What This Calculator Does (US Only)

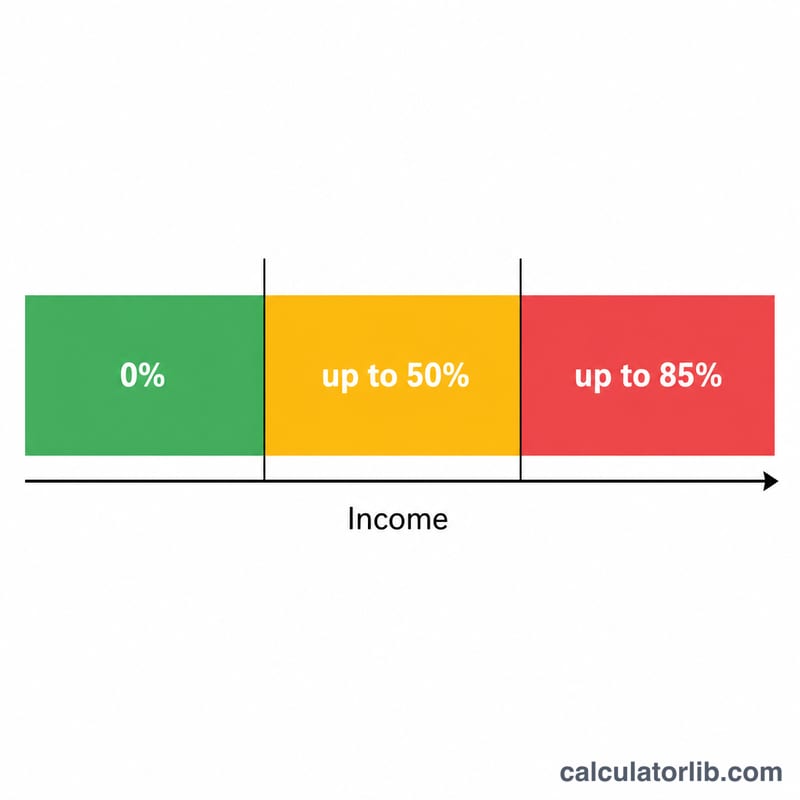

This tool applies United States IRS rules to estimate how much of your Social Security retirement, survivor, or disability benefits will be included in your federal taxable income. Depending on your total income, anywhere from 0% to a maximum of 85% of your benefits may be taxed. The thresholds used ($25,000/$34,000 for single filers and $32,000/$44,000 for married filing jointly) are set by federal law and are not indexed for inflation, so they apply to current tax years. State taxes are not included.

How to Use It

Enter your annual Social Security benefits, your other income (your adjusted gross income excluding benefits — wages, pensions, IRA withdrawals, dividends, etc.), and any tax-exempt interest such as municipal bond income. Choose your filing status and the calculator returns the taxable dollar amount, the percentage of benefits that is taxable, and your provisional (combined) income.

The Formula Explained

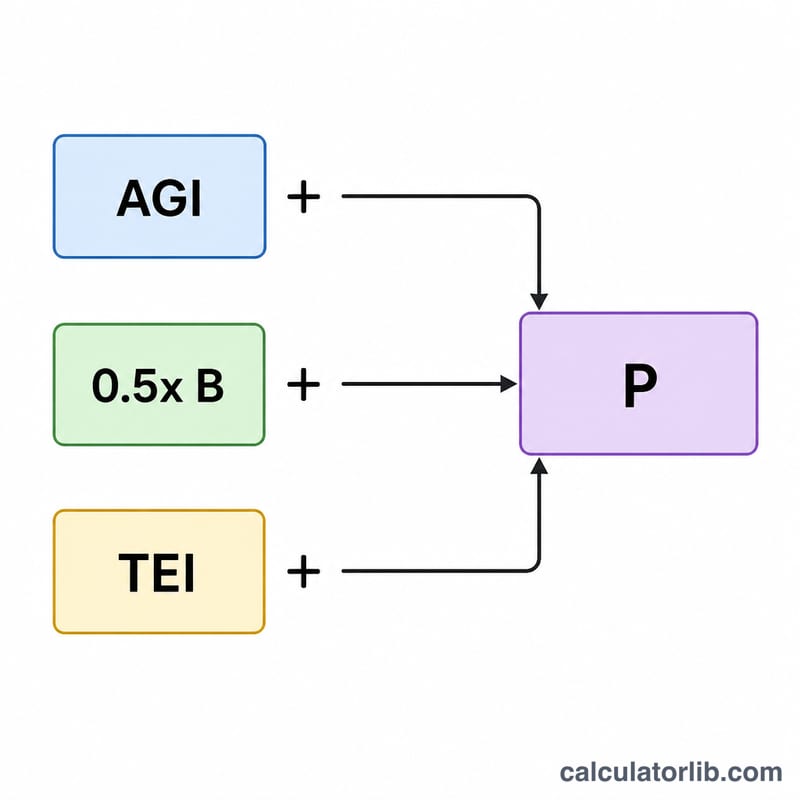

First, provisional income = other income + tax-exempt interest + half of your benefits. If provisional income is below the base threshold, none of your benefits are taxable. Between the base and upper thresholds, up to 50% of benefits become taxable. Above the upper threshold, the amount jumps to a maximum of 85% of benefits, computed as 85% of the excess over the upper threshold plus the smaller of 50% of the threshold gap or 50% of benefits — capped at 85% of total benefits.

$$\text{Taxable} = \begin{cases} 0 & P \le B \\[4pt] \min\!\left(\tfrac{1}{2}(P-B),\ \tfrac{1}{2}\text{SS}\right) & B < P \le U \\[4pt] \min\!\left(0.85(P-U)+L,\ 0.85\,\text{SS}\right) & P > U \end{cases}$$ $$\text{where}\quad \left\{ \begin{aligned} P &= \text{Other Income} + \text{Tax-Exempt Int.} + \tfrac{1}{2}\,\text{SS} \\ \text{SS} &= \text{SS Benefits} \\ B &= 25{,}000,\quad U = 34{,}000 \\ L &= \min\!\left(\tfrac{1}{2}(U-B),\ \tfrac{1}{2}\text{SS}\right) \end{aligned} \right.$$

Worked Example

A single filer receives $20,000 in benefits with $40,000 of other income and no tax-exempt interest. Provisional income = \(40{,}000 + 0 + 10{,}000 = \$50{,}000\), which is above the $34,000 upper threshold. Over = \(50{,}000 - 34{,}000 = \$16{,}000\), so \(0.85 \times 16{,}000 = \$13{,}600\). Add the lesser of \(0.5 \times (34{,}000 - 25{,}000) = \$4{,}500\) or \(0.5 \times 20{,}000 = \$10{,}000\), i.e. $4,500. Tentative = $18,100, but the 85% cap = \(0.85 \times 20{,}000 = \$17{,}000\), so taxable benefits = $17,000 (85%).

FAQ

Is 85% the most that can be taxed? Yes — at most 85% of your Social Security benefits are ever subject to federal income tax.

Does this include state taxes? No. A handful of states tax benefits separately; this tool covers only the federal calculation.

What counts as "other income"? Essentially your AGI before adding Social Security: wages, self-employment, pensions, taxable IRA/401(k) distributions, interest, dividends and capital gains.