What Is the Marginal Tax Rate Calculator?

This calculator applies to United States federal income tax using the 2026 tax-year brackets. It tells you your marginal tax rate — the percentage of tax you pay on your last dollar of taxable income — along with your total estimated federal tax and your effective (average) tax rate. It does not include state taxes, FICA/payroll taxes, deductions, or credits; enter your taxable income (income after deductions).

How to Use It

Enter your taxable income and select your filing status (Single or Married Filing Jointly). The calculator finds the highest bracket your income reaches — that bracket's rate is your marginal rate — and sums the progressive tax owed in each bracket up to your income.

The Formula Explained

The US uses a progressive system. Income is sliced into bands; each band is taxed at its own rate. Your marginal rate is simply the rate of the top band your income enters. Your effective rate is total tax \(\div\) income, which is always lower than the marginal rate because lower bands are taxed at lower rates.

$$\text{Marginal Rate} = \text{rate of the bracket containing } \text{Taxable Income}$$$$\text{Total Tax} = \sum_i \left(\min(\text{Income}, U_i) - L_i\right) \cdot r_i$$$$\text{Effective Rate} = \frac{\text{Total Tax}}{\text{Taxable Income}} \times 100\%$$

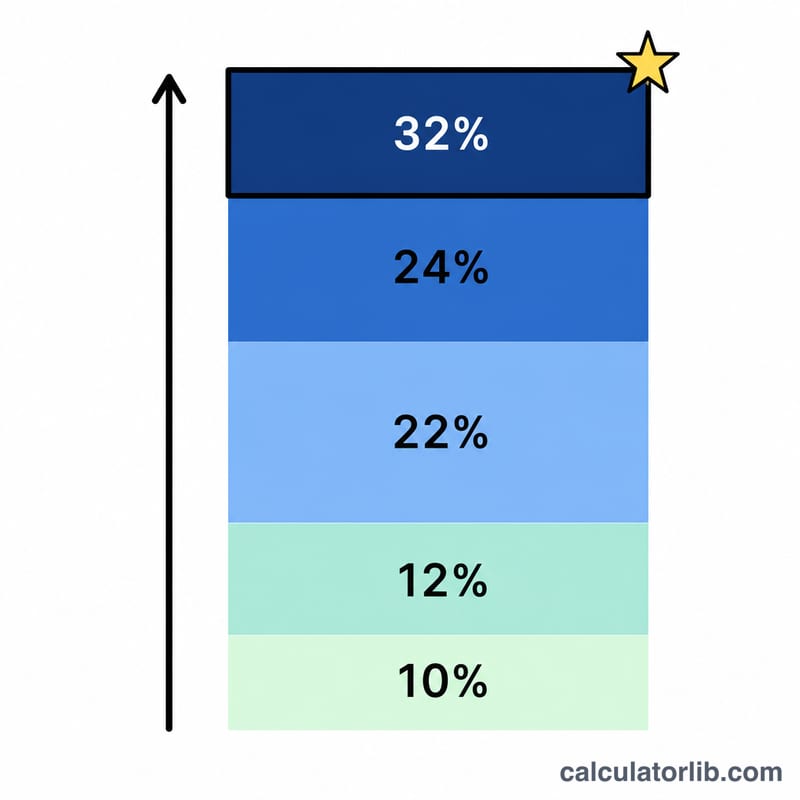

Worked Example

Single filer with $60,000 taxable income (2026): the first $12,400 is taxed at 10% (\(\$1{,}240\)), the next $38,000 (\(\$12{,}400\)–\(\$50{,}400\)) at 12% (\(\$4{,}560\)), and the remaining $9,600 (\(\$50{,}400\)–\(\$60{,}000\)) at 22% (\(\$2{,}112\)). Total tax \(\approx \$7{,}912\). Because $60,000 falls in the 22% band, the marginal rate is 22%, while the effective rate is about 13.19%.

$$\text{Total Tax} = 12400 \times 10\% + 38000 \times 12\% + 9600 \times 22\% \approx \$7{,}912$$$$\text{Effective Rate} = \frac{7912}{60000} \times 100\% \approx 13.19\%$$

FAQ

Is the marginal rate what I pay on all my income? No. Only the income within each bracket is taxed at that bracket's rate. Most of your income is taxed at lower rates.

What's the difference between marginal and effective rate? Marginal is the rate on your next/last dollar; effective is your overall average tax rate across all income.

Does this include state tax? No — it covers federal brackets only. Add your state's rates separately.