What Is a Business Loan Calculator?

A business loan calculator estimates the fixed monthly payment on an amortizing loan, along with the total interest you will pay over the life of the loan and your total repayment. It is useful when comparing financing offers, planning cash flow, or deciding how much you can comfortably borrow for equipment, expansion, or working capital.

How to Use It

Enter the loan amount (principal), the annual interest rate as a percentage, and the loan term in years. The calculator converts the annual rate to a monthly rate, computes the number of monthly payments, and applies the standard amortization formula to return your fixed monthly payment.

The Formula Explained

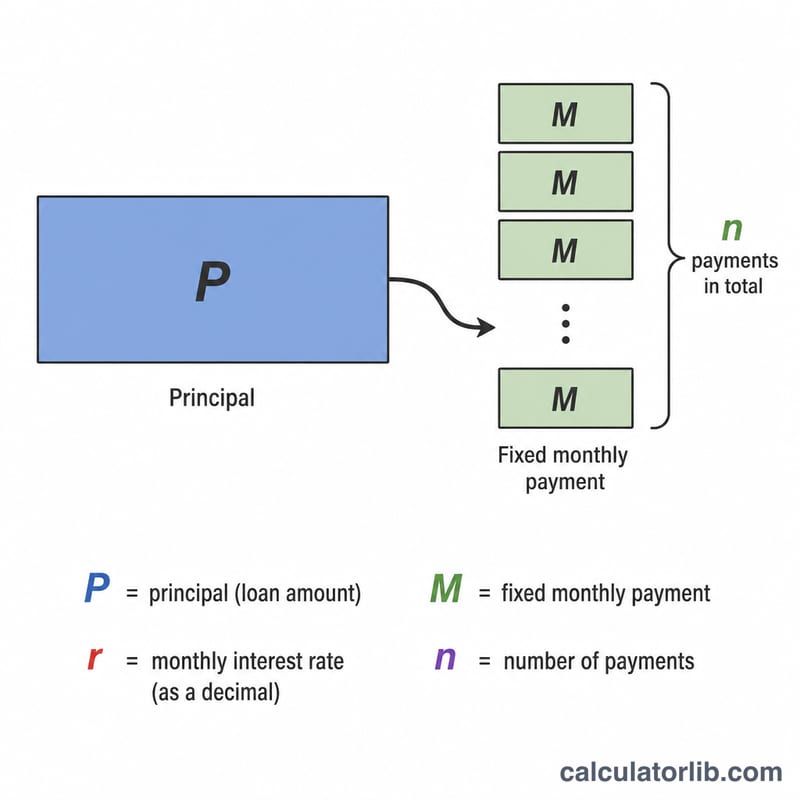

The monthly payment is given by $$M = \dfrac{P \cdot r \cdot (1+r)^n}{(1+r)^n - 1}$$, where \(P\) is the principal, \(r\) is the monthly interest rate (annual rate divided by 12, expressed as a decimal), and \(n\) is the total number of payments (years \(\times\) 12). If the interest rate is zero, the payment simply becomes \(P / n\).

Worked Example

Suppose you borrow $100,000 at 8% annual interest over 5 years. The monthly rate is \(r = 0.08/12 \approx 0.0066667\) and \(n = 60\) payments. Plugging in, \((1+r)^{60} \approx 1.48985\), so $$M = \frac{100000 \times 0.0066667 \times 1.48985}{1.48985 - 1} \approx \$2{,}027.64 \text{ per month}.$$ Over 60 months you repay about $121,658, of which roughly $21,658 is interest.

Interpreting Your Result

The calculator produces three figures, each answering a different question about the loan:

- Monthly payment (\(M\)) — the fixed amount you owe each month. For a fully amortizing loan, every payment covers all accrued interest for that month plus a portion of principal, so the balance steadily falls to zero by the final payment.

- Total interest — the cumulative cost of borrowing, equal to \(M \times n - P\). This is what the loan costs you beyond the amount you actually received.

- Total repayment — the sum of all payments, \(M \times n\), combining principal and interest.

Two factors push the interest share upward. Longer terms keep a larger balance outstanding for more months, so even at the same rate you pay more total interest (though each monthly payment is smaller). Higher rates increase the interest charged on every dollar of remaining balance. A loan can therefore have an affordable monthly payment yet a high lifetime cost.

This calculator models interest on the rate you enter. The APR (annual percentage rate) can be higher than the stated interest rate because APR folds in origination fees, closing costs, and other charges. Since this tool excludes such fees, the true cost of a loan with upfront charges will exceed the figures shown here — compare offers on APR, not the nominal rate.

Lenders judge whether your business can carry the payment using the debt-service coverage ratio (DSCR), defined as net operating income divided by total debt service. A DSCR above roughly 1.25 is commonly required, meaning operating income should exceed the annual loan payments by a comfortable margin.

Key Terms Defined

- Principal (\(P\))

- The amount borrowed — the starting loan balance before any interest accrues.

- Annual interest rate

- The nominal yearly rate charged on the outstanding balance, expressed as a percentage. It does not by itself include fees.

- APR (annual percentage rate)

- The yearly cost of the loan expressed as a percentage that includes interest plus required fees such as origination and closing costs. APR ≥ the nominal interest rate and is the standard basis for comparing offers.

- Monthly rate (\(r\))

- The annual rate divided by 12 (and by 100 to convert from a percentage), i.e. \(r = \frac{\text{annual rate \%}}{1200}\). This is the rate applied to the balance each month.

- Term (\(n\))

- The length of the loan. In this calculator the term in years is multiplied by 12 to give the total number of monthly payments.

- Amortization

- The process of paying off a loan through equal periodic payments that gradually shift from mostly interest early on to mostly principal near the end, reaching a zero balance at maturity.

- Total interest

- The sum of all interest paid over the life of the loan, equal to total repayment minus principal.

- Total repayment

- The grand total paid to the lender over the full term: principal plus all interest (monthly payment × number of payments).

- Balloon payment

- A large lump sum due at the end of certain loans whose regular payments do not fully amortize the balance. Standard amortizing loans (as modeled here) have no balloon.

- Origination fee

- An upfront charge, often a percentage of the loan amount, for processing and funding the loan. It raises the effective APR but is not part of the interest rate.

FAQ

Does this include fees? No. It models principal and interest only. Origination fees, insurance, or balloon payments are not included.

What rate should I enter? Use the nominal annual interest rate (APR) quoted by your lender, not a monthly figure.

Can I use it for any currency? Yes — the math is universal. The dollar sign is just for display; enter amounts in your own currency.