What this calculator does

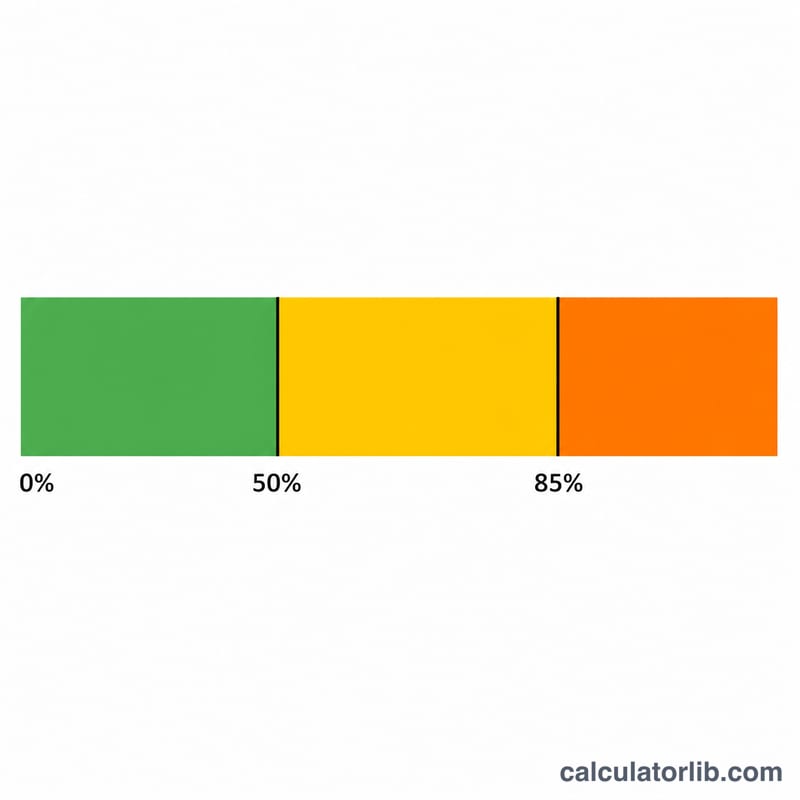

This tool applies to the United States. It estimates how much of your Social Security retirement, survivor, or disability benefits must be included in your federal taxable income, following the IRS worksheet in Publication 915. Depending on your other income, anywhere from 0% to 85% of your benefits may be taxed. State taxes are not included, and these are current federal rules — the threshold amounts ($25,000/$34,000 single, $32,000/$44,000 married filing jointly) are not indexed for inflation.

How to use it

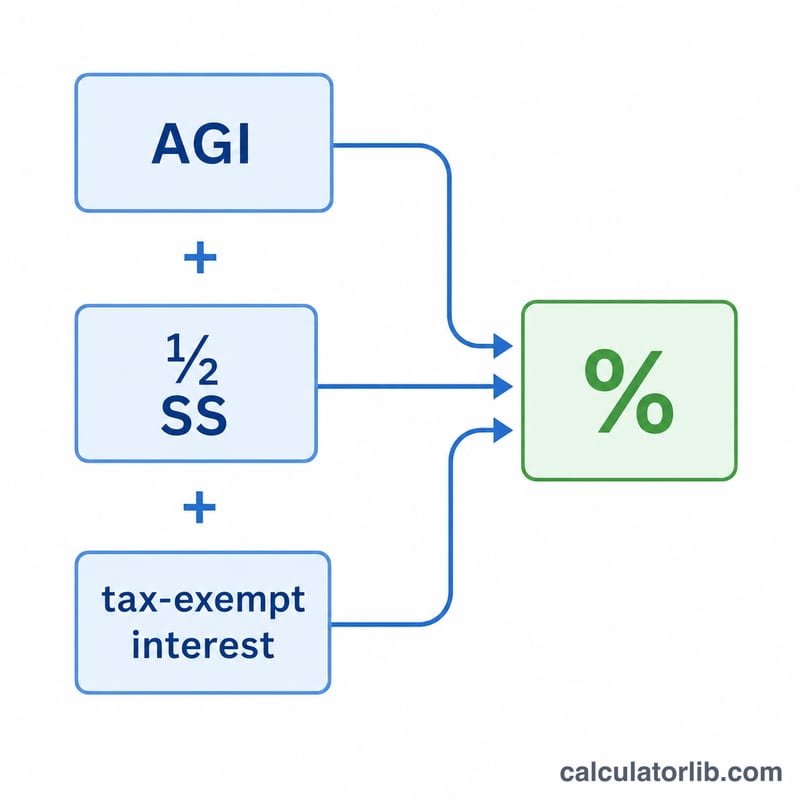

Choose your filing status, enter your annual Social Security benefits, your other income (your AGI excluding Social Security — wages, pensions, IRA distributions, dividends, etc.), and any tax-exempt interest such as municipal bond income. The calculator returns your provisional (combined) income and the taxable portion of your benefits.

The formula explained

First compute provisional income = other income + tax-exempt interest + 50% of benefits. If it is below the base threshold, none of your benefits are taxed. Between the base and upper thresholds, up to 50% of benefits may be taxed. Above the upper threshold, the IRS adds 85% of the excess to the smaller of (50% of benefits) or (50% of the gap between thresholds), capped at 85% of total benefits.

$$T = \begin{cases} 0 & P \le B \\[4pt] \min\!\left(\tfrac{1}{2}(P-B),\ \tfrac{1}{2}S\right) & B < P \le U \\[4pt] \min\!\left(0.85\,(P-U) + \min\!\left(\tfrac{1}{2}(U-B),\tfrac{1}{2}S\right),\ 0.85\,S\right) & P > U \end{cases}$$ $$\text{where}\quad \left\{ \begin{aligned} P &= \text{AGI} + \text{Tax-Exempt Int.} + \tfrac{1}{2}\,\text{SS Benefits} \\ S &= \text{SS Benefits} \\ B &= 25{,}000,\quad U = 34{,}000 \end{aligned} \right.$$

Worked example

A single filer receives $20,000 in benefits with $30,000 of other income and no tax-exempt interest. Provisional income = \(30{,}000 + 0.5\times20{,}000 = \$40{,}000\), which exceeds the $34,000 upper threshold. Taxable:

$$\min\!\left(0.85\times(40{,}000-34{,}000) + \min\!\left(0.5\times(34{,}000-25{,}000),\ 0.5\times20{,}000\right),\ 0.85\times20{,}000\right) = \min(5{,}100 + \min(4{,}500,\ 10{,}000),\ 17{,}000) = \min(9{,}600,\ 17{,}000) = \mathbf{\$9{,}600}.$$FAQ

Can more than 85% ever be taxed? No — 85% is the federal maximum portion of Social Security that can be taxable.

Does tax-exempt interest matter? Yes. Although municipal bond interest is tax-free, the IRS adds it back when computing provisional income, which can push more of your benefits into the taxable range.

Is this an exact tax figure? It estimates the taxable amount of benefits, not your tax bill. Multiply by your marginal rate or use full software for exact liability.