What is the American Opportunity Tax Credit?

The American Opportunity Tax Credit (AOTC) is a United States federal tax credit for qualified education expenses paid for an eligible student during the first four years of higher education. This calculator applies the standard AOTC rules used in recent tax years. Note: this is a US-only tool and provides an estimate, not tax advice. Contribution and phase-out thresholds are fixed by statute and have not been inflation-indexed.

How to use this calculator

Enter the total qualified education expenses you paid for one eligible student (tuition, required fees, and course materials), your Modified Adjusted Gross Income (MAGI), and your filing status. The calculator computes your tentative credit and then applies the income phase-out to show the credit you can actually claim.

The formula explained

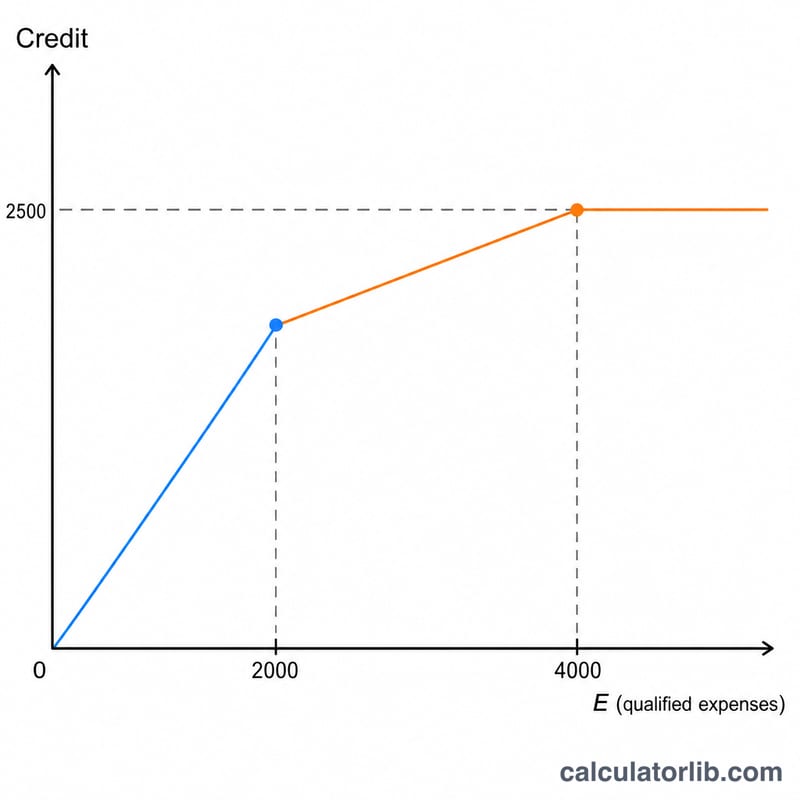

The credit equals 100% of the first $2,000 of qualified expenses plus 25% of the next $2,000, for a maximum of $2,500 per student.

