What This Calculator Does

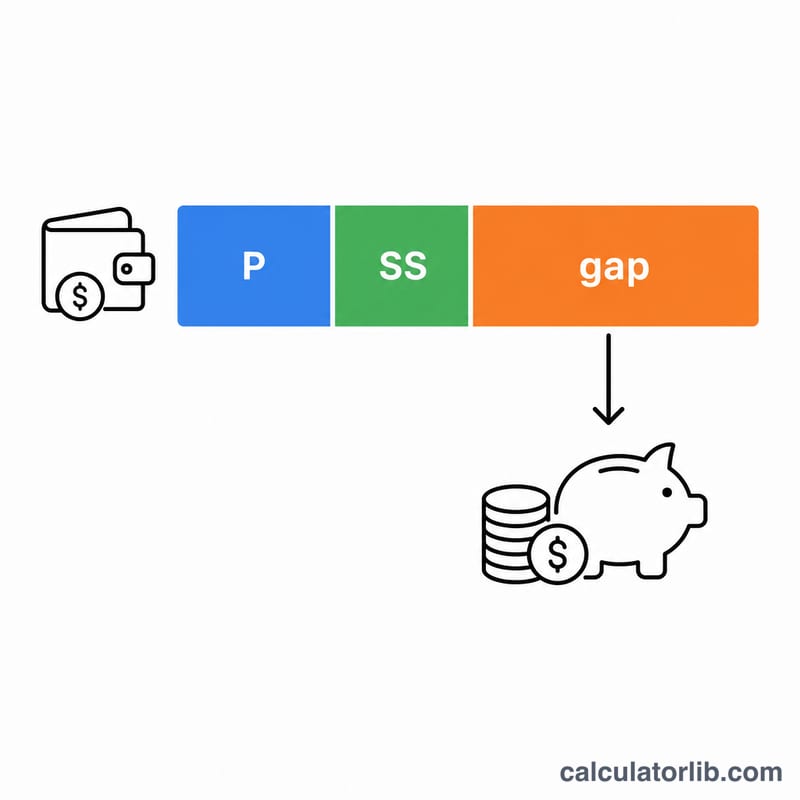

The Nest Egg Needed After Pension & Social Security Calculator tells you how large your investment portfolio must be at retirement to bridge the gap between your guaranteed income (pensions and Social Security) and the lifestyle you actually want. Instead of guessing a "round number," it works backward from your spending target. Social Security figures and pension structures referenced here are typical of the United States, but the math applies to any guaranteed-income source in any country.

How to Use It

Enter your desired annual retirement income — the total you want to spend each year. Then enter the annual pension and annual Social Security you expect to receive. Finally, choose a safe withdrawal rate (SWR). The classic figure is 4%, based on the Trinity Study, though many planners now use 3.5% for added safety. The calculator subtracts your guaranteed income from your target, then divides the remaining gap by your SWR to size the portfolio.

The Formula Explained

$$\text{Nest Egg} = \frac{\text{Desired Income} - \text{Pension} - \text{Social Security}}{\text{SWR}}$$ The numerator is the income gap your savings must produce. Dividing by the withdrawal rate (as a decimal) capitalizes that income stream. For example, a 4% SWR means each dollar of annual income requires $25 of savings \((1 \div 0.04 = 25)\).

Worked Example

Suppose you want $60,000 a year, expect $20,000 from Social Security and no pension, and use a 4% SWR. The income gap is $$\$60{,}000 - \$20{,}000 = \$40{,}000.$$ Dividing by 0.04 gives a required nest egg of $1,000,000.

FAQ

What withdrawal rate should I use? 4% is the traditional benchmark; 3% to 3.5% is more conservative and suited to early retirement or longer horizons.

Should I include taxes? Yes — enter your desired income on a pre-tax (gross) basis if your pension and Social Security figures are also pre-tax, so everything is consistent.

What if my guaranteed income exceeds my target? Then your income gap is zero and no additional nest egg is required for income — though savings still provide a valuable buffer for emergencies and inflation.