What Is Compound Interest?

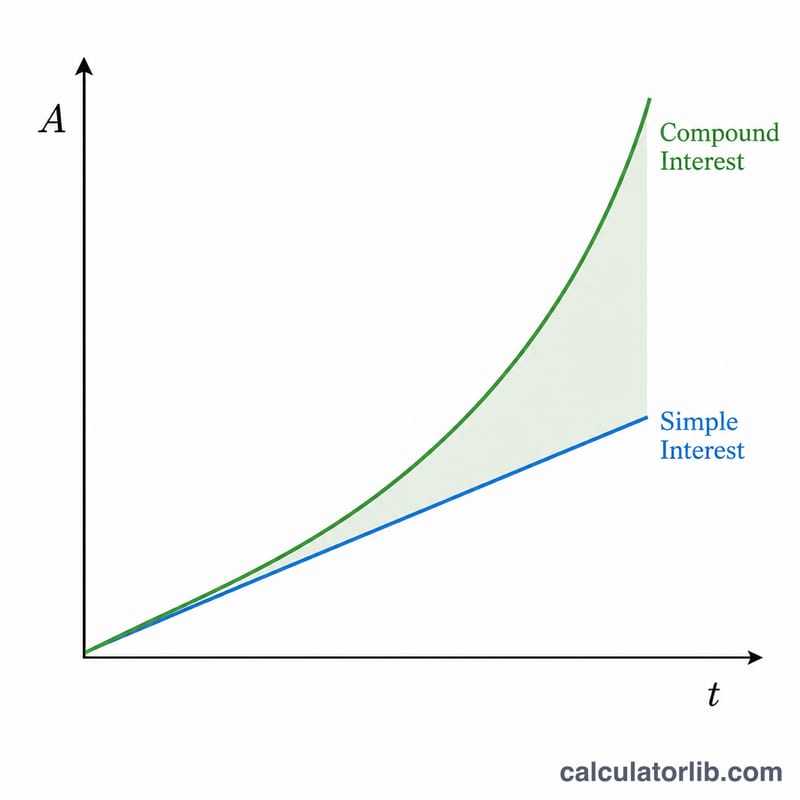

Compound interest is interest calculated on both the initial principal and the accumulated interest from previous periods. Unlike simple interest, which grows linearly, compound interest grows exponentially — earning "interest on interest." This makes it the foundation of savings accounts, investments, and many loans. This calculator is a universal math tool and applies anywhere; it does not include taxes or fees.

How to Use This Calculator

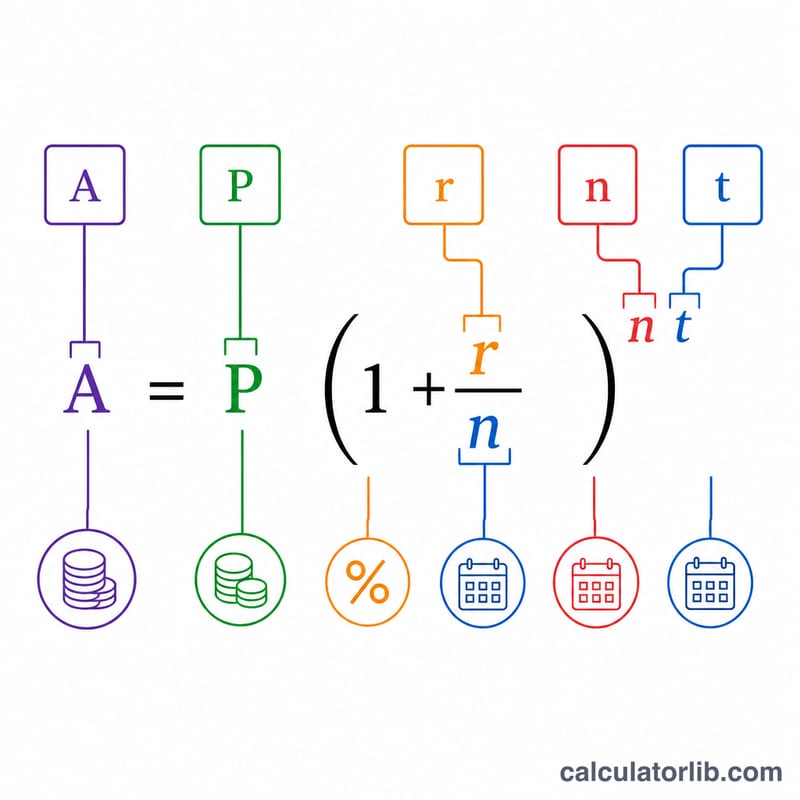

Enter four values: the Principal (P) you start with, the annual interest rate as a percentage, the number of times interest is compounded per year (n) (1 = annually, 4 = quarterly, 12 = monthly, 365 = daily), and the time in years (t). The calculator returns the future value \(A\) and the total interest earned.

The Formula Explained

The compound interest formula is:

$$A = P\left(1 + \dfrac{r}{n}\right)^{nt}$$

Here r is the annual rate as a decimal (5% = 0.05). Dividing \(r\) by \(n\) gives the rate per period, and raising to the power of \(n\cdot t\) accounts for every compounding period over the full term. Subtracting the principal gives the interest earned: \(I = A - P\).

Worked Example

Suppose you invest $10,000 at 5% compounded monthly for 10 years. Then \(P = 10000\), \(r = 0.05\), \(n = 12\), \(t = 10\). Compute \((1 + 0.05/12) = 1.0041667\), raised to the 120th power \(\approx 1.647009\). Multiply by 10000 to get \(A \approx \$16{,}470.09\), so the interest earned is about $6,470.09.

$$A = 10000\left(1 + \dfrac{0.05}{12}\right)^{12\times 10} \approx \$16{,}470.09$$FAQ

Does more frequent compounding earn more? Yes — daily compounding earns slightly more than annual, though the difference shrinks as frequency rises toward continuous compounding.

What if interest is added once a year? Set \(n = 1\); the formula simplifies to \(A = P(1 + r)^{t}\).

Can I use this for loans? Yes, it shows how a debt grows if no payments are made, but it does not model regular repayments.