywhere and involves no national tax or calendar rules. Currency is a display-only passthrough.

How to use it

Enter the starting Principal (P), the Annual Interest Rate (R) as a percentage, and the Time (t) in years. Pick a Compounding Frequency and an Interest Type (compound or simple). The calculator returns the future value, the total interest earned, and the effective annual rate (APY).

The formula explained

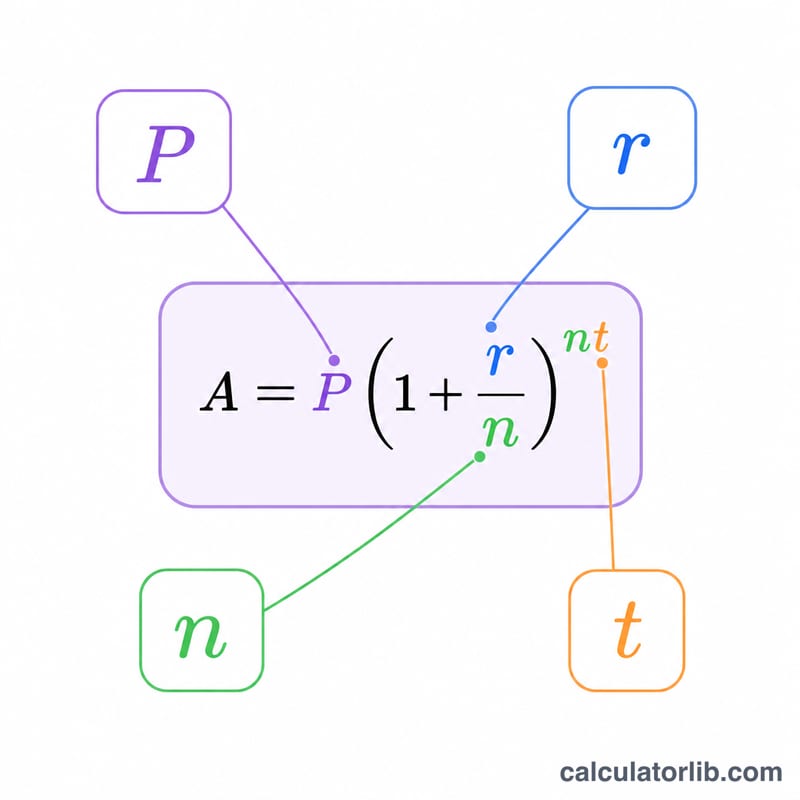

Let \(r = R/100\) be the decimal rate, \(t\) the years, \(P\) the principal, and \(n\) the number of compounding periods per year. For periodic compounding, $$A = P\left(1 + \frac{r}{n}\right)^{n \cdot t}$$ and the interest is \(I = A - P\). For continuous compounding, $$A = P \cdot e^{r \cdot t}.$$ The effective annual rate (APY) is \(\text{EAR} = \left(1 + \frac{r}{n}\right)^n - 1\) for periodic, or \(e^r - 1\) for continuous. In simple-interest mode, \(I = P \cdot r \cdot t\) and \(A = P(1 + r \cdot t)\), so APY equals the nominal rate.

Worked example

With \(P = 5000\), \(R = 5\%\) (\(r = 0.05\)), \(t = 10\) years, compounded monthly (\(n = 12\)): $$A = 5000 \times \left(1 + \frac{0.05}{12}\right)^{12 \times 10} = 5000 \times 1.647009 \approx \mathbf{8235.05}.$$ Total interest = \(8235.05 - 5000 = 3235.05\). APY = \(\left(1 + \frac{0.05}{12}\right)^{12} - 1 \approx 5.1162\%\).

FAQ

How does compounding frequency affect returns? More frequent compounding yields slightly more interest. Monthly beats annual, daily beats monthly, and continuous compounding is the theoretical maximum for a given nominal rate.

What is APY? The Effective Annual Rate (APY) is the true yearly yield once compounding is included. It is always at least the nominal rate and approaches \(e^r - 1\) as frequency increases.

When should I use simple interest? Use simple interest when interest is not added back to the balance — interest is computed only on the original principal each period.