What This Calculator Does

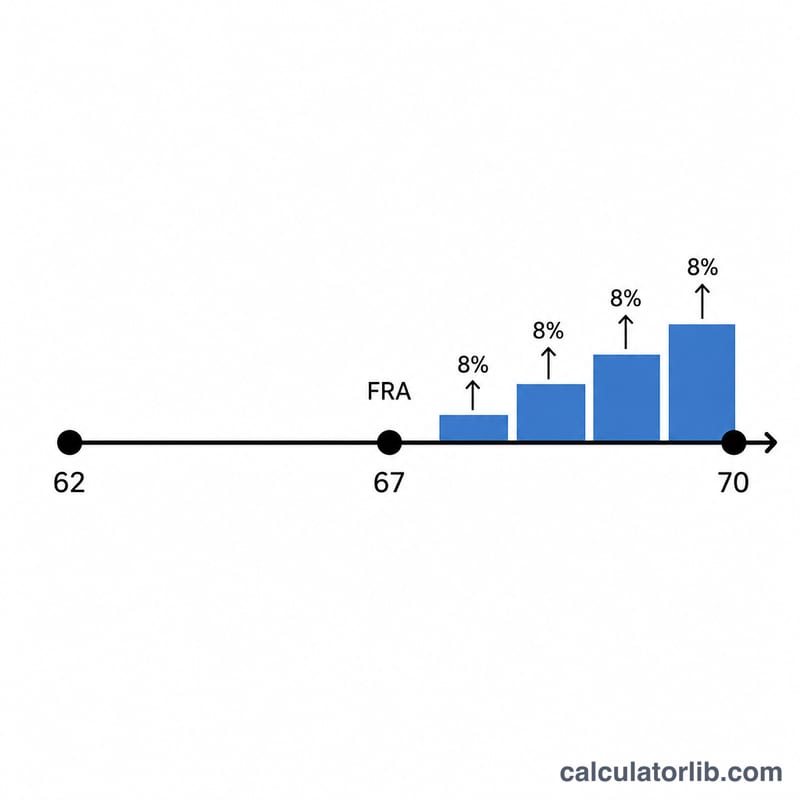

This tool applies to the United States Social Security retirement program. It estimates how much your monthly benefit increases if you delay claiming past your Full Retirement Age (FRA). For each full year you wait — up to age 70 — the Social Security Administration adds Delayed Retirement Credits (DRCs) worth 8% of your Primary Insurance Amount (PIA) per year. Credits stop accruing at age 70, so delaying beyond that provides no further increase.

How to Use It

Enter your PIA (the monthly benefit you would receive at FRA), your Full Retirement Age (66 or 67 for most people born after 1943), and the age you plan to start claiming. The calculator computes the years delayed after FRA, the total credit percentage, and your boosted monthly benefit.

The Formula Explained

The core equation is $$\text{Benefit} = \text{PIA} \times \left(1 + 0.08 \times \text{yearsDelayedAfterFRA}\right)$$ The 0.08 represents the 8% annual credit. If you claim before FRA, this calculator floors the credit at zero (it does not compute early-claiming reductions). Claiming after 70 is treated as 70 because credits cap there.

Worked Example

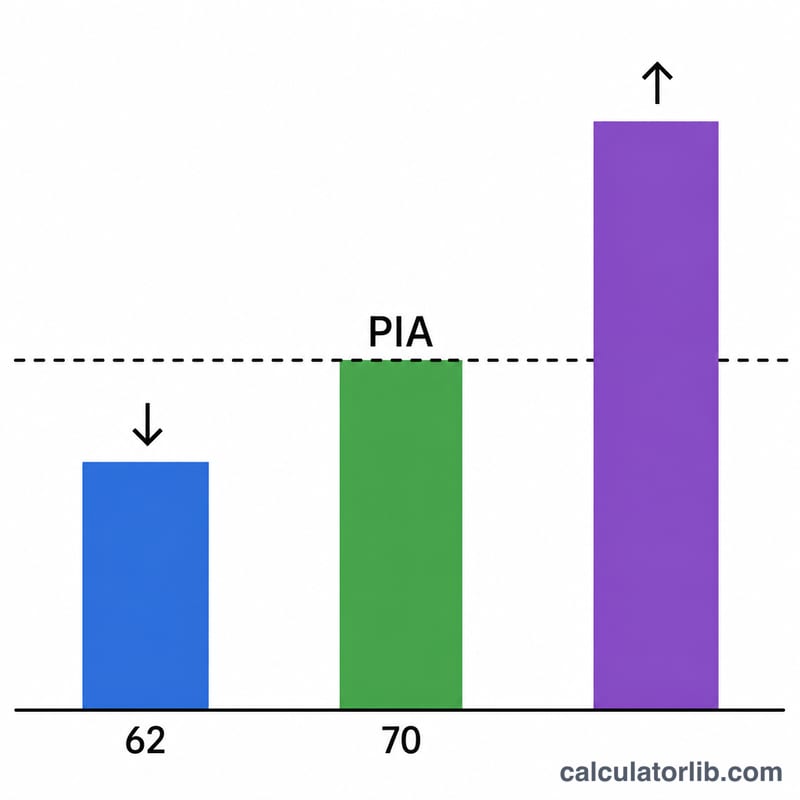

Suppose your PIA is $2,000, your FRA is 67, and you delay to age 70. That is 3 years delayed, so the credit is \(0.08 \times 3 = 0.24\) (24%). Your monthly benefit becomes $$\$2{,}000 \times 1.24 = \$2{,}480,$$ an increase of $480 per month over the PIA.

FAQ

Do delayed credits keep growing after 70? No. The 8% annual credit stops at age 70, so there is no benefit to waiting longer.

Are credits applied monthly or yearly? The SSA actually credits 2/3 of 1% per month (8% per year). This calculator uses whole-year delays for a clean estimate; partial years accrue proportionally.

Is this an official figure? No. This is an educational estimate. Cost-of-living adjustments, taxation, and earnings tests can change your actual benefit — check ssa.gov for your personalized statement.