What this calculator does

This loan affordability calculator works backwards from your budget. Instead of telling you the monthly payment for a given loan, it tells you the largest loan principal you could take out for a monthly payment you are comfortable with. Amounts are shown in US dollars, but the math applies to any currency with monthly compounding and monthly payments. Use it for car, boat, home-equity, or general personal loans.

How to use it

Enter the monthly payment you can afford, choose a loan term (in months or years), and type the annual interest rate (APR) as a percentage. The calculator converts the term to a number of monthly payments (\(n\)) and the annual rate to a monthly rate (\(i\)), then computes the maximum principal.

The formula explained

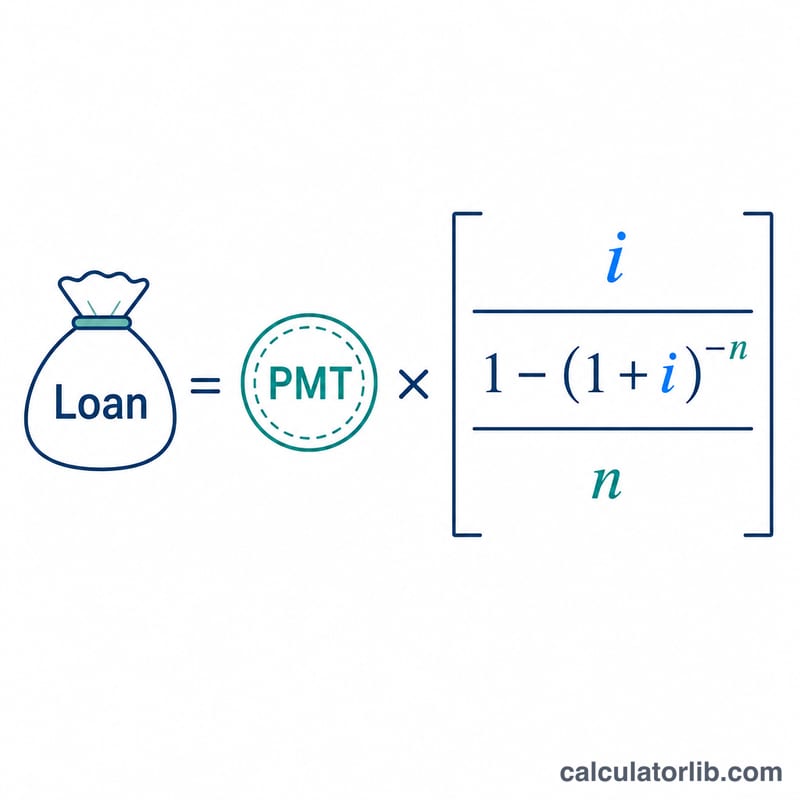

The result is the present value of an ordinary annuity. With a monthly rate \(i\) and \(n\) payments, the loan equals $$\text{Loan} = \text{PMT} \times \dfrac{1 - (1 + i)^{-n}}{i}$$ The monthly rate is the annual rate divided by 100 and then by 12. When the rate is exactly 0, the formula would divide by zero, so the calculator instead uses \(\text{Loan} = \text{PMT} \times n\).

Worked example

Suppose you can pay $350 per month for 48 months at 3.1250% APR. The monthly rate is \(0.031250 / 12 = 0.00260417\), and \(n = 48\). Plugging in: $$350 \times \frac{1 - 1.00260417^{-48}}{0.00260417} \approx 350 \times 45.066 \approx \$15{,}773$$ That is the maximum loan principal your budget supports.

FAQ

Does this include fees or down payments? No. It is a rough estimate that ignores credit rating, collateral, up-front fees, and fees rolled into the loan.

What rate should I enter? Use the annual percentage rate (APR) your lender quotes. A higher rate lowers the loan you can afford for the same payment.

Months or years? Either is fine — pick the unit in the dropdown. Years are simply multiplied by 12 to get monthly payments.