What Is the ACB Credit Card Interest Calculator?

This calculator estimates the interest (finance charge) a credit card issuer will add to your account for one billing cycle using the Average Daily Balance (ACB) method — the most common method used by card issuers. Instead of charging interest only on your closing balance, the ACB method charges interest on the average of your balance across every day of the billing cycle.

How to Use It

Enter three values: your average daily balance (the mean of each day's balance during the cycle), your card's APR as a percentage, and the number of days in the billing cycle (usually 28–31). The tool returns the interest charge, the daily periodic rate, the daily finance charge, and your projected new balance.

The Formula Explained

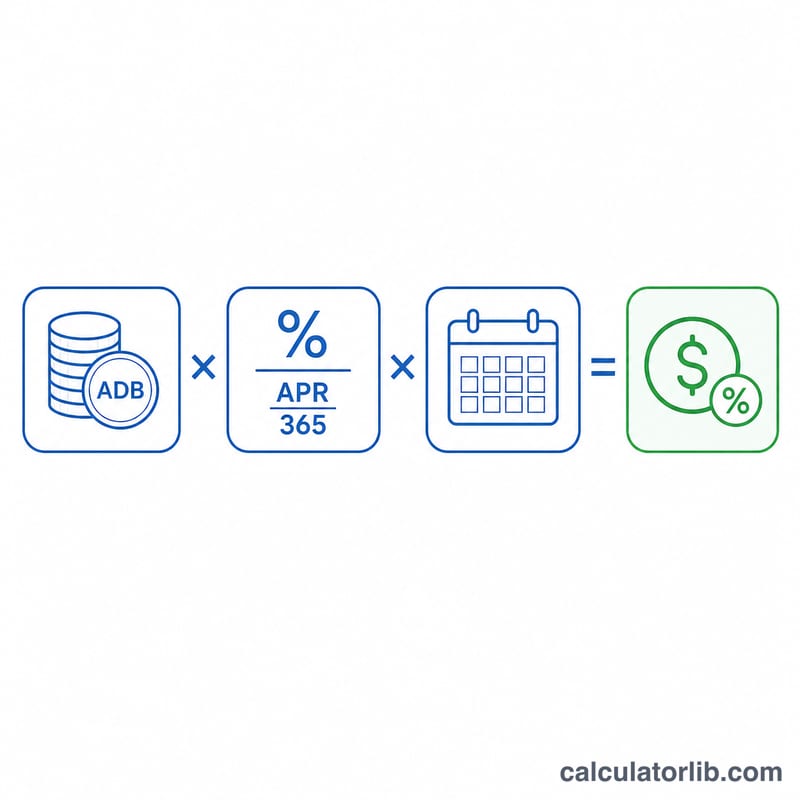

The math is simple. First, convert the APR to a daily periodic rate by dividing by 365: \(\text{DPR} = \frac{\text{APR}}{365}\). Then multiply that daily rate by your average daily balance and by the number of days in the cycle:

$$\text{Interest} = \text{Average Daily Balance} \times \frac{\text{APR}}{365} \times \text{Days in Cycle}$$

Most US issuers use a 365-day year for the daily rate even in leap years, which is the convention used here.

Worked Example

Suppose your average daily balance is $1,000, your APR is 19.99%, and the billing cycle is 30 days. The daily periodic rate is \(0.1999 \div 365 = 0.0005477\). Multiply: $$1{,}000 \times 0.0005477 \times 30 \approx \$16.43$$ in interest. Your new balance would be about $1,016.43.

Typical Credit Card APR Ranges

APRs vary widely by card type, the issuer, and the cardholder's creditworthiness. The ranges below reflect commonly published US averages and should be treated as general guidance, not guarantees. Your actual APR is disclosed in your card agreement and on your monthly statement.

| Card Type | Typical APR Range | Notes |

|---|---|---|

| Rewards / general purpose | ~18% – 28% | Cash-back and points cards; rates depend heavily on credit score. |

| Balance transfer | 0% intro, then ~17% – 26% | Promotional 0% periods (often 12–21 months) revert to a standard APR. |

| Store / retail | ~25% – 33% | Often among the highest standard APRs. |

| Secured | ~22% – 28% | For building or rebuilding credit; backed by a refundable deposit. |

| Cash advance | ~25% – 36% | Usually higher than the purchase APR, and interest typically accrues immediately with no grace period. |

Many cards carry variable APRs tied to the prime rate, meaning the rate can change over time. Always confirm the current rate before relying on any estimate.

Interpreting Your Result

The estimate is built from a few related quantities that appear on a typical credit card statement:

- Daily periodic rate (DPR). This is the APR divided by 365, expressed as a decimal. For a 19.99% APR, the DPR is \(19.99\% \div 365 \approx 0.05477\%\) per day. The issuer multiplies this rate by your balance each day of the cycle.

- Average daily balance. Rather than charging interest on a single snapshot, the ACB method sums your balance at the end of each day in the cycle and divides by the number of days. New purchases raise it; payments lower it.

- Finance charge. This is the dollar interest for the cycle — the average daily balance multiplied by the DPR and by the number of days. It is the number this calculator returns.

- Projected new balance. Your prior balance plus new purchases and the finance charge, minus payments and credits, equals the balance carried into the next cycle.

How it compounds month to month. If you carry a balance, this cycle's finance charge is added to the balance, and the following cycle's interest is calculated on that larger amount. Over time this compounding means unpaid interest itself begins to accrue interest, which is why a small monthly charge can grow substantially if only minimum payments are made.

The role of grace periods. Most cards offer a grace period on purchases: if you pay the statement balance in full by the due date, no interest is charged on purchases for that cycle. Carrying any balance typically forfeits the grace period until the balance is paid in full again. Cash advances and many balance transfers usually have no grace period, so interest accrues from the transaction date.

This section is general information about how credit card interest works and is not personal financial advice. Refer to your cardholder agreement for the exact terms that apply to your account.

FAQ

What counts as the average daily balance? Add up your balance for each day of the billing cycle (including new purchases, minus payments), then divide by the number of days in the cycle.

Can I avoid this interest? Yes — if you pay your statement balance in full by the due date, purchases typically have a grace period and accrue no interest. Carried balances and cash advances usually do not get a grace period.

Why divide by 365 and not 360? Most credit card issuers use 365 days for the daily periodic rate; some mortgages and other products use 360. This calculator uses 365 to match standard card practice.