What Is a Credit Spread?

A credit spread is the difference in yield between a bond carrying credit risk (such as a corporate or high-yield bond) and a risk-free benchmark of the same maturity, typically a government treasury. It represents the extra compensation investors demand for taking on the issuer's default risk, liquidity risk, and other uncertainties. A wider spread signals higher perceived risk; a narrower spread signals confidence in the issuer.

How to Use This Calculator

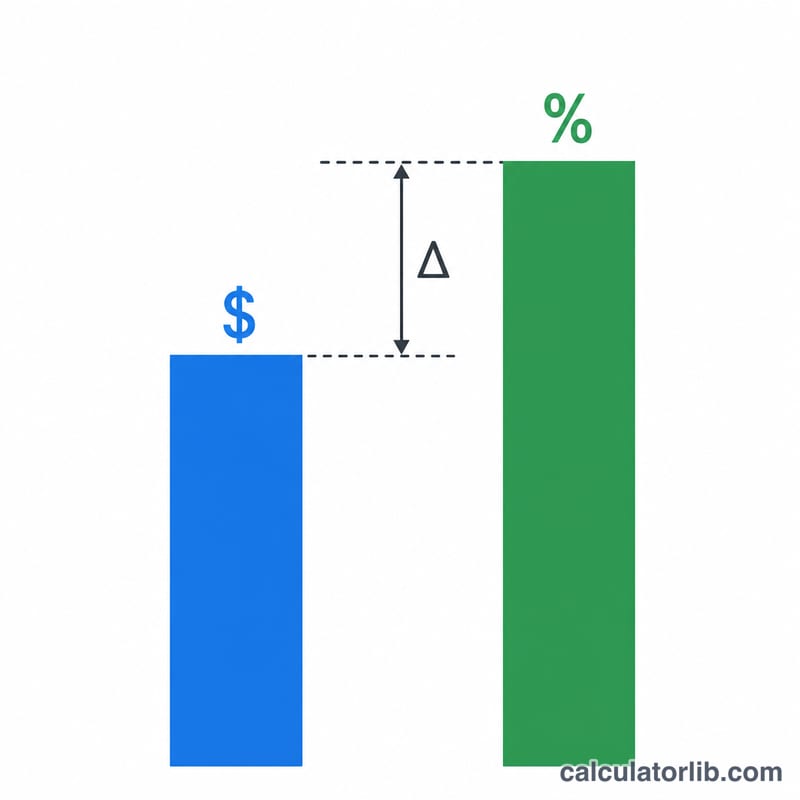

Enter the yield to maturity of the bond you are analyzing and the yield of a comparable risk-free instrument with the same maturity. The calculator subtracts the two and returns the credit spread expressed both as a percentage and in basis points (bps), where 1% equals 100 bps.

The Formula Explained

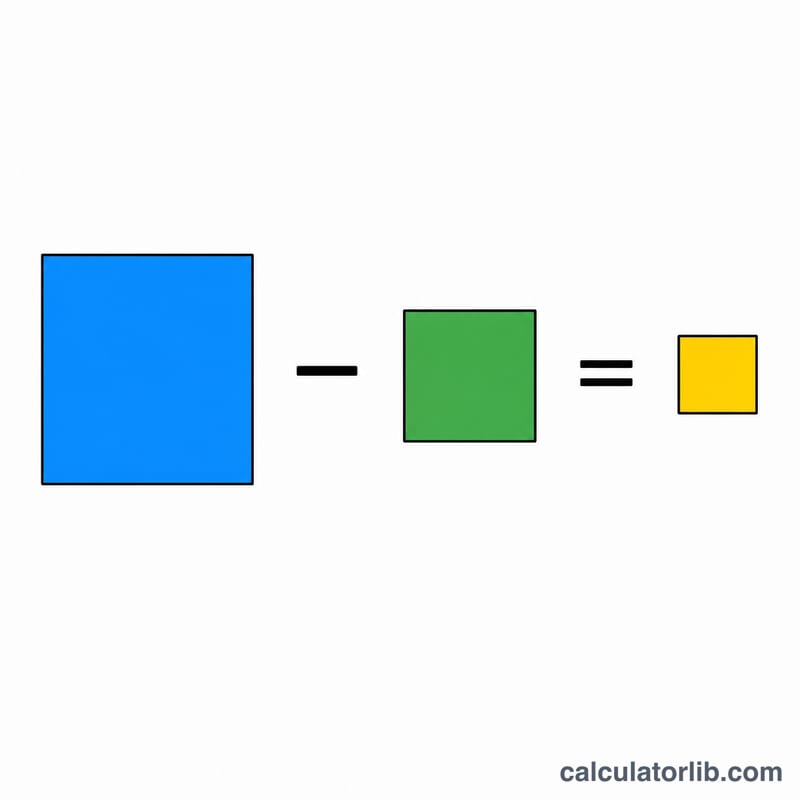

The calculation is intentionally simple: Credit Spread = Bond Yield − Risk-Free Yield. To convert to basis points, multiply the percentage result by 100:

$$\text{Spread (bps)} = \left(\text{Bond Yield (\%)} - \text{Risk-Free Yield (\%)}\right) \times 100$$Matching maturities matters — comparing a 10-year corporate bond to a 2-year treasury would distort the spread because of the term structure of interest rates.

Worked Example

Suppose a corporate bond yields 5.5% and the 10-year treasury yields 3.0%. The credit spread is:

$$\left(5.5\% - 3.0\%\right) \times 100 = 250 \text{ bps}$$That 250 bps is the premium the market is paying you to hold the corporate bond instead of the risk-free treasury.

FAQ

Why use basis points? Bond markets quote small yield differences in basis points for precision; \(0.25\%\) is easier to discuss as "25 bps."

Can the spread be negative? Rarely, but it can occur due to liquidity premiums, supply/demand imbalances, or data timing differences. A persistently negative spread is unusual.

What is a "good" spread? It depends on credit quality — investment-grade bonds often trade at tighter spreads (under 200 bps) while high-yield bonds can exceed 500 bps. Higher spread means higher risk and higher potential reward.