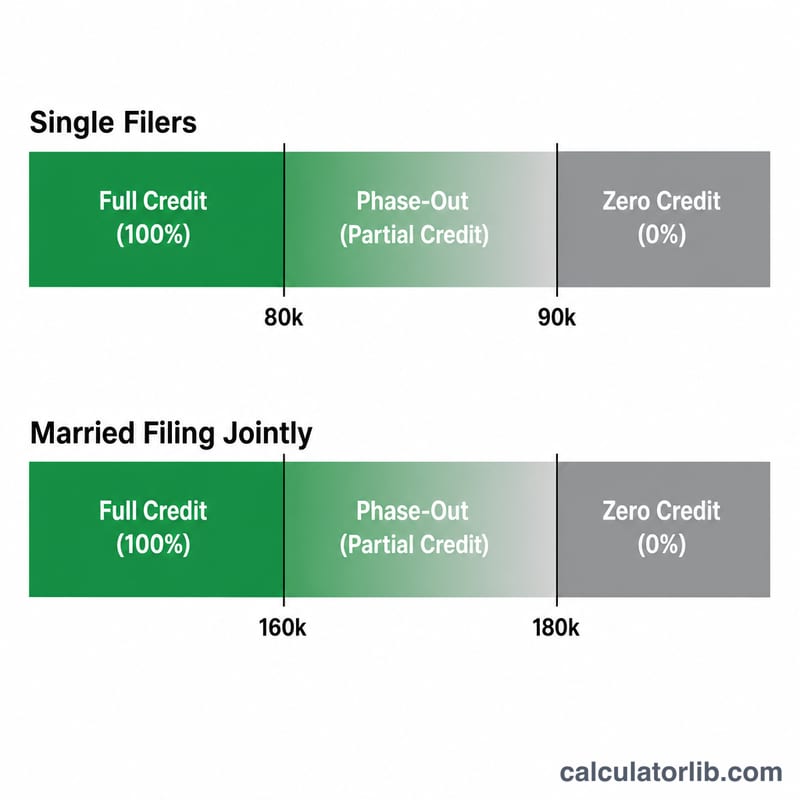

$$\text{Credit} = \min(2000, E) + 0.25 \times \min(2000, \max(E-2000, 0))$$The credit then phases out based on income. For single/head-of-household filers, the phase-out runs from $80,000 to $90,000 of MAGI; for married filing jointly, it runs from $160,000 to $180,000. Within that band the allowed percentage is \((\text{PhaseEnd} - \text{MAGI}) \div \$10{,}000\).

$$f = \frac{\text{PhaseEnd} - \text{MAGI}}{\text{PhaseEnd} - \text{PhaseStart}}$$

Worked example

Suppose you paid $4,000 in qualified expenses and have a MAGI of $60,000 filing single. The tentative credit is

$$100\% \times \$2{,}000 + 25\% \times \$2{,}000 = \$2{,}000 + \$500 = \$2{,}500$$Because $60,000 is below the $80,000 phase-out start, the full $2,500 is allowed.

AOTC Key Figures and Thresholds

The following values define how the American Opportunity Tax Credit is computed. They have remained stable since the AOTC was made permanent and, unlike many tax figures, the phase-out thresholds are not indexed for inflation.

| Item | Value |

|---|---|

| Credit rate on first $2,000 of qualified expenses | 100% |

| Credit rate on next $2,000 of qualified expenses | 25% |

| Maximum credit per eligible student | $2,500 |

| Refundable portion | 40% (up to $1,000) |

| Nonrefundable portion | 60% (up to $1,500) |

| Phase-out range — Single / Head of Household | $80,000 – $90,000 MAGI |

| Phase-out range — Married Filing Jointly | $160,000 – $180,000 MAGI |

| Phase-out band width — Single / HoH | $10,000 |

| Phase-out band width — MFJ | $20,000 |

| Married Filing Separately | Not eligible to claim AOTC |

| Maximum years claimable per student | 4 tax years |

Within a phase-out range, the credit is reduced proportionally. For a single filer with MAGI of $85,000 (halfway through the $80,000–$90,000 band), the allowed credit is half of the tentative amount.

Key Terms Explained

- Modified Adjusted Gross Income (MAGI)

- For the AOTC, MAGI is your adjusted gross income (AGI) plus certain items added back, such as foreign earned income and foreign housing exclusions. For most U.S. taxpayers with no foreign income, MAGI equals AGI.

- Qualified education expenses

- Tuition, required enrollment fees, and required course materials (books, supplies, equipment) for an eligible student. It does not include room and board, insurance, transportation, or medical expenses.

- Eligible student

- A student pursuing a degree or recognized credential, enrolled at least half-time for at least one academic period during the year, who has not completed the first four years of post-secondary education and has not claimed the AOTC for more than four tax years.

- Refundable vs. nonrefundable credit

- A nonrefundable credit can reduce your tax only to zero. A refundable credit can produce a refund beyond your tax liability. Up to 40% of the AOTC (a maximum of $1,000) is refundable; the remaining 60% is nonrefundable.

- Phase-out

- A gradual reduction of the credit as income rises through a defined MAGI range. Below the range you get the full tentative credit; above it the credit is $0; within it the credit is reduced in proportion to where your MAGI falls.

- Filing status

- Single and Head of Household (HoH) share the $80,000–$90,000 phase-out range. Married Filing Jointly (MFJ) uses the $160,000–$180,000 range. Married Filing Separately cannot claim the AOTC.

- Lifetime Learning Credit (LLC)

- An alternative education credit worth up to $2,000 per return (20% of up to $10,000 of expenses). Unlike the AOTC, it is entirely nonrefundable, has no four-year or half-time limit, but cannot be claimed for the same student's same expenses in the same year as the AOTC.

FAQ

Is part of the AOTC refundable? Yes — up to 40% of the credit (max $1,000) can be refundable, but this calculator estimates the total credit amount before refundability splitting.

Can I claim it for more than one student? Yes, the AOTC is per eligible student, so run the calculator separately for each one.

What if my MAGI is above the limit? If your MAGI exceeds $90,000 (single) or $180,000 (MFJ), the credit is fully phased out to $0; you may instead qualify for the Lifetime Learning Credit.