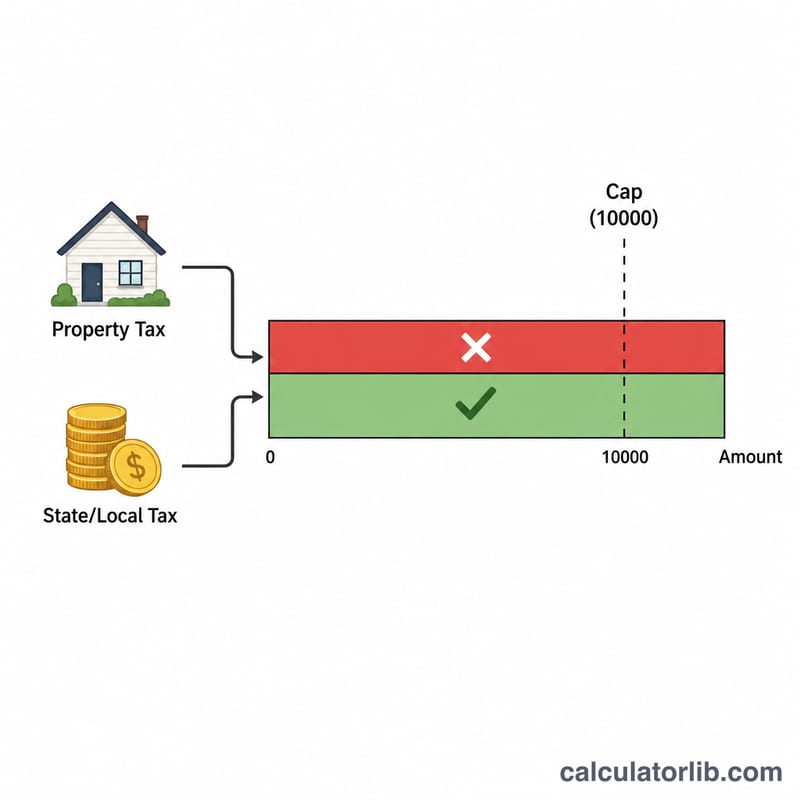

What is the SALT Deduction Cap?

Applies to: United States federal income tax (tax years 2018 onward, under current law). The State and Local Tax (SALT) deduction lets taxpayers who itemize on Schedule A deduct certain state and local taxes — namely state/local income (or general sales) taxes plus property taxes. Since the Tax Cuts and Jobs Act of 2017, the total SALT deduction is capped at $10,000 per return ($5,000 if married filing separately). This calculator shows how much of your SALT you can actually deduct and how much is lost to the cap.

How to Use It

Enter the state and local income or sales taxes you paid, your property taxes, and your filing status. The tool adds the two amounts, applies the correct cap, and reports your deductible figure plus the portion that exceeds the limit. Use it to gauge the federal benefit of itemizing versus taking the standard deduction.

The Formula Explained

The math is a simple minimum function: $$\text{Deductible} = \min\Big( \text{State \& Local Taxes} + \text{Property Taxes},\ \$10{,}000 \Big)$$ Add your two tax categories, then cap the result. If the sum is under the cap, you deduct the full amount; if it is over, you are limited to \(\$10{,}000\) (or \(\$5{,}000\) MFS), and the remainder is non-deductible.

Worked Example

Suppose you paid $8,000 in state income tax and $6,000 in property tax, filing jointly. Total SALT $$= \$8{,}000 + \$6{,}000 = \$14{,}000.$$ The cap is \(\$10{,}000\), so your deductible SALT is $$\min\Big( \$14{,}000,\ \$10{,}000 \Big) = \$10{,}000$$ and \(\$4{,}000\) is lost to the cap.

FAQ

What counts as SALT? State and local income taxes (or sales taxes — you choose one), plus real-estate and personal property taxes.

Does the cap apply if I take the standard deduction? No — the SALT deduction only matters when you itemize on Schedule A.

Is the limit different for married filing separately? Yes, it drops to \(\$5{,}000\) per spouse. This calculator adjusts automatically.