What this calculator does (US)

This tool applies to United States 401(k) workplace retirement plans. Many US employers offer a matching contribution — effectively free money — when you defer part of your paycheck into a 401(k). This calculator shows the annual dollar value of that match based on your salary, how much you contribute, your employer's match cap, and the match rate. Plan rules vary by employer, so confirm your specific match formula in your plan documents.

How to use it

Enter your gross annual salary, the percentage of salary you contribute, the percentage of salary your employer matches up to (the cap), and the match rate. A "50% match up to 6%" means a match rate of \(0.5\) with a cap of 6%. A "100% match (dollar-for-dollar) up to 4%" means a rate of \(1\) with a cap of 4%.

The formula explained

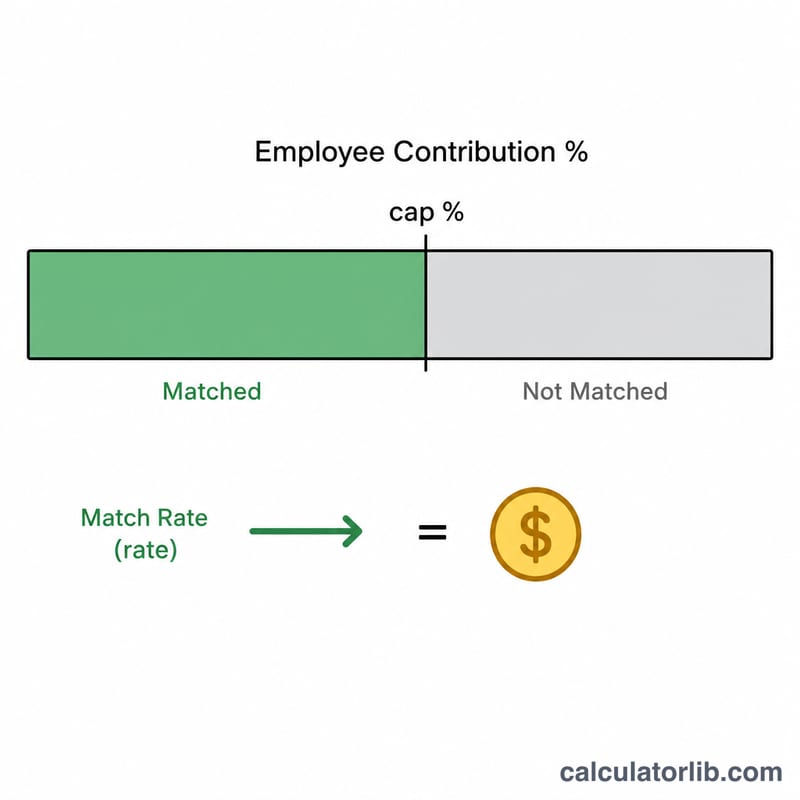

The employer only matches contributions up to the cap, so we first take the smaller of your contribution percentage and the cap percentage. We multiply that by the match rate and your salary:

$$\text{Match} = \min(\text{contrib\%},\,\text{cap\%}) \times \text{rate} \times \text{salary}$$

Contributing less than the cap leaves match dollars on the table; contributing more than the cap earns no extra match (but still grows your retirement savings).

Worked example

Salary $60,000, you contribute 6%, employer matches 50% up to 6%. The matched percentage is \(\min(6, 6) = 6\%\). $$\text{Match} = 6\% \times 0.5 \times \$60{,}000 = \$1{,}800 \text{ per year}$$ Your own contribution is \(6\% \times \$60{,}000 = \$3{,}600\), so $5,400 total goes into your 401(k).

FAQ

What if I contribute more than the cap? The match is still capped — only the first cap% is matched, but contributing more boosts your total retirement savings and may lower taxable income.

Is the match free money? Yes, subject to your plan's vesting schedule. Always contribute at least enough to get the full match.

Does this include IRS contribution limits? No. This estimates the match only; check current IRS annual deferral limits separately.