What Is the QBI Deduction?

This calculator applies to United States federal income tax under Internal Revenue Code Section 199A. The Qualified Business Income (QBI) deduction lets eligible owners of pass-through businesses — sole proprietorships, partnerships, S corporations, and many LLCs — deduct up to 20% of their qualified business income. This tool computes the simplified version of the deduction. It does not apply the specified-service-trade-or-business (SSTB) phase-out or the W-2 wage / unadjusted-basis limits that apply above the income thresholds, so treat the result as an estimate for taxpayers below those thresholds.

How to Use It

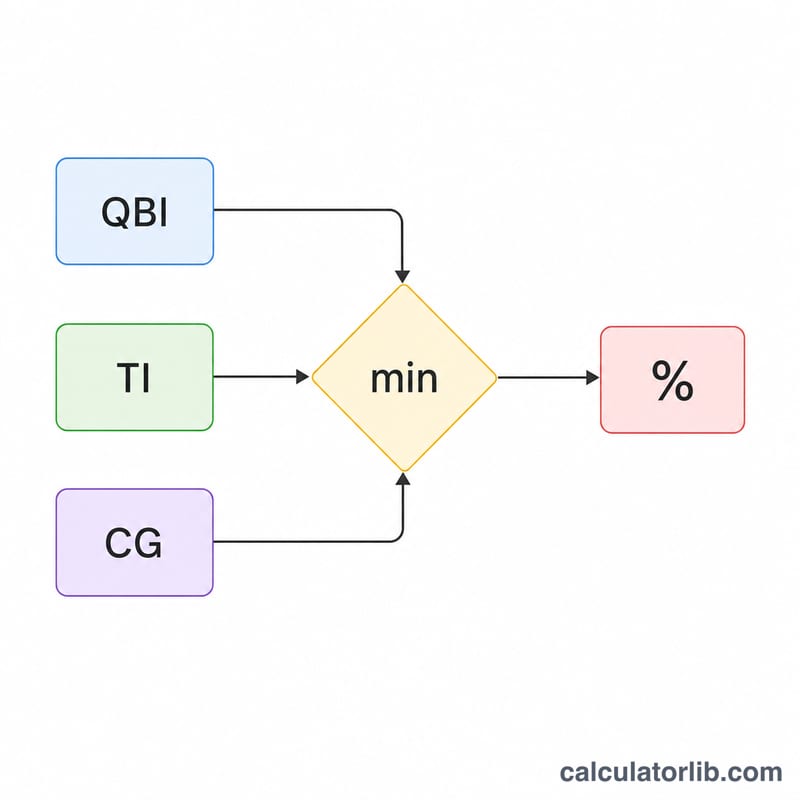

Enter your qualified business income, your taxable income before the QBI deduction, and your net capital gain (which for this purpose includes qualified dividends). The calculator returns the smaller of the two limits, which is your estimated deduction.

The Formula Explained

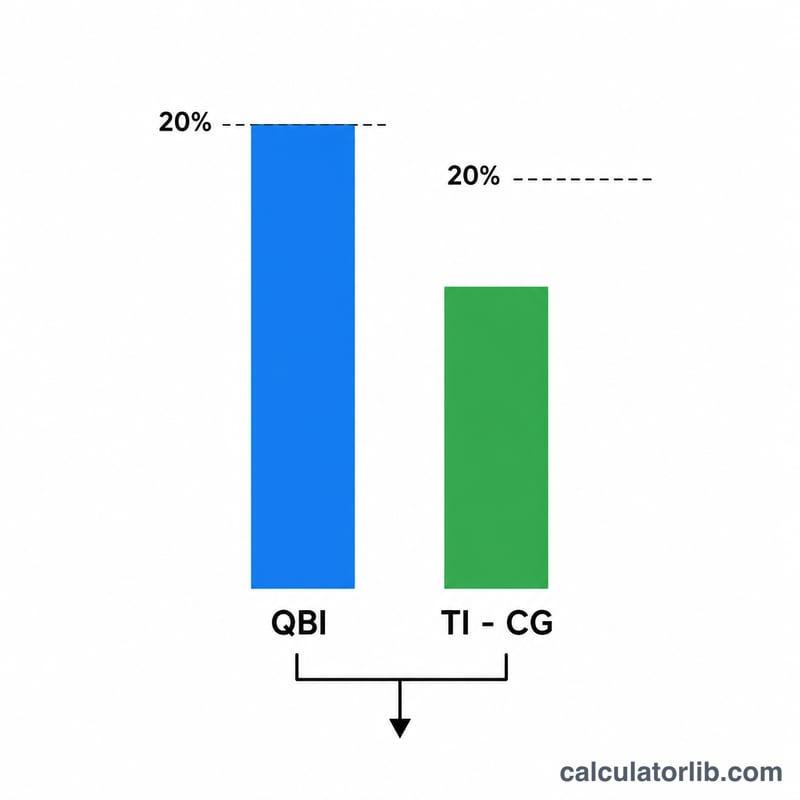

The deduction equals the lesser of two amounts: (1) 20% of your QBI, and (2) 20% of your taxable income minus net capital gain. The second term is an overall cap that prevents the deduction from exceeding 20% of your ordinary taxable income. Net capital gain is subtracted because that income is already taxed at preferential rates and does not qualify.

$$\text{QBI Deduction} = \min\left(0.20 \times \text{QBI},\; 0.20 \times \left(\text{Taxable Income} - \text{Net Capital Gain}\right)\right)$$

Worked Example

Suppose QBI is $100,000, taxable income is $120,000, and net capital gain is $10,000. The QBI component is \(0.20 \times \$100{,}000 = \$20{,}000\). The income limit is \(0.20 \times (\$120{,}000 - \$10{,}000) = \$22{,}000\). The deduction is the lesser, $20,000.

FAQ

What counts as net capital gain? For the QBI limit it means net long-term capital gain over net short-term capital loss, plus qualified dividends.

Does this handle the high-income limits? No. Above the annual taxable-income threshold, W-2 wage limits, qualified property limits, and SSTB phase-outs apply; this tool covers the basic case only.

Can the deduction be zero? Yes — if taxable income minus net capital gain is zero or negative, the income limit is $0 and so is the deduction.