What Is a Business Loan EMI Calculator?

A Business Loan EMI Calculator works out the fixed Equated Monthly Installment (EMI) you will pay on a business loan. The EMI bundles both principal repayment and interest into a single, predictable monthly figure, making it easy to budget your company's cash flow before you sign a loan agreement.

How to Use It

Enter three values: the loan amount (the principal you borrow), the annual interest rate as a percentage, and the loan term in years. The calculator instantly returns your monthly EMI, the total interest you will pay over the life of the loan, and the total amount repaid.

The Formula Explained

The standard amortization formula is $$\text{EMI} = P \cdot \frac{r\,(1+r)^{n}}{(1+r)^{n}-1}$$ where P is the principal, r is the monthly interest rate (annual rate divided by 12 and by 100), and n is the total number of monthly payments (years \(\times\) 12). If the interest rate is zero, the EMI is simply the principal divided by the number of months.

Worked Example

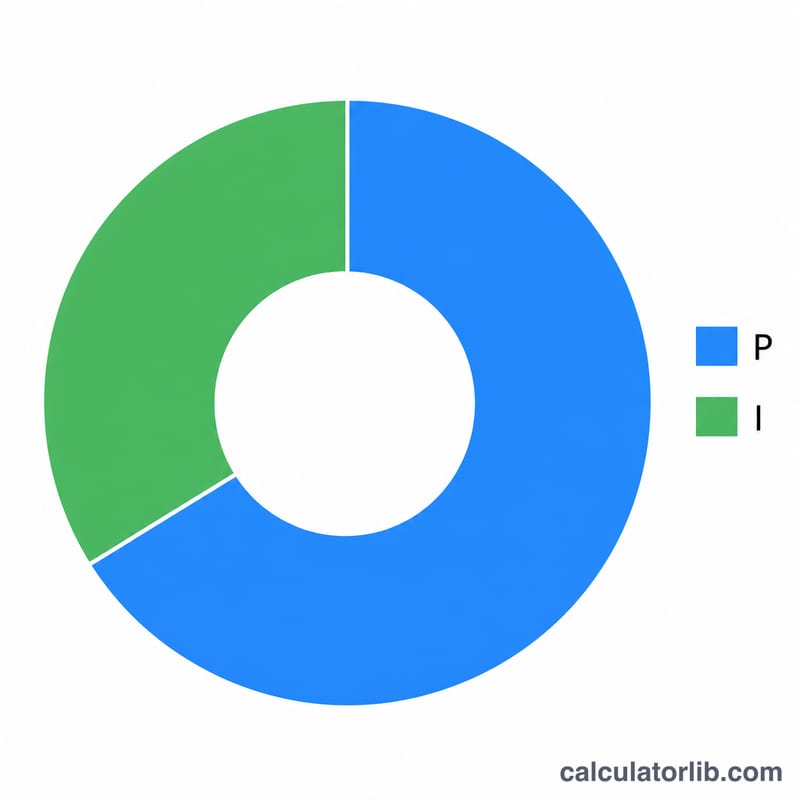

Suppose you borrow 500,000 at 12% annual interest over 5 years. The monthly rate \(r = 0.12 \div 12 = 0.01\), and \(n = 60\) months. Plugging into the formula gives an EMI of about 11,122.22 per month. Over 60 months you repay roughly 667,333, of which about 167,333 is interest.

Interpreting Your EMI Result

The calculator returns three figures, each measuring a different part of the same loan:

- EMI (Equated Monthly Instalment) — the fixed amount you pay every month. Under reducing-balance amortization each instalment is identical, but its composition changes over time: early payments are mostly interest, while later payments are mostly principal.

- Total interest — the sum of every interest portion across all \(n\) payments. It is the cost of borrowing, calculated as total repayment minus the original principal.

- Total repayment — the principal plus total interest, i.e. \(\text{EMI} \times n\). This is the full amount you will hand over across the life of the loan.

A longer term lowers the EMI because the principal is spread over more payments, easing monthly cash flow. The trade-off is that interest accrues on the outstanding balance for more months, so the total interest rises. A shorter term does the opposite: a higher EMI but less interest overall. The right balance depends on how much monthly outflow your business can comfortably sustain.

These results assume a fixed annual rate, equal monthly payments, and no missed payments. They exclude processing or origination fees, GST or other taxes, insurance, prepayment charges, and late-payment penalties — your actual cash outflow and effective cost may be higher. For a variable-rate (floating) loan, the EMI or the number of payments will change whenever the benchmark rate is revised, so the figures here reflect only the current rate as a snapshot.

This information is general and educational, not professional financial advice. Confirm exact terms, fees, and the applicable rate with your lender before committing.

Key Terms Explained

- EMI (Equated Monthly Instalment)

- The fixed monthly payment that fully repays a loan over its term, combining interest and principal in each instalment.

- Principal (\(P\))

- The original loan amount borrowed, before any interest is added. In the formula this is the starting balance on which interest is first charged.

- Annual interest rate

- The yearly rate quoted by the lender, expressed as a percentage (e.g. 12%). It must be converted to a monthly rate before use in the EMI formula.

- Monthly interest rate (\(r\))

- The annual rate divided by 12 and by 100, i.e. \(r = \dfrac{\text{annual rate \%}}{1200}\). For 12% per year, \(r = 0.01\) per month.

- Loan term

- The length of time over which the loan is repaid, usually stated in years. Here it is multiplied by 12 to get the number of monthly payments.

- Number of payments (\(n\))

- The total count of monthly instalments, equal to term in years \(\times\) 12. A 5-year loan has \(n = 60\) payments.

- Amortization

- The process of repaying a loan through scheduled equal payments, where each payment covers the accrued interest first and the remainder reduces the outstanding principal.

- Total interest

- The cumulative interest paid over the full term, equal to total repayment minus principal (\(\text{EMI}\times n - P\)).

FAQ

Does the EMI change over time? No — with a fixed-rate loan the EMI stays constant. Early payments contain more interest and later ones more principal, but the monthly amount is unchanged.

What currency does this use? The calculator is currency-agnostic; enter amounts in whatever currency your loan is denominated in.

Are processing fees included? No. The result reflects only principal and interest. Add any one-time fees separately to estimate the true cost of borrowing.