What Is the Daily Interest Calculator?

This calculator shows how your savings grow when interest is compounded daily. Daily compounding means interest is added to your balance every single day, and the next day's interest is calculated on the slightly larger amount. Over time this "interest on interest" effect produces a higher return than simple interest or less frequent compounding.

How to Use It

Enter three values: your initial deposit (principal), the annual interest rate as a percentage, and the time in years. The tool returns your projected future balance along with the total interest earned over the period.

The Formula Explained

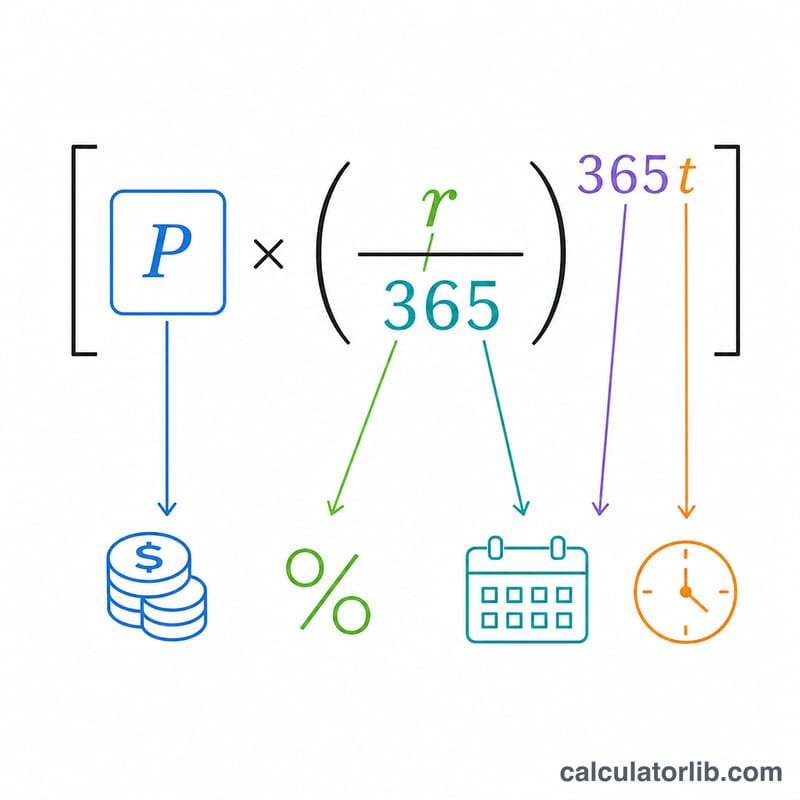

The growth follows the compound interest equation with 365 compounding periods per year:

$$A = P \times \left(1 + \frac{r}{365}\right)^{365 \cdot t}$$

Here A is the future balance, P is the principal, r is the annual rate written as a decimal (5% = 0.05), and t is the number of years. The interest earned is simply \(I = A - P\).

Worked Example

Suppose you deposit $10,000 at a 5% annual rate for 1 year with daily compounding. Then \(r = 0.05\) and \(365 \cdot t = 365\), so $$A = 10{,}000 \times \left(1 + \frac{0.05}{365}\right)^{365} \approx \$10{,}512.67$$ The interest earned is about $512.67 — slightly more than the $500 you'd get from simple interest, thanks to daily compounding.

FAQ

Does daily compounding beat monthly compounding? Yes, but only by a small margin. More frequent compounding always yields slightly more, with diminishing returns as frequency increases.

What rate should I enter? Use the stated annual interest rate (APR) of your savings account. If you have the APY instead, the result may differ slightly.

Are taxes included? No. This is a gross projection and does not account for taxes, fees, or additional deposits.