What this calculator does (US)

This tool is designed for the United States retirement system, comparing a traditional 401(k) against a Roth 401(k). Contribution limits and rules vary by tax year; this calculator models the math of taxation rather than enforcing IRS annual limits, so enter the contribution you actually plan to make.

How to use it

Enter your annual contribution, expected annual return, years until retirement, and your current and retirement marginal tax rates. The calculator shows the after-tax value of each account at retirement so you can see which wins for your situation.

The formula explained

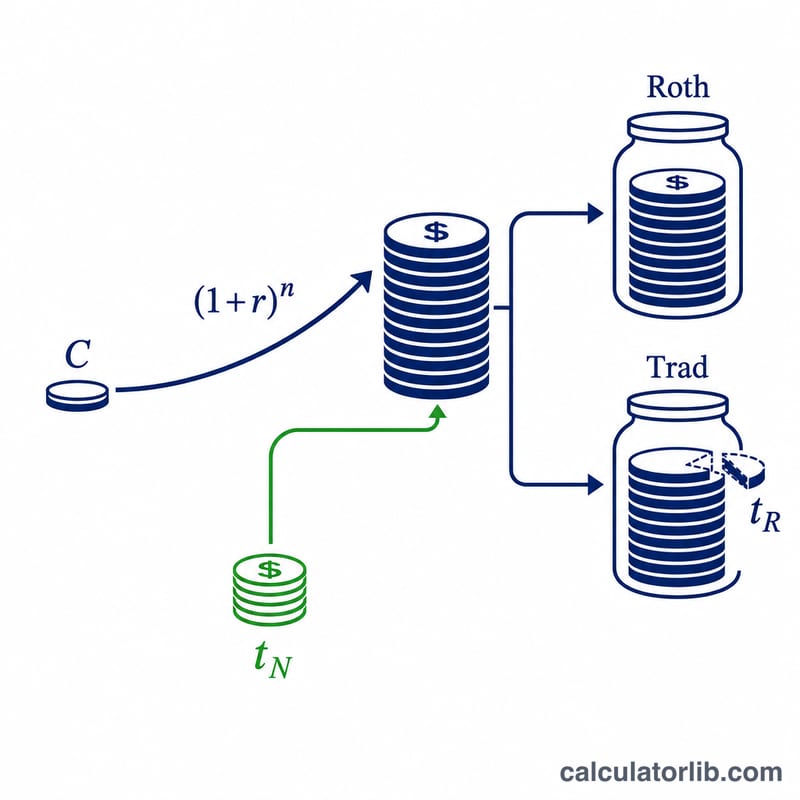

A Roth contribution is made with after-tax dollars and grows tax-free: \(\text{Roth} = C(1+r)^n\). A traditional contribution is pre-tax, so the whole balance is taxed when withdrawn: \(C(1+r)^n(1-t_R)\). To compare fairly, the upfront tax saving (\(C \times t_N\)) is invested in a side account that also grows and is taxed at the retirement rate: \(C\,t_N(1+r)^n(1-t_R)\). The two traditional pieces are added together.

$$\text{Roth} = C(1+r)^n,\quad \text{Trad} = C(1+r)^n(1-t_R) + C\,t_N(1+r)^n(1-t_R)$$

Worked example

Contribute $5,000 at 6% for 20 years. Growth factor = \(1.06^{20} \approx 3.207135\). Roth = \(5{,}000 \times 3.207135 \approx 16{,}035.68\). Traditional balance taxed at 15% = \(16{,}035.68 \times 0.85 \approx 13{,}630.33\). Upfront saving \(5{,}000 \times 0.30 = 1{,}500\) grown and taxed: \(1{,}500 \times 3.207135 \times 0.85 \approx 4{,}087.92\). Traditional total \(\approx 17{,}718.25\) — beating Roth here because the retirement tax rate (15%) is well below today's rate (30%).

Key Terms & Variables

- Contribution \(C\)

- The dollar amount you put in this year. In a Roth 401(k), \(C\) is paid with after-tax dollars; in a Traditional 401(k), \(C\) is pre-tax, so the same paycheck reduction lets you contribute more (or frees up cash equal to the tax saved).

- Annual return \(r\)

- The assumed compound rate of growth per year, expressed as a percent. Both accounts are assumed to grow at the same rate.

- Years \(n\)

- The number of years the money compounds before withdrawal, giving the growth factor \(g=(1+r/100)^n\).

- Current marginal rate \(t_N\)

- The tax rate on the last dollar of your income today — the rate the Traditional contribution avoids and the rate at which your upfront tax savings are generated.

- Retirement marginal rate \(t_R\)

- The tax rate expected to apply to Traditional withdrawals (and side-account gains) when you retire. This is the single most decisive input.

- Pre-tax vs after-tax dollars

- Pre-tax dollars (Traditional) have never been taxed and are taxed on the way out; after-tax dollars (Roth) were already taxed and come out tax-free. A dollar of each is not worth the same.

- Side account

- The investment of the upfront tax savings \(C\cdot t_N/100\) that a fair comparison assumes the Traditional saver also invests. Without it, the Traditional contributor enjoys an extra spendable amount the Roth saver does not.

- Tax-free growth

- The Roth feature whereby qualified earnings are never taxed. The Traditional account grows tax-deferred but every withdrawn dollar is taxed at \(t_R\).

Interpreting Your Result

The option with the higher after-tax value is the more tax-efficient choice for the assumptions you entered. The difference \(\Delta = V_{\text{Roth}} - V_{\text{Trad}}\) tells you the dollar advantage: positive favors the Roth, negative favors the Traditional.

The break-even point. When your current rate equals your retirement rate (\(t_N=t_R\)), and the side account is fully invested and taxed at the same rate, the two strategies produce identical after-tax values. Algebraically the \((1-t_R)\) factors cancel out and \(V_{\text{Roth}}=V_{\text{Trad}}\). This is the mathematical core of the decision: Roth wins only if \(t_R>t_N\), and Traditional wins only if \(t_R

Why the side-account assumption matters. The Traditional total above credits you with investing the upfront tax savings. If, in reality, you spend that tax refund instead of investing it, the Traditional advantage in the \(t_R

Factors not modeled. This calculator simplifies several real-world effects:

- Required minimum distributions (RMDs) historically applied to Traditional balances and could force taxable withdrawals; Roth 401(k)s no longer require RMDs for the original owner under current rules.

- Future tax-law changes — bracket structures and rates can shift, and your actual retirement rate is unknown today.

- Employer match is always pre-tax and lands in a Traditional bucket regardless of which account you choose, so it is taxed on withdrawal.

- A single flat \(t_R\) ignores that retirement income is taxed across multiple brackets; your effective rate is often lower than your marginal rate.

This is general educational information, not personalized tax or financial advice. Consider consulting a qualified professional about your specific situation before choosing between account types.

FAQ

Which is better, Roth or traditional? Roth wins when your retirement tax rate is higher than today's; traditional wins when it is lower.

Why include a side account? A fair comparison must invest the traditional plan's upfront tax savings, otherwise the traditional option is understated.

Are state taxes included? No — enter a combined marginal rate if you want to factor in state income tax.