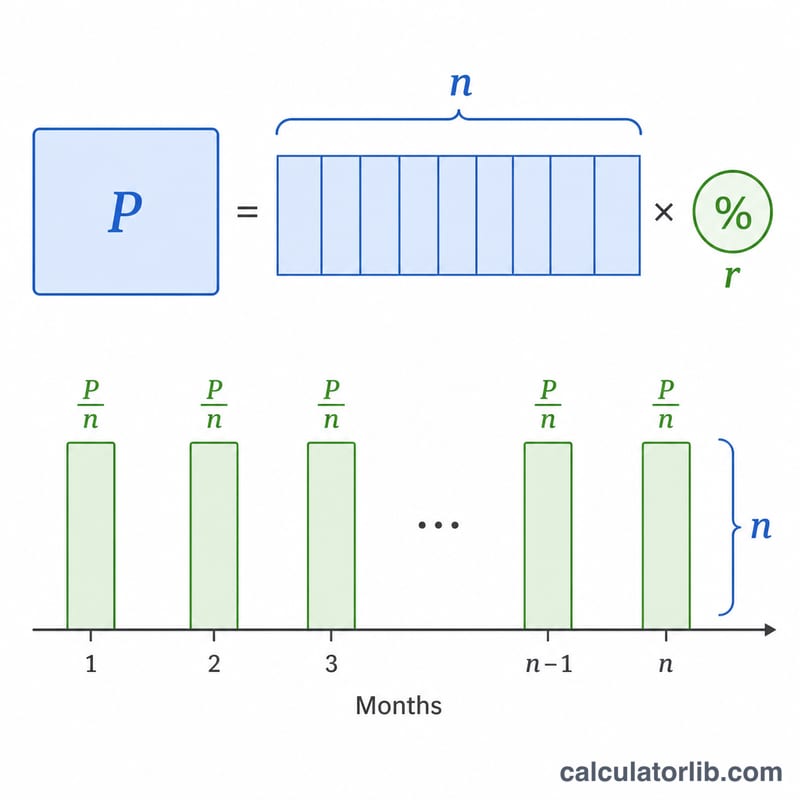

What is the ACB Personal Loan EMI Calculator?

This calculator estimates the Equated Monthly Installment (EMI) for a personal loan, such as one offered by ACB. An EMI is the fixed amount you repay each month over the loan term, covering both interest and principal. It uses the standard reducing-balance method, the most common way banks compute loan repayments.

How to use it

Enter three values: the loan amount (principal), the annual interest rate as a percentage, and the loan term in months. The calculator instantly returns your monthly EMI, the total interest you will pay over the life of the loan, and the total amount repaid (principal plus interest).

The formula explained

The EMI formula is $$\text{EMI} = \dfrac{P \cdot r \cdot (1+r)^n}{(1+r)^n - 1}$$ where P is the principal, r is the monthly interest rate (annual rate \(\div\) 1200), and n is the number of months. Dividing the annual rate by 1200 converts a percentage-per-year figure into a decimal-per-month rate. When the interest rate is zero, the EMI simply equals \(P \div n\).

Worked example

Suppose you borrow 500,000 at 12% annual interest for 60 months. The monthly rate \(r = 12 \div 1200 = 0.01\). With \(n = 60\), \((1.01)^{60} \approx 1.8167\). $$\text{EMI} = \frac{500{,}000 \times 0.01 \times 1.8167}{1.8167 - 1} \approx 11{,}122.22$$ per month. Over 60 months you repay about 667,333, of which roughly 167,333 is interest.

Key Terms Explained

- EMI (Equated Monthly Installment) — the fixed amount you pay every month, combining principal repayment and interest, so the loan is fully cleared by the end of the term.

- Principal (P) — the original loan amount you borrow, before any interest is added.

- Nominal annual interest rate — the quoted yearly rate (e.g. 12%) used to derive the monthly rate. It does not, by itself, account for compounding effects or fees.

- Monthly rate (r) — the per-month interest rate used in the EMI formula, calculated as the annual rate divided by 1200 (i.e. annual % ÷ 12 ÷ 100). For 12% annual, \(r = 12/1200 = 0.01\).

- Tenure / Term (n) — the total number of monthly installments. A 3-year loan has \(n = 36\).

- Reducing-balance method — interest each month is charged only on the outstanding balance, which falls as you repay. This is the standard method behind the EMI formula.

- Total interest — the sum of all interest paid over the life of the loan: total payment minus principal.

- Total payment — the total cash outflow over the term: \(\text{EMI} \times n\).

Understanding Your EMI Result

The EMI is the fixed monthly amount you commit to until the loan ends. Each installment is identical, but its internal split shifts over time. The total interest is the extra cost of borrowing — everything you pay above the principal — and the total payment is principal plus total interest, equal to the EMI multiplied by the number of months.

Under the reducing-balance method, interest dominates the early payments. Because interest is charged on the outstanding balance, the first installments are mostly interest with only a small slice going to principal; as the balance shrinks, later installments repay more principal and less interest. This is why paying extra early, or choosing a shorter term, sharply reduces total interest.

The result uses only the quoted nominal rate you entered. It does not include processing fees, loan insurance, late-payment penalties, government taxes, or any rate changes — so the real cost of an ACB personal loan may be higher than the figure shown here. Lenders often express the all-in cost as an APR; you can convert a quoted APR to its monthly equivalent with the APR to Monthly Interest Rate Calculator.

This calculation is an estimate for planning purposes only and is not a loan offer, approval, or financial advice. Actual terms depend on ACB's assessment of your application and the final contract you sign. For decisions about borrowing, confirm exact figures with the lender and consider speaking to a qualified financial professional.

FAQ

Does a longer term lower my EMI? Yes — spreading payments over more months reduces each installment but increases total interest paid.

Is this the actual amount ACB will charge? This is an estimate. Banks may add processing fees, insurance, or taxes, so confirm the exact figure with ACB.

What rate should I enter? Use the nominal annual interest rate quoted for your loan; the calculator converts it to a monthly rate automatically.