What Is Daily Compound Interest?

Daily compound interest means your interest is calculated and added to your balance every single day. Because each day's interest then earns interest itself, your money grows slightly faster than with monthly or annual compounding. This calculator uses a standard 365-day year to determine your future balance and the total interest earned on a deposit or investment.

How to Use It

Enter three values: your starting principal (the amount you deposit), the annual interest rate as a percentage, and the time in years. The calculator instantly returns the future value of your balance plus how much of that is interest. You can use decimals for the years field — for example, enter 0.5 for six months.

The Formula Explained

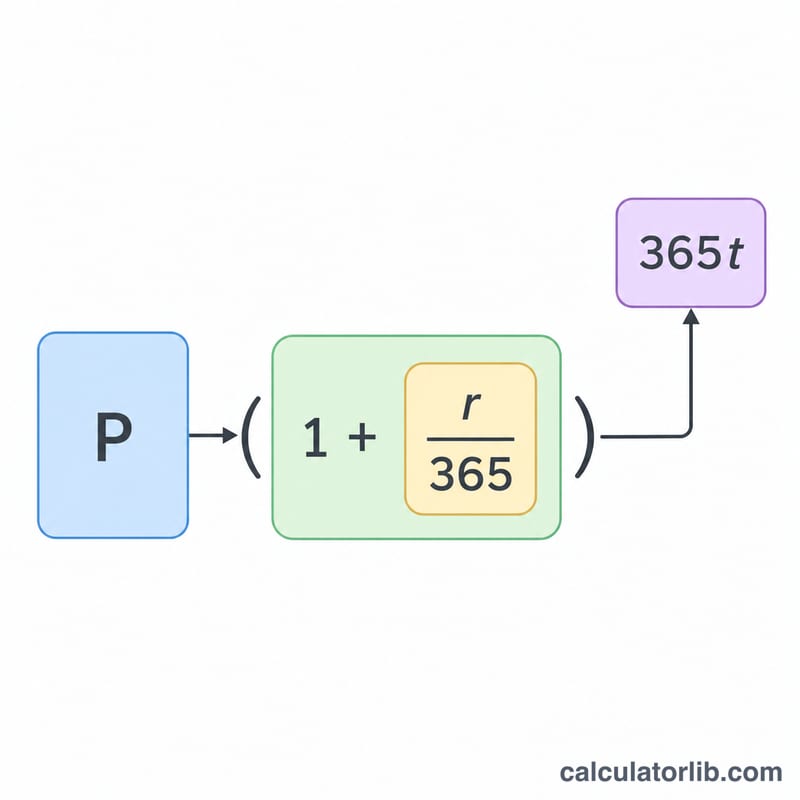

The growth follows the compound interest equation $$A = P \times \left(1 + \frac{r}{365}\right)^{365t}$$ Here \(P\) is the principal, \(r\) is the annual rate written as a decimal (so \(5\% = 0.05\)), and \(t\) is the number of years. Dividing the rate by 365 gives the daily rate, and raising it to the power of \(365t\) accounts for compounding on every day of the period.

Worked Example

Suppose you invest $10,000 at a 5% annual rate for 3 years. The daily rate is \(0.05 \div 365\), and the number of compounding periods is \(365 \times 3 = 1{,}095\). So $$A = 10{,}000 \times \left(1 + \frac{0.05}{365}\right)^{1095} \approx \$11{,}618.34$$ That means you earned about $1,618.34 in interest — slightly more than simple interest would give.

FAQ

Is daily compounding much better than monthly? Only marginally. At typical rates, daily compounding earns a tiny bit more than monthly, but the difference grows with higher rates and longer terms.

Does this account for taxes or fees? No. It shows gross growth only; taxes, fees, and inflation are not deducted.

Can I use it for loans? Yes — it shows how a balance grows if interest compounds daily and no payments are made, which is useful for understanding accruing debt.