What Is a Loan Affordability Calculator?

A loan affordability calculator works the mortgage and loan math in reverse. Instead of asking "what is the payment on a given loan," it asks "given a payment I can comfortably afford, how large a loan can I take out?" This is one of the most practical questions for anyone shopping for a home, car, or personal loan, because your real-world budget — not the listing price — is the true limit on what you can borrow.

How to Use It

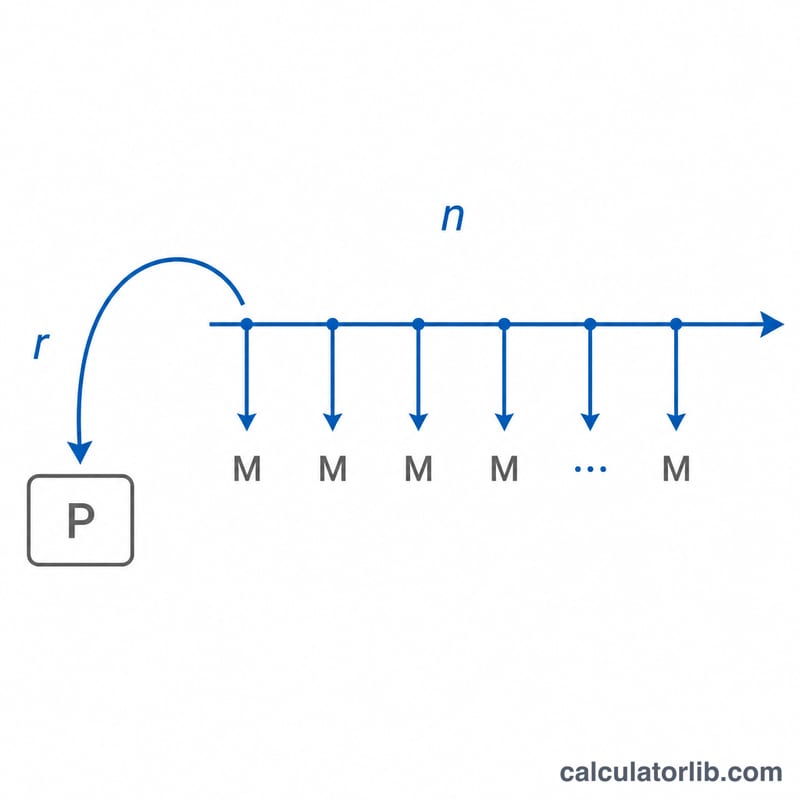

Enter three values: the monthly payment you can comfortably afford, the annual interest rate or APR offered by your lender, and the loan term in years. The calculator returns the maximum loan principal that payment can support, along with the total amount you will pay over the life of the loan and the portion that is interest.

The Formula Explained

The calculation uses the present value of an annuity formula: $$P = M \times \dfrac{1 - (1 + r)^{-n}}{r}$$ Here M is your monthly payment, \(r\) is the monthly interest rate (the APR divided by 100 and then by 12), and \(n\) is the total number of monthly payments (years × 12). The term in parentheses is the annuity discount factor — it sums the present value of every future payment, giving you the loan amount those payments can buy today. When the interest rate is zero, the formula simplifies to \(P = M \times n\).

Worked Example

Suppose you can afford $1,500 per month, your lender offers a 6% APR, and you want a 30-year loan. The monthly rate is \(r = 0.06 / 12 = 0.005\), and \(n = 360\) months. Plugging in: $$P = 1500 \times \dfrac{1 - 1.005^{-360}}{0.005} \approx \$250{,}187$$ Over 30 years you would pay $540,000 in total, of which about $289,813 is interest.

Interpreting Your Result

The figure this calculator returns is the principal only — the loan balance whose scheduled principal-and-interest payments equal your chosen monthly amount. It is not the total you will repay. Over the full term you repay the principal plus all interest; that total cost equals \(M \times n\). For example, a $1,500 payment for 30 years totals \(1500 \times 360 = \$540{,}000\) paid, so a $250,000 loan at 6% involves roughly $290,000 of interest over its life.

Principal vs. total cost. A longer term lets you borrow more for the same payment, but you pay interest on the balance for more years, raising total cost. A shorter term or higher rate reduces the present value of your payment stream, so the principal you can support shrinks even though each monthly payment is unchanged.

Why higher rate and shorter term lower borrowing power. The principal is the discounted (present) value of your future payments. A higher monthly rate \(r\) discounts each payment more heavily, and a smaller number of payments \(n\) means fewer payments to add up — both shrink the sum. Lenders therefore approve smaller loans at the same payment when rates rise or terms shorten.

The 28/36 DTI guideline. This rule comes from conventional mortgage underwriting standards used by lenders and the agencies that buy their loans. It suggests your housing payment stay at or below 28% of gross monthly income (the front-end ratio) and that total debt payments — housing plus car loans, student loans, credit cards and other obligations — stay at or below 36% (the back-end ratio). To translate a target into an affordable payment: if you earn $6,000 gross per month, 28% is $1,680 available for housing principal and interest. You can check how a proposed payment fits your income with a debt-to-income ratio calculator.

What the result excludes. This calculator covers principal and interest only. It does not include property taxes, homeowners or mortgage insurance (PMI), HOA dues, closing costs, or loan origination fees. For a mortgage, those items can add hundreds of dollars to the true monthly cost, so the affordable principal you compute here should be treated as an upper bound before such expenses are layered in. The APR you enter is also treated as the nominal annual rate divided across 12 months; a lender's quoted APR that bundles fees will produce a slightly different effective cost.

Definitions & Glossary

- Principal (\(P\)) — the amount borrowed: the loan balance at origination, before any interest accrues. This is the value the calculator solves for.

- Monthly payment (\(M\)) — the fixed amount paid each period toward principal and interest. Here it is the payment you judge affordable.

- Monthly interest rate (\(r\)) — the periodic rate applied each month, equal to the annual rate divided by 12: \(r = \text{APR} / 1200\) when the APR is expressed as a percent.

- Number of payments (\(n\)) — the total count of monthly payments over the loan, \(n = 12 \times \text{term in years}\). A 30-year loan has \(n = 360\).

- APR vs. nominal rate — the nominal rate is the stated annual interest rate. The Annual Percentage Rate (APR) reflects the yearly cost of borrowing including certain fees, so it can exceed the nominal rate. This tool treats your entered APR as the rate driving the payment math.

- Loan term — the length of time over which the loan is scheduled to be repaid, here entered in years and converted to months.

- Present value of an annuity — the lump sum today that is financially equivalent to a stream of equal future payments, discounted at the periodic rate. The borrowing formula \(P = M\,\frac{1-(1+r)^{-n}}{r}\) is exactly the present value of an ordinary annuity of payments \(M\).

- Debt-to-income (DTI) ratio — total monthly debt payments divided by gross monthly income, expressed as a percentage. Lenders use it (commonly with a 28%/36% guideline) to gauge how much debt a borrower can responsibly carry.

FAQ

Does this include taxes and insurance? No. The result is the loan principal only. For a mortgage, set aside additional budget for property tax, homeowner's insurance, and any HOA fees.

What payment should I enter? Use a figure that leaves comfortable room in your budget — lenders often suggest keeping total housing costs under about 28% of gross monthly income.

Is APR the same as interest rate? APR includes certain fees, so it is usually slightly higher than the nominal interest rate. Using APR gives a more conservative, realistic estimate.