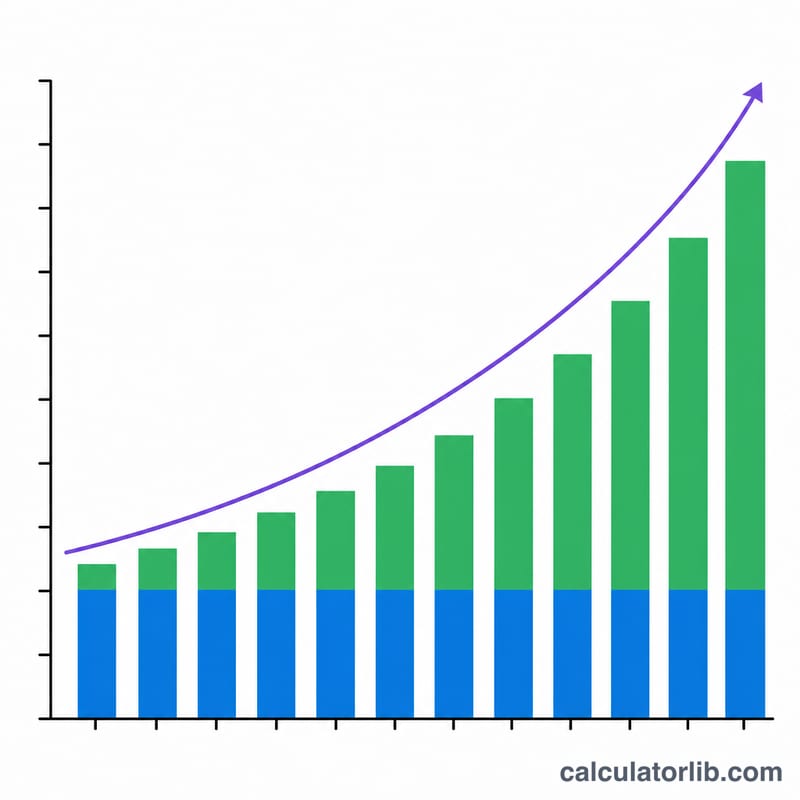

What Is the Compound Savings Calculator?

This tool projects how much a savings account or investment will grow over time when you combine an initial lump sum, regular ongoing deposits, and compound interest. Compounding means the interest you earn also earns interest, so the longer your money stays invested, the faster it accelerates. The calculator is universal — it works with any currency — and assumes deposits are made at the end of each compounding period (an ordinary annuity).

How to Use It

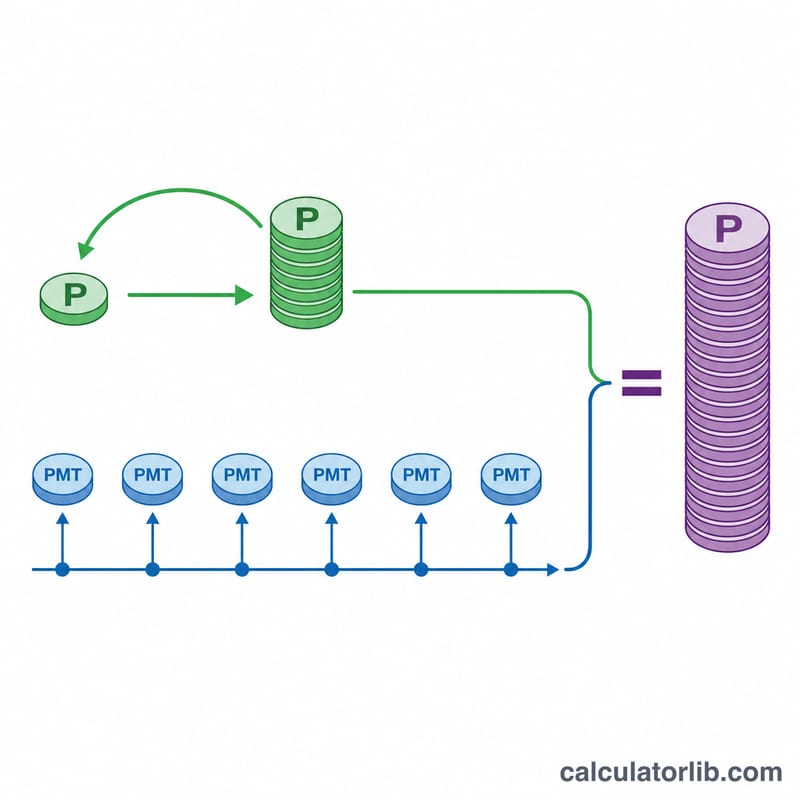

Enter your initial deposit (the money you start with), the regular deposit you add each period, the annual interest rate as a percentage, the number of years, and how often interest compounds and deposits are made. The result shows your future value, the total of everything you put in, and the interest earned on top.

The Formula Explained

The future value combines two parts. The first, \(P(1+r)^{n}\), grows your starting balance. The second, \(PMT\cdot\dfrac{(1+r)^{n}-1}{r}\), is the future value of a stream of equal deposits. Here \(r\) is the periodic rate (annual rate ÷ frequency) and \(n\) is the total number of periods (frequency × years). If the rate is zero, the formula simplifies to principal plus all deposits.

$$FV = P\,(1+r)^{n} + D\cdot\frac{(1+r)^{n}-1}{r}$$ $$\text{where}\quad \left\{ \begin{aligned} P &= \text{Initial Deposit} \\ D &= \text{Regular Deposit} \\ r &= \dfrac{\text{Rate (\%)}}{100 \times \text{Frequency}} \\ n &= \text{Frequency} \times \text{Years} \end{aligned} \right.$$

Worked Example

Start with 1,000 at 5% annual interest, compounded monthly, adding 100 per month for 10 years. The periodic rate is \(0.05/12 \approx 0.0041667\) and there are 120 periods. Your balance grows to roughly 17,175 — about 13,000 contributed and over 4,000 in interest.

FAQ

Does it assume deposits at the start or end of the period? The end of each period (ordinary annuity), the most common convention.

Can I model a one-time investment only? Yes — set the regular deposit to 0 and only the principal compounds.

Why does interest grow so much in later years? Because compound interest is exponential: each period's gains are added to the base that earns the next period's interest.