What This Calculator Does

This calculator tells you the fixed monthly payment you need to make to completely pay off a credit card balance within a chosen number of months. Instead of guessing, you enter your current balance, your card's APR, and your target payoff timeline — and it computes the exact level payment that gets you to a zero balance on schedule, along with the total interest you'll pay.

How to Use It

Enter your current balance, the card's annual percentage rate (APR), and the number of months in which you want to be debt-free. The result shows your required monthly payment, the total amount paid over that period, and the total interest cost. Shortening the timeline raises the payment but lowers total interest; lengthening it does the opposite.

The Formula Explained

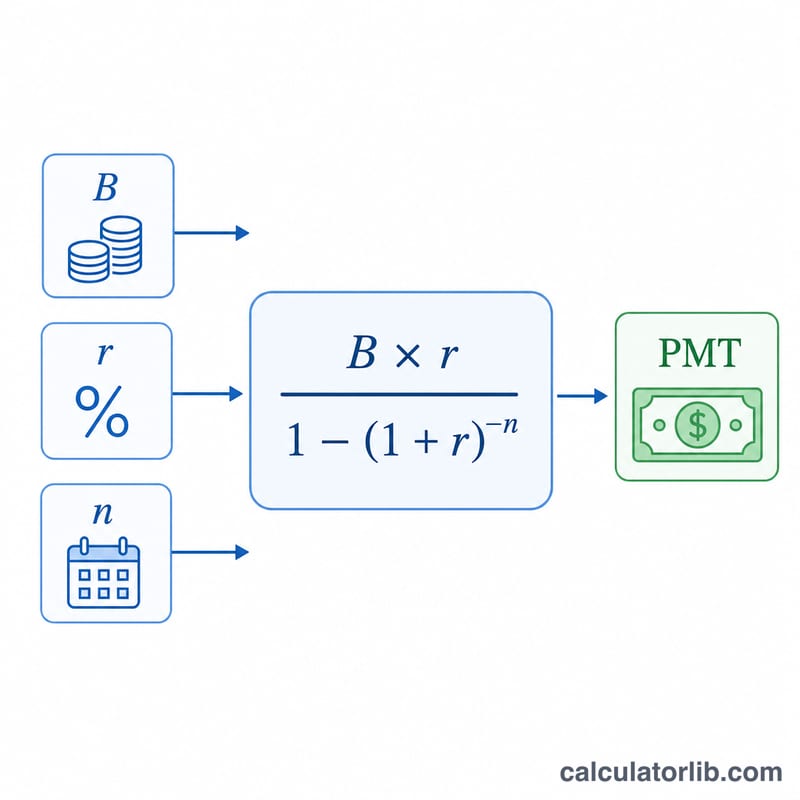

The calculation uses the standard amortizing-loan payment formula:

$$\text{PMT} = \frac{B \times r}{1 - (1 + r)^{-n}}$$Here B is the balance, r is the monthly interest rate (the APR divided by 12, expressed as a decimal), and n is the number of months. If the APR is 0%, the payment is simply the balance divided by the number of months.

Worked Example

Suppose you owe $5,000 at an 18% APR and want to be debt-free in 24 months. The monthly rate is \(0.18 / 12 = 0.015\). The payment is

$$\frac{5000 \times 0.015}{1 - 1.015^{-24}} = \frac{75}{0.30115} \approx 249.62 \text{ per month}$$Over 24 months you pay about $5,990.96, of which roughly $990.96 is interest.

FAQ

Does this assume no new charges? Yes. The formula assumes you stop using the card and make the same payment every month until the balance reaches zero.

Why does a higher APR mean a bigger payment? More of each payment goes to interest, so you must pay more overall to clear the principal in the same time.

What if I want to pay off faster? Reduce the number of months — the required payment rises but you save on total interest.