What It Is

The Weekly Loan Payment Calculator works out the fixed amount you repay each week on an amortizing loan. Instead of monthly compounding, it divides the annual percentage rate (APR) into 52 weekly periods, which matches loans and lines of credit that bill on a weekly schedule.

How to Use It

Enter the loan amount (the principal you borrow), the annual interest rate as a percentage, and the term measured in weeks. The calculator returns your weekly payment, the total of all payments over the life of the loan, and the total interest you will pay.

The Formula Explained

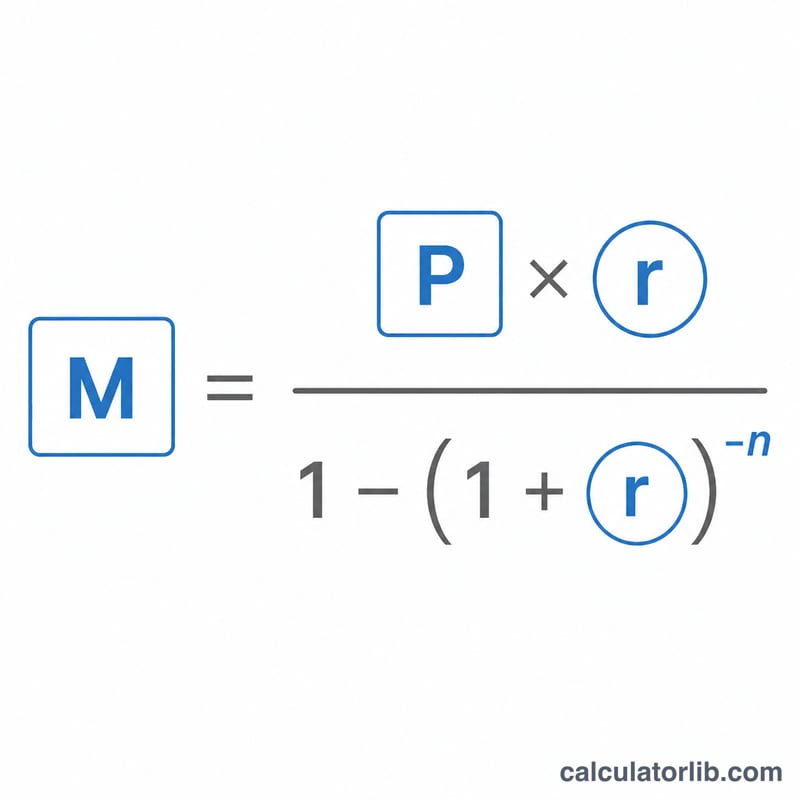

The standard amortization formula is $$M = P \cdot \frac{r}{1 - (1 + r)^{-n}}$$ Here \(P\) is the principal, \(r\) is the periodic interest rate, and \(n\) is the number of payments. For weekly loans the periodic rate is \(r = \text{APR} \div 52\), and \(n\) is the number of weeks. If the rate is zero the payment is simply \(P \div n\).

Worked Example

Borrow $10,000 at 6% APR over 52 weeks. The weekly rate is \(r = 0.06 \div 52 = 0.00115385\). With \(n = 52\), the payment is $$M = 10{,}000 \times \frac{0.00115385}{1 - 1.00115385^{-52}} \approx \$198.45$$ Over 52 weeks you pay about $10,319.50, of which roughly $319.50 is interest.

FAQ

Is the rate compounded weekly? Yes. The APR is divided by 52 to get the weekly rate used in the amortization formula.

Why is my total interest higher than a monthly loan? Total interest depends on rate and term length, not just the payment frequency. Comparable loans should yield similar totals; differences come from the exact compounding convention.

What if I enter 0% interest? The calculator falls back to dividing the principal evenly across all weeks, so the total interest is zero.