What is a 401(k) Employer Match?

This calculator applies to US 401(k) workplace retirement plans. An employer match is money your company adds to your 401(k) when you contribute. A very common formula is "50% of contributions up to 6% of salary" — meaning the employer puts in 50 cents for every dollar you contribute, but only on the first 6% of your pay. Leaving this match on the table is leaving free money behind. Note: this tool models a single-tier match and does not enforce the annual IRS contribution limit (e.g. the employee deferral limit), which can apply for high contributions.

How to Use It

Enter your annual salary, the percentage of salary you contribute, your employer's match rate (e.g. 50% or 100%), and the match cap (the maximum percentage of salary the employer will match against). The calculator returns your annual employer match, your own contribution, and your total yearly 401(k) savings.

The Formula Explained

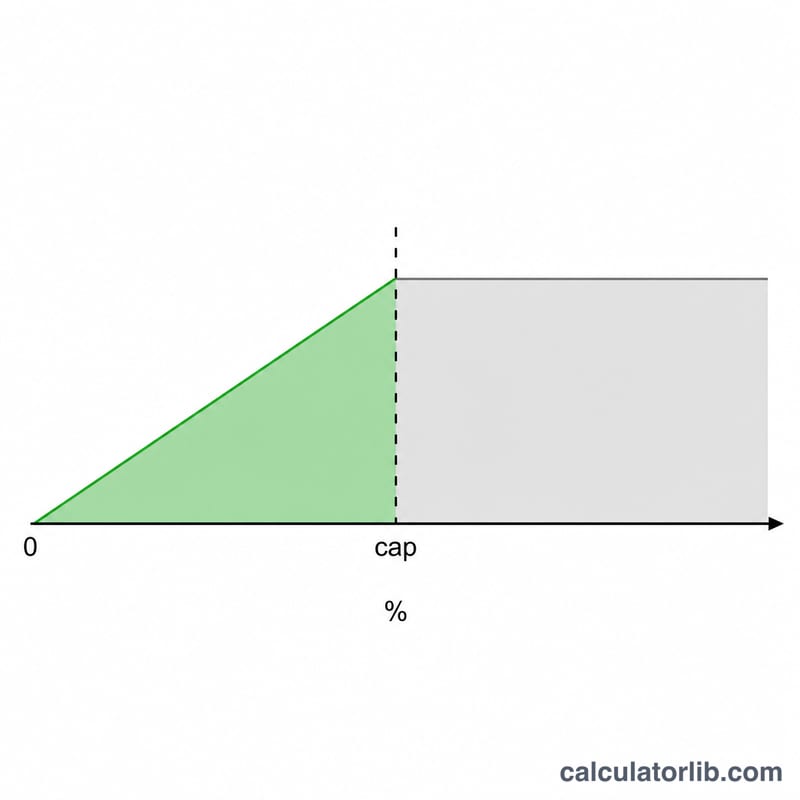

$$\text{Match} = \frac{\min(\text{contribution\%}, \text{cap\%})}{100} \times \text{salary} \times \frac{\text{matchRate}}{100}$$ The min step ensures the employer only matches up to the cap. If you contribute more than the cap, the extra is still saved by you but is not matched.

Worked Example

Suppose you earn $60,000, contribute 6%, your employer matches 50%, and the cap is 6%. The matched portion is \(\min(6, 6) = 6\%\) of $60,000 = $3,600. The employer match is $$\$3{,}600 \times 50\% = \mathbf{\$1{,}800}.$$ Your own contribution is $3,600, so your total annual 401(k) savings is $5,400.

Match Across Different Scenarios

The table below shows the annual employer match and total annual contribution (your money plus the match) for several common match structures at two salary levels. The matched portion is limited by whichever is smaller — your contribution rate or the plan's match cap.

| Salary | Your Contribution | Match Formula | Employer Match | Total Annual Savings |

|---|---|---|---|---|

| $60,000 | 6% ($3,600) | 50% up to 6% | $1,800 | $5,400 |

| $60,000 | 6% ($3,600) | 100% up to 3% | $1,800 | $5,400 |

| $60,000 | 6% ($3,600) | 100% up to 6% | $3,600 | $7,200 |

| $100,000 | 4% ($4,000) | 50% up to 6% | $2,000 | $6,000 |

| $100,000 | 6% ($6,000) | 100% up to 3% | $3,000 | $9,000 |

| $100,000 | 6% ($6,000) | 100% up to 6% | $6,000 | $12,000 |

Notice that at $60,000, a "50% up to 6%" plan and a "100% up to 3%" plan both yield a $1,800 match — the formulas are economically equivalent at the cap. Contributing below the cap leaves match dollars unclaimed; contributing above it adds your own savings but no extra match.

Common Employer Match Formulas

Employer match formulas are typically expressed as a match rate applied to contributions up to a cap (a percentage of pay). The effective maximum employer contribution — the most the employer adds, as a percent of salary — equals the match rate multiplied by the cap. You must contribute at least up to the cap to receive the full match.

| Match Formula | Match Rate | Cap (% of pay) | Max Employer Match (% of salary) |

|---|---|---|---|

| 50% up to 6% | 50% | 6% | 3.0% |

| 100% up to 3% | 100% | 3% | 3.0% |

| 100% up to 4% | 100% | 4% | 4.0% |

| Dollar-for-dollar up to 5% | 100% | 5% | 5.0% |

| 100% up to 6% | 100% | 6% | 6.0% |

| 50% up to 8% | 50% | 8% | 4.0% |

| Tiered: 100% on first 3% + 50% on next 2% | 100% / 50% | 5% | 4.0% |

The widely cited "safe harbor" basic match is 100% on the first 3% plus 50% on the next 2%, giving a maximum employer contribution of 4% of pay when an employee defers at least 5%.

Interpreting Your Result

The employer match figure represents money your employer adds to your account on top of your own contribution. On the matched portion, this is effectively an immediate return: a 50% match on the dollars you contribute up to the cap is a 50% gain before any market growth, and a dollar-for-dollar (100%) match doubles those contributions instantly.

Contributing more than the cap does not earn additional match, but those unmatched dollars still benefit from tax-advantaged growth — pre-tax (traditional) contributions reduce current taxable income and grow tax-deferred, while Roth 401(k) contributions grow tax-free in qualified withdrawals.

A few details affect how much of the match you ultimately keep:

- Combined IRS 415(c) limit. Employee contributions plus employer match (and any other additions) are subject to a separate overall annual limit on total additions to a 401(k) account, which is higher than the employee elective-deferral limit. Most matched employees are nowhere near this combined cap.

- Vesting. Employer match dollars may be subject to a vesting schedule — you may need to stay employed a certain number of years before the match is fully yours. Unvested match is forfeited if you leave early, so the calculated match is the amount credited, not necessarily the amount kept.

- Timing and true-up. Some plans match each paycheck and some "true up" annually; front-loading contributions in a per-paycheck plan can cause you to miss match in later months.

This is general educational information, not personalized financial or tax advice. Check your plan's Summary Plan Description for the exact match formula, vesting schedule and contribution rules, and consult a qualified professional for guidance on your situation.

FAQ

What if I contribute less than the cap? Then you only get matched on what you contribute — you miss part of the free money. To maximize the match, contribute at least up to the cap.

Does the match count toward my IRS limit? Employer matching contributions do not count against your personal elective-deferral limit, though there is a separate combined limit.

Is the match guaranteed? Matches often vest over time. Check your plan's vesting schedule — you may need to stay several years to keep the full match.