What This Calculator Does

Most loan calculators start with a loan amount and tell you the monthly payment. This one works in reverse: you tell it the monthly payment you can comfortably afford, the annual interest rate, and the loan term, and it tells you the maximum loan amount you could borrow. It's perfect for budgeting a mortgage, car loan, or personal loan around your cash flow rather than around a sticker price.

How to Use It

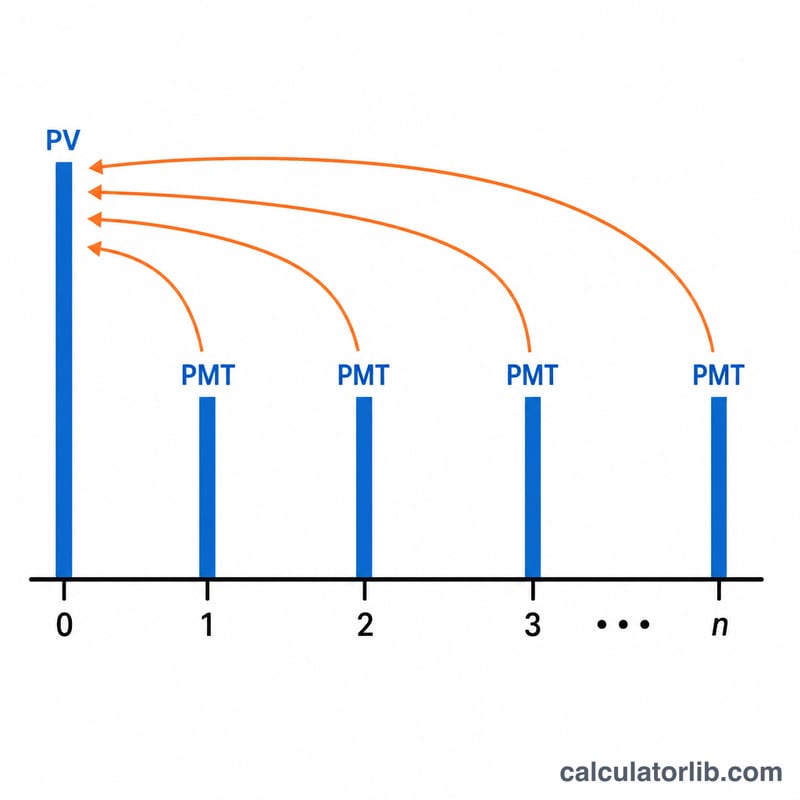

Enter the monthly payment you're willing to make, the annual interest rate offered by your lender (as a percentage), and the loan term in years. The calculator converts these into a monthly interest rate and a total number of payments, then computes the present value of that stream of payments — which is exactly the loan principal you can support.

The Formula Explained

The math is the present value of an ordinary annuity: $$PV = PMT \times \frac{1 - (1+i)^{-n}}{i}$$ Here PV is the loan amount, PMT is the monthly payment, \(i\) is the monthly interest rate (annual rate ÷ 12), and \(n\) is the number of monthly payments (years × 12). When the interest rate is 0%, the formula simplifies to \(PV = PMT \times n\).

Worked Example

Suppose you can pay $1,500 per month, the annual rate is 6%, and the term is 30 years. Then \(i = 0.06/12 = 0.005\) and \(n = 360\). $$PV = 1500 \times \frac{1 - 1.005^{-360}}{0.005} \approx \$250{,}187$$ Over the loan you'd pay \(\$1{,}500 \times 360 = \$540{,}000\), meaning roughly $289,813 in interest.

FAQ

Does this include taxes and insurance? No. It calculates the loan principal only. For a mortgage, set aside extra room in your budget for property tax, insurance, and HOA fees.

Is the payment principal and interest only? Yes. The result reflects a fully amortizing loan of principal and interest, with no escrow or fees added.

What if my rate is 0%? The calculator handles that automatically — your borrowing power simply equals the payment multiplied by the number of payments.