What this calculator does (US only)

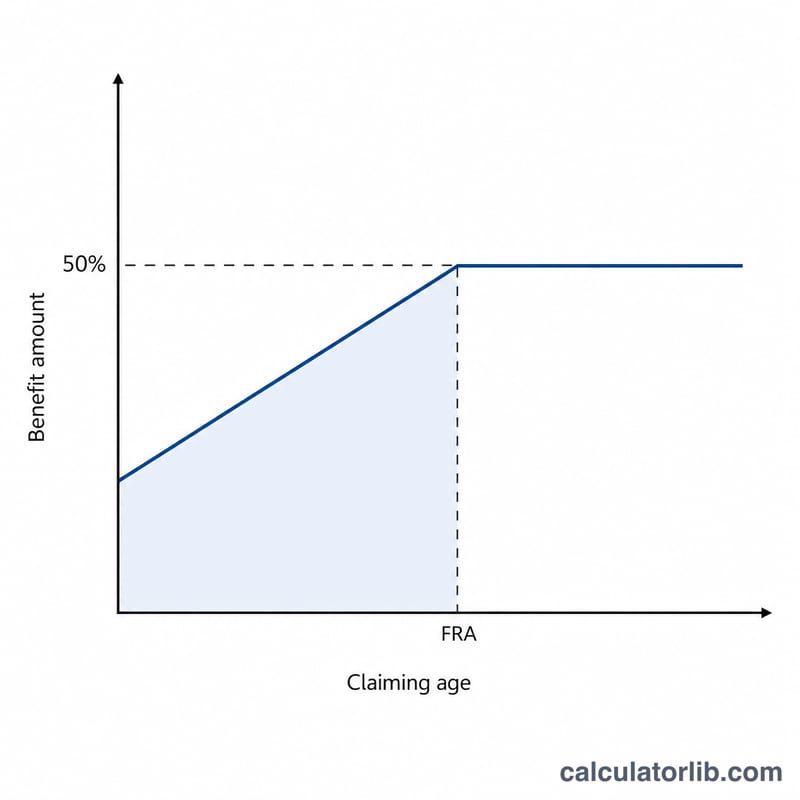

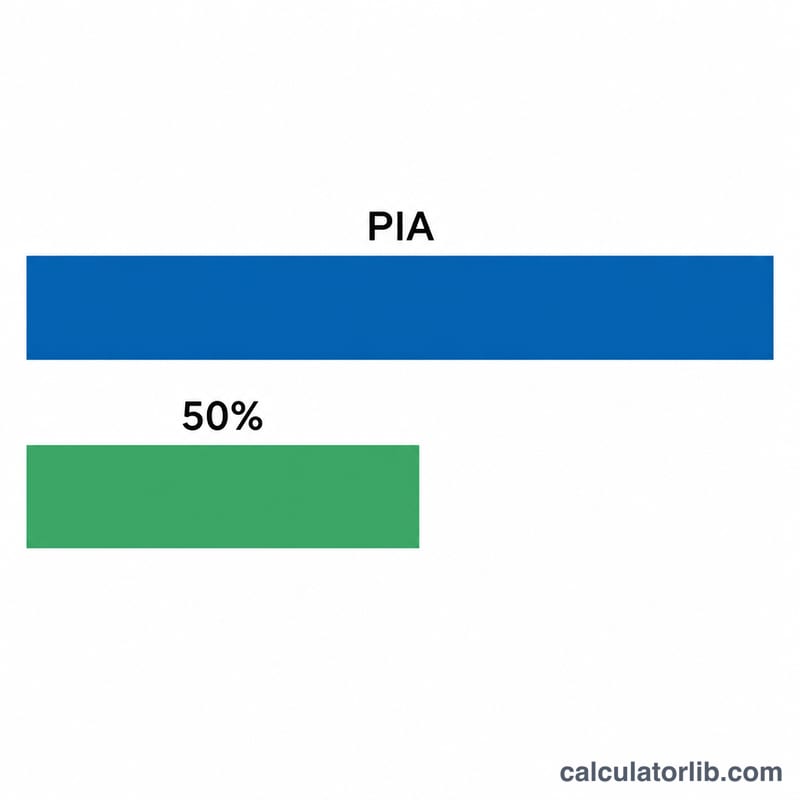

This tool estimates the Social Security spousal benefit available under the US Social Security Administration (SSA) rules. A spousal benefit lets a husband or wife collect a check based on their partner's earnings record. At your own full retirement age (FRA), the maximum spousal benefit is 50% of the worker's Primary Insurance Amount (PIA) — the monthly amount the worker would receive at their own FRA. Estimates here use current SSA reduction rules and assume the worker has already filed.

How to use it

Enter the worker's PIA (their monthly benefit at full retirement age), select your own FRA (66, 66½, or 67 depending on your birth year), and enter the age at which you plan to claim. The calculator returns your estimated monthly spousal benefit, the unreduced 50% amount, and the percentage reduction for claiming early.

The formula explained

The unreduced spousal benefit is \(0.50 \times \text{PIA}\). If you claim before your FRA, SSA reduces it by 25/36 of 1% per month for the first 36 months early, plus 5/12 of 1% per month for any additional months. Unlike retirement benefits, spousal benefits earn no delayed retirement credits, so claiming after FRA does not increase them.

$$\begin{gathered} B = 0.5 \cdot \text{PIA} \cdot \left(1 - R\right) \\[1.5em] \text{where}\quad \left\{ \begin{aligned} m &= \left(\text{FRA} - \text{Claim Age}\right)\times 12 \\ R &= \tfrac{25}{3600}\cdot\min(m,36) + \tfrac{5}{1200}\cdot\max(m-36,\,0) \end{aligned} \right. \end{gathered}$$

Worked example

Suppose the worker's PIA is $2,000 and your FRA is 67. The full spousal benefit is \(0.50 \times \$2{,}000 = \$1{,}000\). If you claim at 64, that's 36 months early: reduction = \(36 \times (25/36 \text{ of } 1\%) = 25\%\). Your benefit = $$\$1{,}000 \times (1 - 0.25) = \$750 \text{ per month}$$

FAQ

Can I get more than 50%? No. 50% of the worker's PIA is the maximum, reached only at your full retirement age.

Does waiting past FRA help? No. Spousal benefits do not earn delayed retirement credits, so there's no bonus for claiming after FRA.

Is this exact? It is an estimate. Your actual benefit depends on your own work record, deemed filing rules, and SSA's official PIA. Confirm figures with the SSA.