What This Calculator Does

Most credit card issuers compound interest daily rather than monthly. This calculator shows how much a carried balance actually costs by converting your card's APR into a daily periodic rate (DPR) and multiplying it across the number of days you hold the balance. It is useful for understanding the real price of paying late, carrying a balance between statements, or skipping a full payment.

How to Use It

Enter your current outstanding balance, your card's APR (Annual Percentage Rate, e.g. 19.99), and the number of days the balance is carried. The tool returns the daily periodic rate, the interest accrued per day, the total interest for the period, and your projected new balance.

The Formula Explained

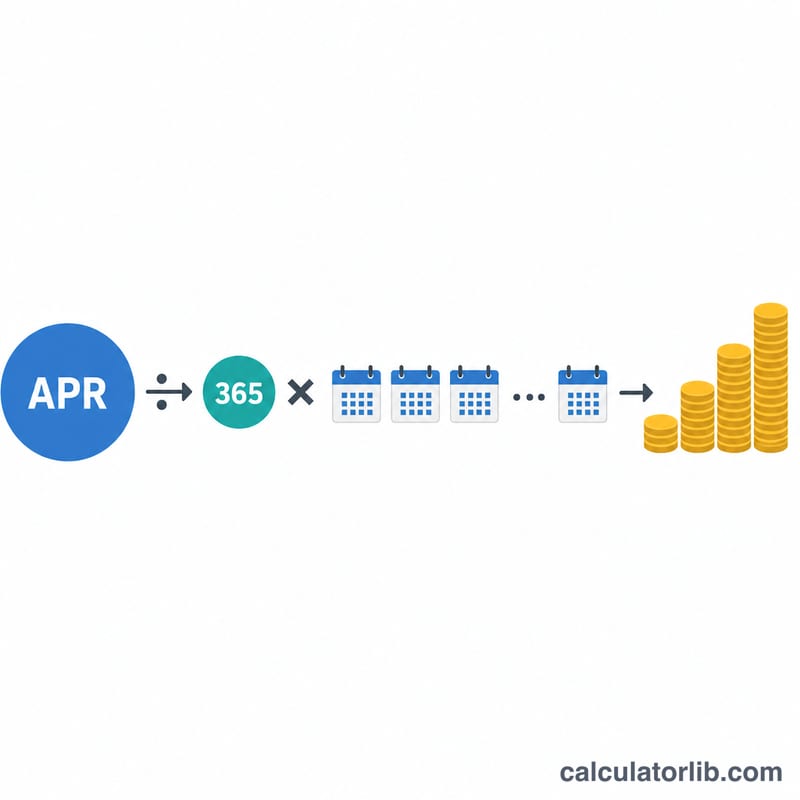

The daily periodic rate is simply the APR divided by 365: $$\text{DPR} = \frac{\text{APR}}{100 \times 365}$$ Each day's interest equals the balance times the DPR. Over a period you multiply that daily amount by the number of days:

$$\text{Interest} = \text{Balance} \times \frac{\text{APR \%}}{100 \times 365} \times \text{Days}$$This simple-interest model assumes a constant balance; real cards add new daily interest to the balance (compounding), so over long periods actual charges can be slightly higher.

Worked Example

Suppose you carry a $1,000 balance on a card with a 19.99% APR for 30 days. The daily periodic rate is \(19.99 / 100 / 365 = 0.0005477\). Daily interest is \($1{,}000 \times 0.0005477 = $0.5477\). Over 30 days that is about $16.43, bringing your balance to roughly $1,016.43.

FAQ

Is this simple or compound interest? It uses simple daily interest on a fixed balance. Actual cards usually compound the accrued interest into the balance each day, so this is a close but slightly conservative estimate.

Why divide by 365? Most US issuers use a 365-day year for the daily periodic rate; a few use 360. Adjust the APR slightly if your issuer uses a different convention.

How do I avoid this interest? Pay your statement balance in full each month within the grace period. Interest only applies when a balance is carried past the due date.