What This Calculator Does

This tool is for US retirement savers comparing a Roth IRA against a Traditional IRA. It estimates the future value of a single contribution under each account type, then applies your expected retirement tax rate so you compare apples to apples — on an after-tax basis. Assumptions: a flat annual return, a single lump contribution growing over the period, and a known retirement tax rate. It ignores annual contribution limits, RMDs, and the up-front tax deduction a Traditional IRA provides (which you would separately invest).

How to Use It

Enter your annual contribution, your expected average annual investment return, the number of years until retirement, and the marginal tax rate you expect to pay when withdrawing. The calculator shows the tax-free Roth balance, the after-tax Traditional balance, and the dollar advantage of one over the other.

The Formula Explained

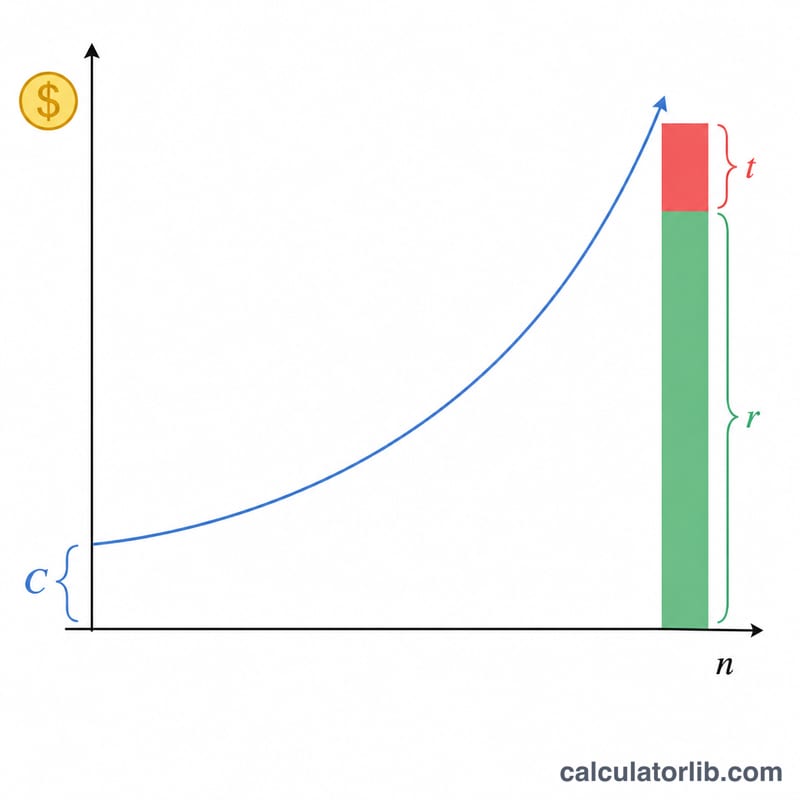

Both accounts grow identically:

$$C(1+r)^n$$where \(C\) is the contribution, \(r\) the annual return, and \(n\) the years. A Roth withdrawal is tax-free, so its after-tax value equals the full balance. A Traditional withdrawal is taxed at rate \(t\), so its after-tax value is the balance multiplied by \((1 - t)\). When your retirement tax rate is positive, the Roth always wins on this single-contribution basis because its dollars were already taxed.

$$\text{Roth}_{FV} = C(1+r)^n,\quad \text{Trad}_{FV} = C(1+r)^n(1-t)$$

Worked Example

Contribute $6,000 at a 7% return for 30 years with a 22% retirement tax rate. Growth factor = \(1.07^{30} \approx 7.612255\). Roth:

$$6{,}000 \times 7.612255 \approx \$45{,}673.53$$Traditional after-tax:

$$45{,}673.53 \times 0.78 \approx \$35{,}625.35$$The Roth advantage is about $10,048.18.

FAQ

Is Roth always better? Not necessarily. This model assumes the same dollar contribution. In reality a Traditional contribution gives an immediate tax deduction; if you invest that savings, results can be closer or favor Traditional when your retirement tax rate is lower than today's.

What return should I use? A long-run diversified stock/bond portfolio has historically returned roughly 6–8% before inflation. Use a conservative figure for planning.

Does this include contribution limits? No. For 2024 the IRA limit is $7,000 ($8,000 if 50+). Enter a value within limits for a realistic projection.