What Is a Reverse Loan Calculator?

A reverse loan calculator flips the usual question. Instead of "how much will my monthly payment be for a given loan?", it asks "how big a loan can I afford if I can pay a certain amount each month?" By entering your target monthly payment, the interest rate, and the term, it solves for the loan amount — the present value (PV) of that stream of payments. This is ideal for budgeting before you shop for a mortgage, car loan, or personal loan.

How to Use It

Enter the monthly payment you are comfortable making, the annual interest rate offered by your lender, and the loan term in years. The calculator instantly returns the maximum loan amount, the total number of payments, the total you will repay over the life of the loan, and the total interest paid.

The Formula Explained

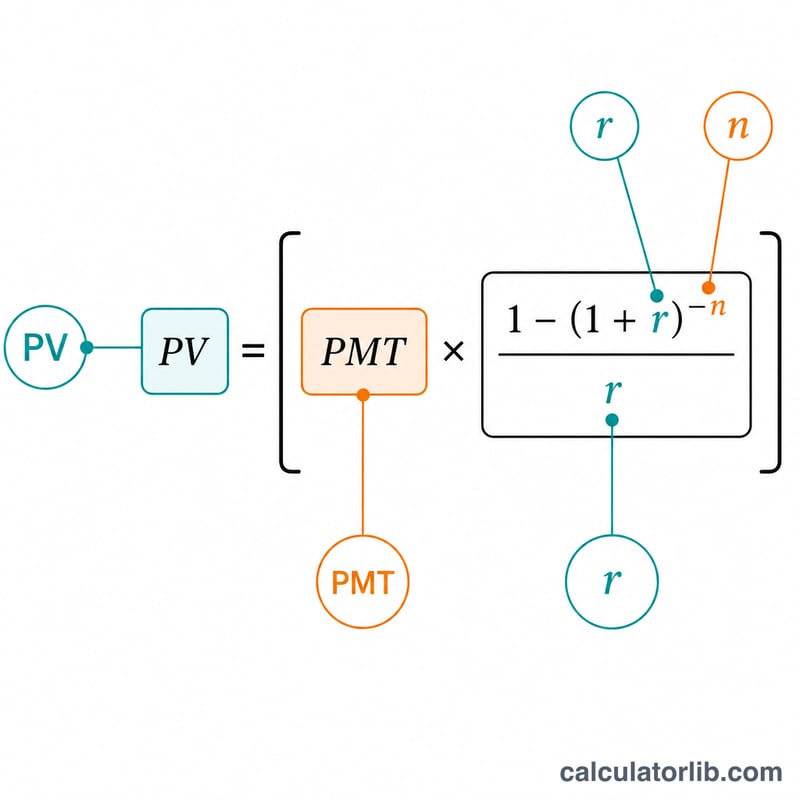

The tool uses the present value of an ordinary annuity formula:

$$\text{PV} = \text{PMT} \times \frac{1 - (1 + r)^{-n}}{r}$$Here r is the monthly interest rate (annual rate ÷ 12 ÷ 100) and n is the total number of monthly payments (years × 12). When the interest rate is zero, the loan amount is simply payment × n.

Worked Example

Suppose you can pay $1,000 per month, the annual rate is 6%, and the term is 30 years. The monthly rate \(r = 0.005\) and \(n = 360\).

$$\text{PV} = 1000 \times \frac{1 - 1.005^{-360}}{0.005} \approx \$166{,}791.61$$Over 30 years you would pay $360,000 in total, of which about $193,208 is interest.

FAQ

Does this include taxes and insurance? No. It models only principal and interest. For a mortgage, escrow for property tax and insurance reduces how much of your payment goes to the loan.

What rate should I use? Use the APR your lender quotes for the closest result, since APR reflects the effective borrowing cost.

Can I use it for any loan? Yes — any fully amortizing fixed-rate loan with equal monthly payments works, including mortgages, auto loans, and personal loans.