What Is the Section 179 Deduction?

This calculator applies to the United States and uses the IRS Section 179 limits for tax year 2023: a maximum deduction of $1,160,000 and a spending phase-out threshold of $2,890,000. Section 179 lets businesses deduct the full purchase price of qualifying equipment and software in the year it is placed in service, rather than depreciating it over many years. Always confirm current-year figures and eligibility with a tax professional or IRS Publication 946.

How to Use It

Enter the cost of the specific asset you want to deduct, your total equipment purchases for the year, and an optional bonus depreciation rate (60% for 2024-placed property, often 100% in earlier years — check the applicable year). The tool computes the allowable Section 179 amount after any phase-out, then applies bonus depreciation to the remaining basis.

The Formula Explained

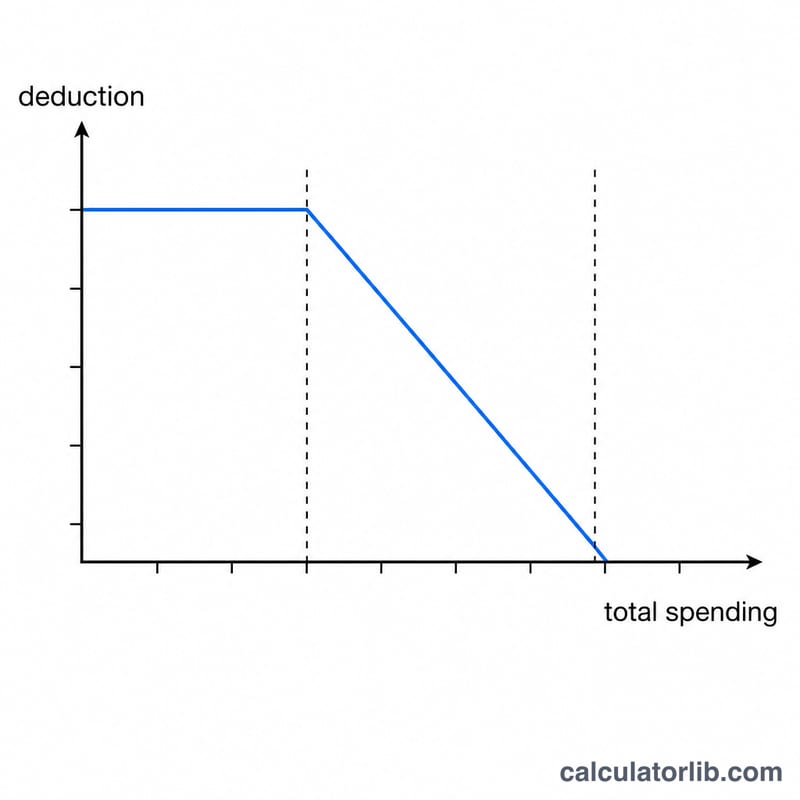

The annual $1,160,000 limit is reduced dollar-for-dollar by the amount your total purchases exceed $2,890,000. So if you buy $2,950,000 of equipment, your limit drops by $60,000 to $1,100,000. The Section 179 deduction is then the smaller of the asset cost and this adjusted limit. Whatever basis remains can take bonus depreciation.

$$\begin{gathered} D = S_{179} + \left(\text{Cost} - S_{179}\right)\times \dfrac{\text{Bonus Rate}}{100} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} S_{179} &= \min\!\left(\text{Cost},\ L\right) \\ L &= \max\!\left(0,\ 1{,}160{,}000 - \max\!\left(0,\ \text{Total Purchases} - 2{,}890{,}000\right)\right) \end{aligned} \right. \end{gathered}$$

Worked Example

You buy a $100,000 machine and your total purchases are $100,000 (under the threshold, so no phase-out). With a 60% bonus rate: Section 179 = \(\min(\$100{,}000,\ \$1{,}160{,}000) = \$100{,}000\). Because the full cost is already deducted, remaining basis is $0 and bonus depreciation is $0. Total first-year deduction = $100,000.

FAQ

Can the deduction exceed my purchase cost? No — it is capped at the asset cost you enter.

What if I spend more than $4,050,000? The Section 179 limit phases out completely, so the deduction drops to $0 (but bonus depreciation may still apply).

Is there an income limit? Yes. Section 179 cannot exceed your business taxable income; this calculator does not apply that cap.