What Is the Discount Yield?

The bank discount yield (also called the discount rate or discount yield) is the standard way to quote the return on short-term discount instruments such as U.S. Treasury bills (T-bills), commercial paper, and bankers' acceptances. These securities pay no coupon; instead they are sold below face value and redeemed at face value at maturity. The discount yield annualizes the gain using a 360-day year, which is the convention for money-market instruments.

How to Use This Calculator

Enter three values: the face value (F) the security pays at maturity, the purchase price (P) you actually pay today, and the days to maturity (t). The calculator returns the annualized bank discount yield as a percentage, the dollar discount (F − P), and the bond equivalent yield for easier comparison with coupon bonds.

The Formula Explained

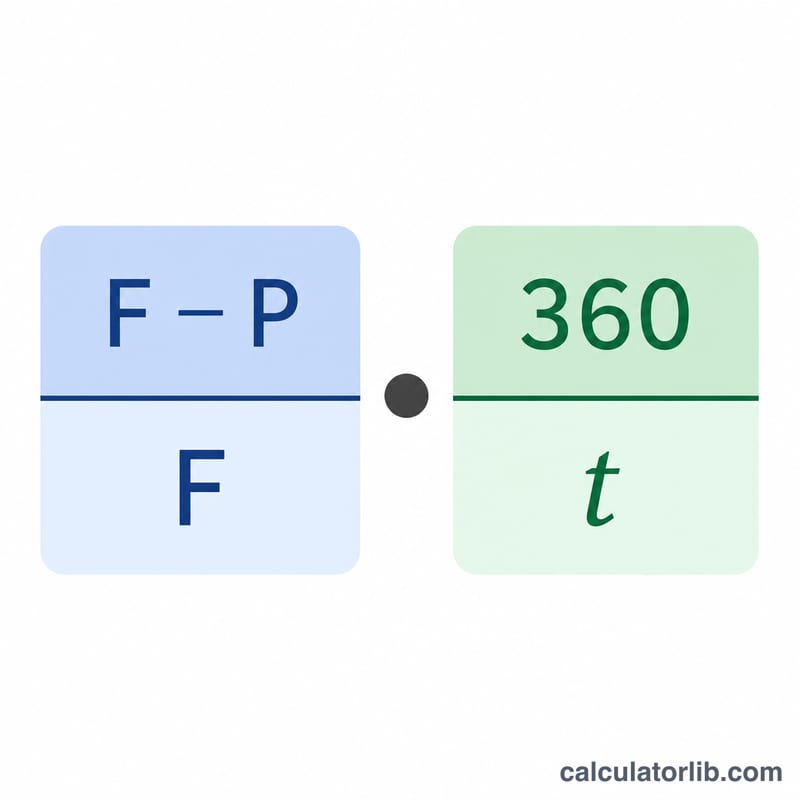

The bank discount yield is calculated as:

$$d = \frac{F - P}{F} \times \frac{360}{t}$$The first term, \(\frac{F - P}{F}\), is the discount expressed as a fraction of face value. The second term, \(\frac{360}{t}\), annualizes that figure on a 360-day basis. Note that the discount yield uses face value as the denominator, which slightly understates the true investment return — that is why the bond equivalent yield (which uses price and a 365-day year) is also shown.

Worked Example

Suppose you buy a T-bill with a $10,000 face value for $9,750, maturing in 90 days. The discount is \(\$10{,}000 - \$9{,}750 = \$250\). The discount yield is $$\frac{250}{10{,}000} \times \frac{360}{90} = 0.025 \times 4 = 0.10,$$ or 10.00%. The bond equivalent yield is \(\frac{250}{9{,}750} \times \frac{365}{90} \approx 10.40\%\).

FAQ

Why 360 days and not 365? Money markets historically use a 360-day year for discount instruments. This is a quoting convention, not the true calendar.

Why is the discount yield lower than the bond equivalent yield? The discount yield divides by face value (larger denominator) and uses 360 days, both of which reduce the figure relative to the true investment return.

Does this apply outside the U.S.? The 360/365 conventions are widely used in international money markets, though specific instruments may follow local day-count rules. The formula here matches the standard U.S. T-bill discount basis.