What This Calculator Does

The Compound Interest with Monthly Contributions Calculator projects how an investment or savings account grows when you start with a lump sum and add a fixed amount every month. Unlike a basic compound interest tool, it accounts for both the growth of your starting balance and the ongoing power of regular deposits compounding month after month.

How to Use It

Enter your initial principal (the amount you already have saved), your monthly contribution, the annual interest rate as a percentage, and the number of years you plan to invest. The calculator instantly returns your projected future value, along with a breakdown of how much you contributed versus how much you earned in interest.

The Formula Explained

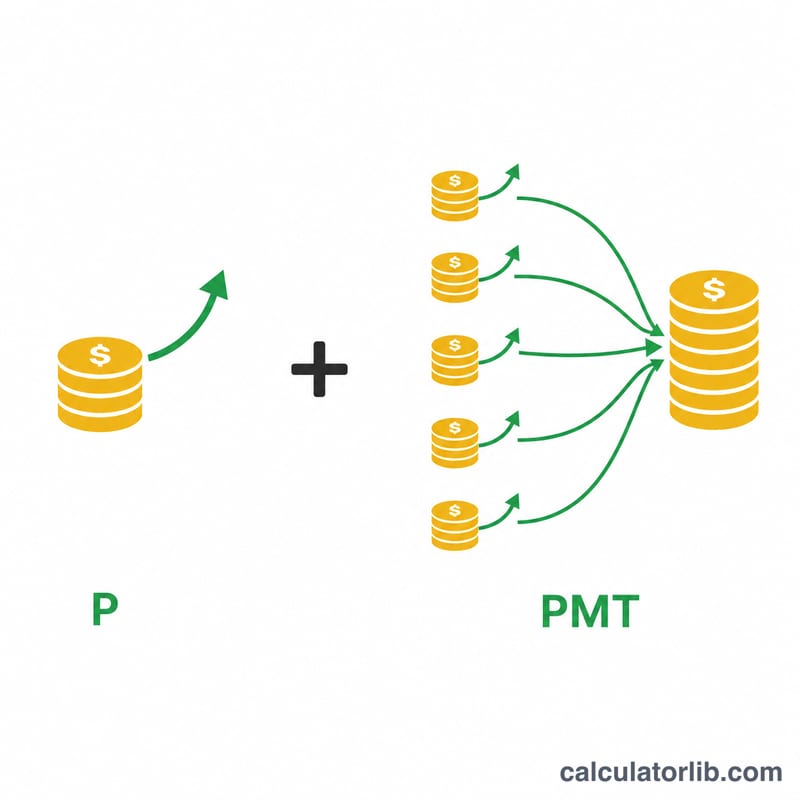

The future value combines two parts. The first, \(P(1+i)^n\), grows your initial principal. The second, \(PMT \cdot \dfrac{(1+i)^n - 1}{i}\), is the future value of an annuity — it sums the growth of every monthly deposit. The full formula is:

$$FV = P(1+i)^n + PMT \cdot \dfrac{(1+i)^n - 1}{i}$$Here \(i\) is the monthly rate (annual rate \(\div 1200\)) and \(n\) is the total number of months (years \(\times 12\)). Contributions are assumed to be made at the end of each month (ordinary annuity).

Worked Example

Suppose you start with $10,000, add $200 per month, earn 6% annually, and invest for 10 years. The monthly rate is \(0.06/12 = 0.005\), and \(n = 120\) months. The principal grows to about $18,194, while the contributions grow to about $32,776, for a future value of roughly $50,970. Of that, $34,000 came from your own money and about $16,970 is interest.

FAQ

Does it compound monthly? Yes. Both the interest and contributions are compounded monthly, which matches most savings and investment accounts.

What if the rate is 0%? The calculator simply adds your principal and total contributions with no growth.

Are contributions added at the start or end of the month? This tool uses end-of-month (ordinary annuity) timing, the most common convention.