What This Calculator Does

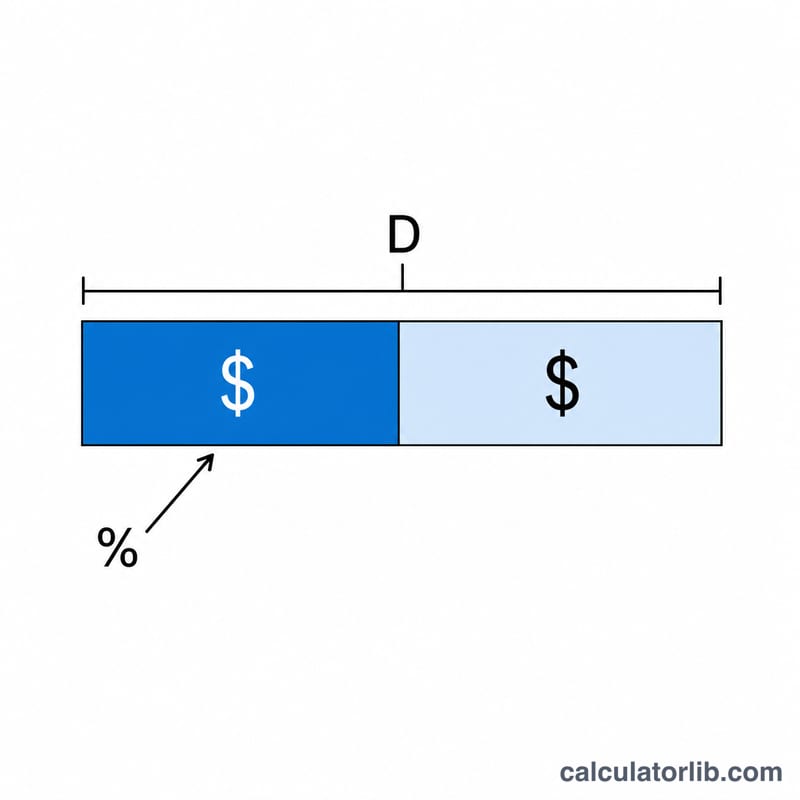

A tax deduction lowers your taxable income, not your tax bill directly. So a $1,000 deduction does not save you $1,000 in tax — it saves you $1,000 multiplied by your marginal tax rate (the rate on your last dollar of income). This calculator shows the real cash value of any deduction so you can make smarter decisions about charitable giving, retirement contributions, mortgage interest, and business expenses.

How to Use It

Enter the deduction amount in dollars and your marginal tax rate as a percentage. The tool returns the tax you save, the deduction amount for reference, and your net out-of-pocket cost (what the deductible expense actually costs you after the tax break).

The Formula Explained

The core relationship is $$\text{Tax Saved} = \text{Deduction} \times \text{Marginal Rate}$$ If you spend money on a fully deductible expense, the government effectively subsidizes it at your marginal rate. The remaining $$\text{Net Cost} = \text{Deduction} - \text{Tax Saved}$$ is what you truly pay.

Worked Example

Suppose you contribute $10,000 to a deductible retirement account and your marginal tax rate is 24%. Tax saved = $$\$10{,}000 \times 0.24 = \mathbf{\$2{,}400}$$ Your net cost is $$\$10{,}000 - \$2{,}400 = \mathbf{\$7{,}600}$$ In other words, the $10,000 contribution only costs you $7,600 after taxes.

FAQ

Marginal vs. effective rate — which do I use? Use your marginal rate. Deductions reduce income from the top down, so they are valued at the rate on your highest taxed dollars.

Why isn't a deduction worth its full amount? Because it reduces taxable income, not tax owed. A credit reduces tax dollar-for-dollar; a deduction only saves a percentage.

Can the savings push me into a lower bracket? A large deduction can straddle two brackets, in which case the blended saving is slightly less than your top rate. This tool uses a single marginal rate for a clean estimate.