What This Calculator Does

Applies to the United States Social Security program (SSA rules). Your benefit at full retirement age (FRA) is called the Primary Insurance Amount (PIA). If you claim before FRA, your monthly check is permanently reduced; if you wait past FRA, you earn delayed retirement credits that increase it. This tool estimates the adjusted monthly and annual benefit based on the age you choose to claim.

How to Use It

Enter your PIA (the monthly amount the Social Security Administration estimates for you at full retirement age), your full retirement age (commonly 66–67 depending on birth year), and the age at which you plan to claim. The calculator computes the number of months you are claiming early or late and applies the corresponding reduction or credit.

The Formula Explained

The number of months from FRA is \((\text{claimAge} - \text{FRA}) \times 12\). For early claiming, the first 36 early months reduce the benefit by 5/9 of 1% each (about 0.5556%), and any further months reduce it by 5/12 of 1% each (about 0.4167%). For delayed claiming, each month adds 2/3 of 1% (8% per year), up to age 70.

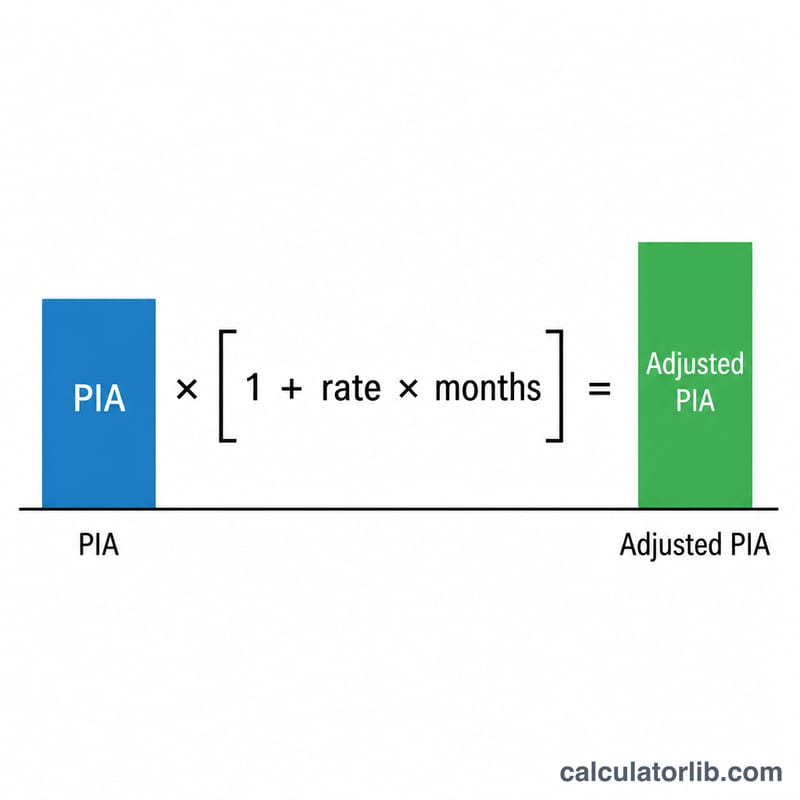

$$R = 36\times\tfrac{5}{9}\%+(m-36)\times\tfrac{5}{12}\%$$$$C = m \times \tfrac{2}{3}\%$$$$\text{Adjusted} = \text{PIA} \times (1 + \text{rate} \times \text{months})$$

Worked Example

Suppose your PIA is $2,000 and your FRA is 67, but you claim at 62 — that is 60 months early. The first 36 months cut the benefit by \(36 \times \tfrac{5}{9}\% = 20\%\), and the remaining 24 months by \(24 \times \tfrac{5}{12}\% = 10\%\), for a total 30% reduction. Your adjusted benefit is

$$\$2{,}000 \times (1 - 0.30) = \$1{,}400 \text{ per month}$$FAQ

Is this an official SSA figure? No. It is an estimate using standard SSA adjustment rates and does not account for earnings tests, taxation, or COLA increases.

What is the maximum delayed credit? Delayed retirement credits stop accruing at age 70, so claiming later than 70 provides no further increase.

What is PIA? The Primary Insurance Amount is the benefit you would receive if you started benefits exactly at your full retirement age.