What this calculator does

The Loan Affordability by Income Calculator estimates the largest loan you could realistically borrow based on what your budget can support each month. It combines your gross monthly income, a target debt-to-income (DTI) ratio, your current debt payments, and the loan's interest rate and term to produce a maximum affordable loan amount. It is a general-purpose tool and does not assume any specific country's lending rules.

How to use it

Enter your gross monthly income before taxes, the maximum DTI ratio you want to stay under (lenders often use 36%–43%), your existing monthly debt payments (cards, car, student loans), and the loan's annual interest rate and term in years. The calculator returns your monthly payment budget, the payment available for the new loan, and the loan principal that payment can support.

The formula explained

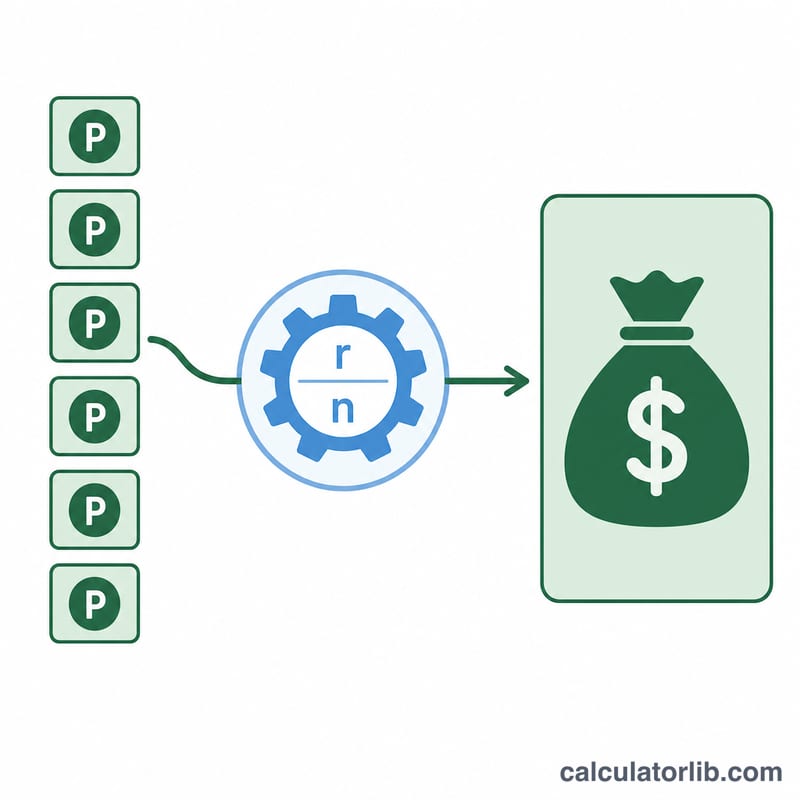

First it finds your total payment budget: \(\text{Income} \times \text{DTI}\). It subtracts existing debt payments to get the payment available for the new loan, \(P\). Then it converts that payment into a loan amount using the present-value annuity formula, where \(r\) is the monthly interest rate (annual rate ÷ 12) and \(n\) is the number of monthly payments (years × 12): $$\text{Loan} = P \cdot \frac{1 - (1 + r)^{-n}}{r}$$

Worked example

Income $5,000/month, DTI 36%, existing debts $500, rate 6%, term 30 years. Budget \(= 5000 \times 0.36 = \$1{,}800\). Available payment \(P = 1800 - 500 = \$1{,}300\). Monthly rate \(r = 0.06/12 = 0.005\), \(n = 360\). $$\text{Loan} = 1300 \times \frac{1 - 1.005^{-360}}{0.005} \approx \$216{,}829$$

FAQ

What is a good DTI ratio? Many lenders prefer a total DTI at or below 36%, though some allow up to 43% or higher depending on the product and your credit profile.

Should I use gross or net income? DTI is conventionally based on gross (pre-tax) monthly income, which is what this calculator expects.

Does this include taxes, insurance or fees? No. It estimates principal and interest only. Add property taxes, insurance and closing costs separately for a complete picture.